Summary

- Many tech names have done stock splits in 2020 and 2021 that got a lot of attention.

- INTC has split its shares oftentimes in the past, but not in the last 20 years. We'll look at the reasons and what they mean for the future.

- Intel has some issues, but on the other hand, shares are pretty inexpensive and offer an above-average yield. All in all, Intel does neither look especially strong nor especially bad.

- I do much more than just articles at Cash Flow Kingdom: Members get access to model portfolios, regular updates, a chat room, and more.

Article Thesis

Due to reader demand, we'll take a look at whether Intel Corporation (INTC) might conduct another stock split in the foreseeable future. Peers such as NVIDIA (NVDA) have done so in the recent past, thus the idea is not completely outlandish. At the same time, however, it should be noted that Intel's share price has been languishing in the recent past, and since shares are far from expensive, I believe that a stock split in the near term is unlikely.

INTC Stock Price

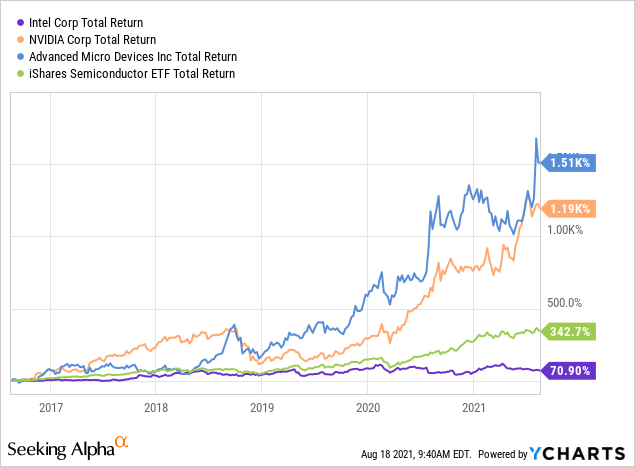

Intel Corporation is a leading semiconductor company in terms of revenue generation and output, but due to problems with new processes, and due to declining market share versus peers such as NVIDIA Corp and AMD (AMD), its shares have vastly underperformed the broad semiconductor industry in recent years:

With a 70% return over five years, Intel has been far from a bad investment, as this still pencils out to about 11% a year. But compared to its peers and the semiconductor industry as a whole (SOXX), Intel Corporation's returns look pretty bad, as others have seen their shares rise by 300%+ in the same time frame. With a market capitalization of $210 billion, Intel is cheaper than NVIDIA, despite the fact that Intel generates much higher revenue, earnings, and cash flow -- the market is valuing NVIDIA at a premium due to its better growth and more attractive product lineup. At current prices of around $53, Intel is trading ~20% below the consensus price target of $63, which indicates solid upside potential over the next year. Based on current earnings per share estimates for this year, Intel Corporation trades for 11x net profits, which is one of the lowest valuations in the semiconductor industry, and which represents a clear discount compared to how the broad market is valued. At the same time, Intel also offers a dividend yield of 2.6% today -- which is roughly twice as much as the S&P 500's (SPY) yield.

Is Intel Stock Likely To Split Again

In 2020 and 2021, stock splits have gotten a lot of attention, as huge companies such as Apple (AAPL) and Tesla Motors (TSLA) did them, while there was also speculation that Amazon.com (AMZN) could be interested in doing a stock split. Not too long ago, NVIDIA, one of Intel's main competitors, did a stock split as well.

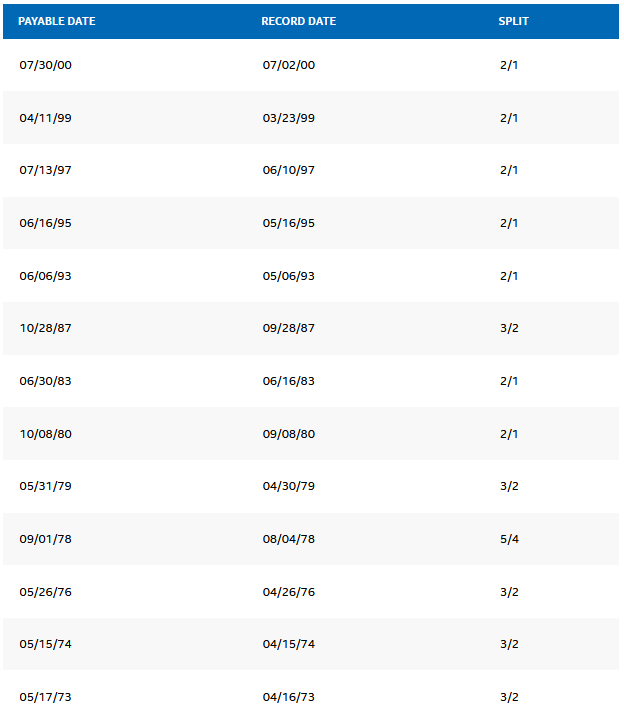

Some readers are interested in knowing whether Intel might do a stock split as well, which is why we can try to gauge the pros and cons of that. Let's first look at Intel's stock split history:

Source: Intel Corporation

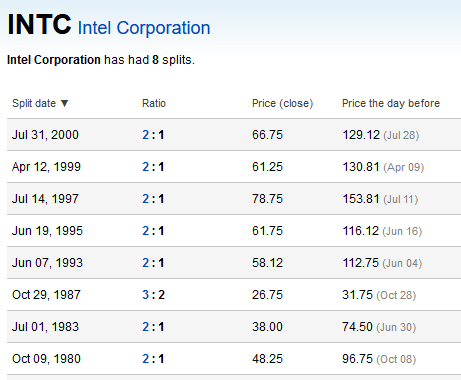

We see that the company has done stock splits repeatedly in the past, with a total of 13 stock splits recorded on the company's website. Clearly, the company has not been reluctant to split its shares in the past. At the same time, however, we can also note that the series of stock splits stopped in 2000, i.e. a little more than two decades ago. Not a single stock split was recorded since then, which means that the company has seemingly seen no good reason to split its stock since then. When Intel did its last stock split in 2000, its shares were trading at well above $100 and as high as $150 at some point. In other words, when Intel did its last stock split, its shares were trading with a relatively high nominal price, which was, of course, the result of the dot.com bubble during which Intel saw its shares explode upwards. Since then, shares have not regained their former strength, as they continue to trade below their highs from back then -- even following the 2-1 split that occurred in July 2000.

When we look at other stock splits, we see a similar pattern:

Shares did trade for well above $100 before other stock splits as well, e.g. in 1999, 1997, 1995, and 1993. Adjusted for inflation, that likely pencils out for roughly $200 in today's dollars. When we compare these prices to Intel's current share price, it looks like there is one good reason for Intel's decision to not split its shares in the last twenty years --they are too cheap for a split. In the past, Intel split its shares regularly when they rose to levels well above $100, but since shares are far from that level today, there just is no good reason to conduct a stock split right now.

In an age where fractional shares can be bought easily through most brokers, stock splits have become less important overall. However, there are still some advantages to stock splits, e.g. when it comes to index inclusion, or when it comes to the ease of using options. With Intel's shares trading in the $50s, however, these arguments are not really valid, and one can summarize that there would not be any clear benefit from a stock split. Therefore, I doubt that Intel will do a stock split in the near term, at least unless its shares rally massively. Intel has a share count of roughly 4 billion today, which is a pretty large number already, and there is no real benefit from doubling that number by cutting the share price in half. Over the last decade, this number has dropped from around 5.3 billion to where it stands right now, but Intel would need to repurchase shares for many more years before the share count drops to a number that could be called "too low". For now, I thus believe that a stock split is unlikely, and that also holds true for the foreseeable future. It is, of course, possible that Intel does a stock split a decade from now if it manages to regain its footing in major markets and if its profitability and valuation improve. In that case, shares could eventually rise well above where they trade today, which may result in a stock split. Future stock splits are thus not ruled out completely, but it looks like there is no reason to do one in the near or medium term.

INTC Stock Forecast

Wall Street analysts have a stock price target of $63 over the next year, which, combined with the dividend, would result in total returns of more than 20%, which would undoubtedly be attractive. At the same time, however, the consensus rating on the stock isNeutral, which may mean that analysts are not too convinced that their models are very precise.

Looking at Seeking Alpha's Quant Rating on the stock, we see a reading of 3.46, which is Neutral as well, although bordering on the edge of Bullish. The main issue for Intel's Quant score is its weak growth, which offsets the very strong value rating. Intel's strong value rating isn't a large surprise, as shares are valued at just 11x forward profits, which compares very favorably to the likes of AMD (43x forward earnings) and NVIDIA (49x forward earnings).

Intel has, despite its strong profitability and large size, not been able to really capitalize on the growth of the global chip industry. Process delays and market share losses in high-value areas such as data centers have led to underperformance when it comes to profit growth versus its peers, and it looks like this will not change in the very near term. 2021 will be a flat-to-down year, and 2022 will likely not see any meaningful profit growth, either. Growth investments in Arizona and potential new multi-billion dollar plants in the US should positively impact Intel's growth eventually, but these investments will take years before starting to generate profits -- this will not help Intel improve its position in 2021. A while ago I estimated Intel's return potential in the high-single-digits range for the long run, with about one-third of that coming from the dividend. This is far from bad, and I assume that holding Intel will not be a bad decision at this time. I don't think that Intel must necessarily be an outrageously strong buy today, however -- investors may want to wait for even lower prices (looking at Intel's chart, this happens from time to time), or wait for a clearer picture about Intel's future, e.g. when it comes to the question of how well the company is doing with its new processes.

Is Intel Stock A Buy, Sell, Or Hold Right Now?

Intel, overall, is still a leading semi company when it comes to output, revenue, cash generation, and R&D power. Its new CEO Pat Gelsinger seems to be making the right moves to position the company for the future, but at the same time, Intel is a pretty large ship to turn around, and for now, others such as NVIDIA seem to be leaner and more agile. Investing in Intel could pay off handsomely if the company gets back on growth track a couple of years from now, as this would leave a lot of multiple expansion potential. A successful turnaround towards stronger profit growth is not guaranteed, however. The near-term outlook is thus not very strong, although the low valuation could still leave upside potential if sentiment about Intel's future plans improves. In the longer run, Intel has opportunities to deliver shareholder gains, but the outlook is still clouded and uncertainties about execution remain. For now, we are neutral on Intel.

精彩评论