Summary

- Apple's new chips, the M1 Pro and the M1 Max, are very powerful and energy-efficient at the same time.

- Getting rid of Intel and taking control of the chips it uses fits well with Apple's strategy, and its products will become more attractive.

- Overall, Apple still doesn't look like a great buy today, mainly due to a too-high valuation.

Article Thesis

Apple(NASDAQ:AAPL)has been increasing its focus on developing and using its own silicon for its laptops. Thanks to strong performance metrics and excellent power/performance ratios, these new chips, such as the M1 Pro and the M1 Max should help improve the value proposition of Apple's MacBooks, which could lead to higher market share. MacBooks aren't Apple's most important product by far, but over the years, moving away from Intel(NASDAQ:INTC)should still be an incremental positive for Apple.

Did Apple Use Intel Chips?

Apple's Macs had been using Intel processors for 15 years, but that has changed with recent new Mac and MacBook releases. In 2020, Apple has showcased laptops and a Mac that use its own chip, the M1, for the first time, ending the partnership with Intel that had been running for well over a decade. Intel's chips had been using the X86 technology, whereas the chips that Apple develops utilize the ARM architecture -- the one that it also had been using for its iPhone and iPad chips for a long period of time. In the past, ARM-based chips had not been powerful enough for the more demanding applications and use cases that play a role for PCs. Apple has now, however, closed that performance gap, which allows them to use its own ARM-based silicon to power its Macs and MacBooks in the future.

What Are Apple's Newest Chips?

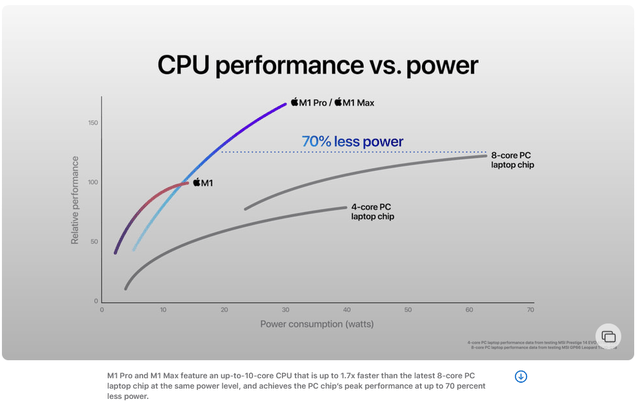

In the laptop and PC space, Apple's newest chips are the M1 Pro and M1 Max, following up on last year's M1 chip. These new chips are being offered in the MacBook Pro and,presumably, in the 2022 MacBook Pro. These chips do, according to Apple, provide an unprecedented performance relative to the power they consume:

With up to 10 CPU cores, up to 32 GPU cores, and up to 64 GB of shared RAM, Apple's newest chips offer outstanding performance. As we can see in the above chart, this performance is achieved at considerably lower power consumption relative to current chips by competitors. This is especially important when it comes to Apple's MacBooks, as power consumption is highly important for laptops. Not only does lower power consumption lead to lower operating costs, but the laptop can also be constructed with lower battery capacity, all else equal, which translates into an improved form factor and lower weight. This, in turn, will make the new laptops more user-friendly, which should attract more buyers and help Apple expand its market share.

Why Is Apple Transitioning Away From Intel Chips?

There are several reasons for Apple's decision to move away from Intel and to develop its own chips for its laptops and PCs. First, this move gives Apple more control over core technologies and makes the company less dependent on suppliers. If Apple wants to make changes to its chips it can easily do that and put the engineering focus where it sees the biggest potential gains or benefits. While Apple was using Intel's chips, it was dependent on smart R&D by Intel, and thus not in control. This fits well with Apple's strategy that is sometimes called the Tim Cook Doctrine. The CEO has explained that Apple has a “long-term strategy of owning and controlling the primary technologies behind the products that we make.”Getting more control over the chips it uses in laptops and PCs is just a relatively logical step for a company that seeks to increase its ownership in key technologies for its products in order to become more dominant and less dependent on suppliers over time.

On top of that, technological progress has allowed ARM chips to increase their performance relative to X86 chips over the last couple of years. Due to the better efficiency of these chips and the huge benefits this efficiency guarantees in the notebook space, it is logical for Apple to pursue ARM-based chips instead of Intel's X86 architecture as this allows Apple to craft a better overall product.

In short, there are thus both strategic reasons for Apple to move away from Intel, while there are also technical reasons that make ARM-based chips look favorable relative to what Apple was able to buy from Intel.

Apple Stock Forecast

With the introduction of the most recent high-powered and highly efficient chips, Apple should be able to strengthen its position in the higher-end laptop and PC space over the coming year, and likely beyond, as the company will continue to improve its chips going forward.

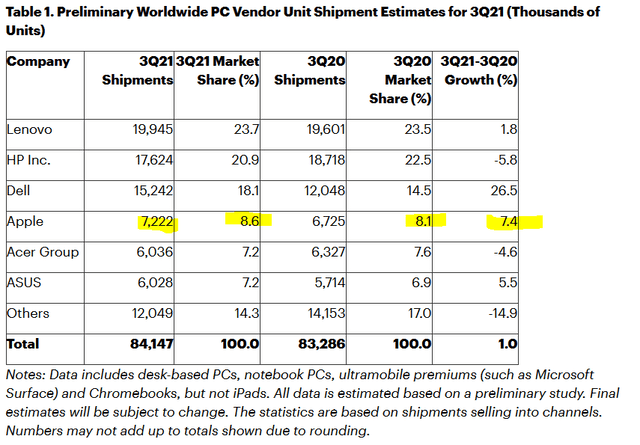

The market for PCs has been relatively strong in 2020 and 2021, on the back of more people working from home. On top of that, distance learning, due to school closures, and more demand for home entertainment, due to lockdowns that reduced the availability of out-of-house entertainment choices, have been beneficial for the global PC market over the last one and a half years. Gartner states that PC shipments rose by 1% during the third quarter, on top of a 4% growth rate in 2020, which had been the best year over the preceding decade. Gartner also estimates that Apple was the number four company in global PC market share, with an 8.6% market share:

Apple was able to grow its market share by 50 basis points, which allowed the company to grow its overall sales by 7%, which was well above the overall market growth. Thanks to the introduction of its new and highly capable chips, it would not be a surprise to see Apple gain further market share in the coming years.

Apple's PC and laptop business is, however, not overly large relative to the company's overall size. This is why solid growth in the PC space will not necessarily lead to huge growth for the company overall. Apple is highly dependent on iPhone sales as those make up the majority of the company's revenue and profits. Apple recently had to announce that it would cut iPhone 13 shipments by 10 million in Q4 due to part shortages, which doesn't bode too well for the company's near-term outlook. Once part shortages have ended, production should expand again, but the iPhone business nevertheless isn't a high-growth franchise.

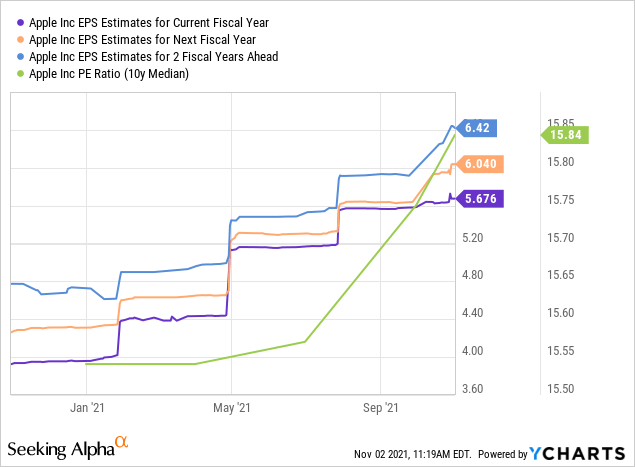

With much of the top line being dependent on the lower-growth iPhone business, it is not too surprising to see that analysts aren't predicting a lot of growth for Apple going forward:

For the current year, analysts are predicting a 4% revenue increase, with a 5% top-line improvement being expected for the following year. Beyond that, however, growth is forecasted to decelerate. It is, of course, possible that Apple will outperform expectations, but it should be noted that the company actually missed estimates for the most recent quarter, breaking a very solid record of beating estimates. It is thus not guaranteed that Apple's actual performance will be better than the ~3% annual growth that analysts are forecasting today.

In the past, Apple has been able to grow its earnings per share way quicker than its revenue, thanks to margin improvements and the impact of buybacks. Buybacks will continue to have a positive impact on Apple's earnings per share growth, but most likely not at a similar magnitude compared to what we have seen in the past. When Apple was trading at 10-15x net profits, its buybacks had a lot more power, and the company was able to lower its share count pretty quickly. Today, with shares trading at 26x forward earnings, its share repurchase program is less impactful, as fewer shares can be bought back. This, in turn, leads to a smaller share count decline, which results in less pronounced earnings per share growth tailwinds. Overall, Apple should still be able to grow its earnings per share relatively reliably in the future, but I do believe that the current valuation could be too high for the growth that one can expect going forward.

Analysts are currently predicting that Apple will earn $5.70 during the current fiscal year (which ends in September 2022), while earnings per share for the following two years are seen at $6.04 and $6.42. This pencils out to a growth rate of around 6% over these two years, which isn't disastrous at all, but it's also far from excellent. When we consider that Apple trades at 26x forward earnings today, while the median earnings multiple over the last decade is just 16, then Apple does not look like an exciting investment, I believe.

Is Apple Stock A Buy, Sell, Or Hold?

In the very long term, an investment in Apple will in all likelihood generate positive returns. Those could still be at a level that isn't especially attractive, however. With Apple entering a phase of somewhat subdued growth, while shares are historically expensive, I believe that the total return outlook isn't too great with shares trading at $150.

Apple will likely make gains in the PC space, but this alone will not be enough to move Apple's top line by a large amount, due to the fact that the PC and laptop business is relatively small in comparison to the much larger iPhone business. With some revenue growth and the impact of buybacks, 6%-10% annual earnings per share growth seems achievable, but I don't think that paying more than 25x forward earnings for that growth makes for a great investment proposal. Overall, I think Apple is aHoldat current prices, due to its relatively high valuation.

精彩评论