Summary

- Nvidia is an undisputed leader in the semiconductors space, with one of the most profitable business models.

- Investors' focus is usually put on the company's strong product roadmap, which is now less relevant for the share price performance.

- Due to its unique positioning, Nvidia's share price is now more sensitive to market-wide forces than it is to the company's business fundamentals.

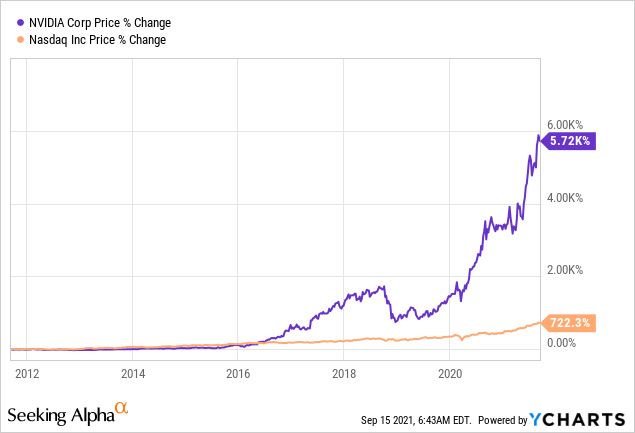

From a relatively small gaming company a couple of years ago, Nvidia (NVDA) has turned into one of the most important technological enterprises globally. From data centers & cloud computing, driverless cars and all kinds of artificial intelligence computing workloads, to gaming, visualization & cryptocurrency mining, Nvidia products are now the lifeblood of the new digital economy.

Not only is Nvidia's intellectual property uniquely positioned within the new digital age, but the company is also an undisputed leader in the graphics processing unit(GPU)space with a very wide moat. This led to the success story called Nvidia.

Going forward, however, share price returns are likely to disappoint even in the face of improving business fundamentals. It appears that certain market-wide risks are now in the driver's seat of Nvidia share price and could catch many of Nvidia shareholders off-guard. But before we dig into that, we need to properly account for the leading position business potential of the company.

All about GPUs demand

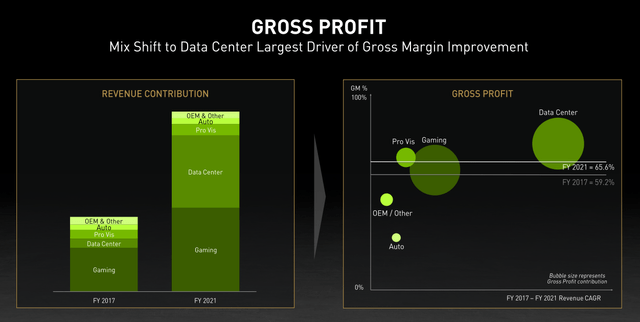

Even though the Gaming segment still takes a sizeable proportion of Nvidia's business, just over the course of four years Data Center has become equally important in size.

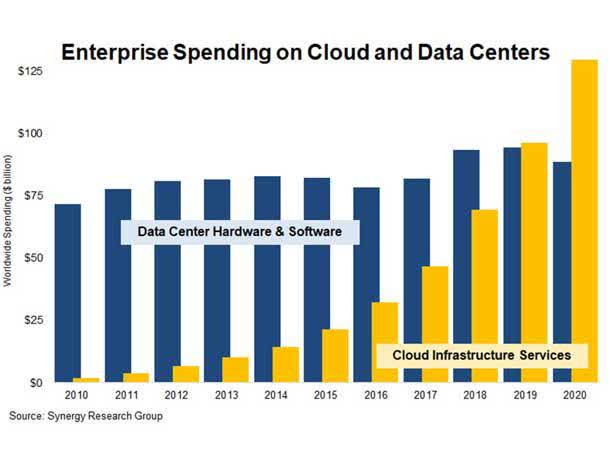

As if the already ongoing trend towards more cloud-based workloads was not enough, the current pandemic significantly accelerated the overall demand.

In addition to data centers, the automotive industry is also starving for Nvidia's chips which made the company deeply embedded in the automotive ecosystem.

NVIDIA is working with several hundred partners in the automotive ecosystem including automakers, truck makers, tier one suppliers, sensor manufacturers, automotive research institutions, HD mapping companies, and startups to develop and deploy AI systems for self-driving vehicles.

Source: Nvidia Annual Report 2021

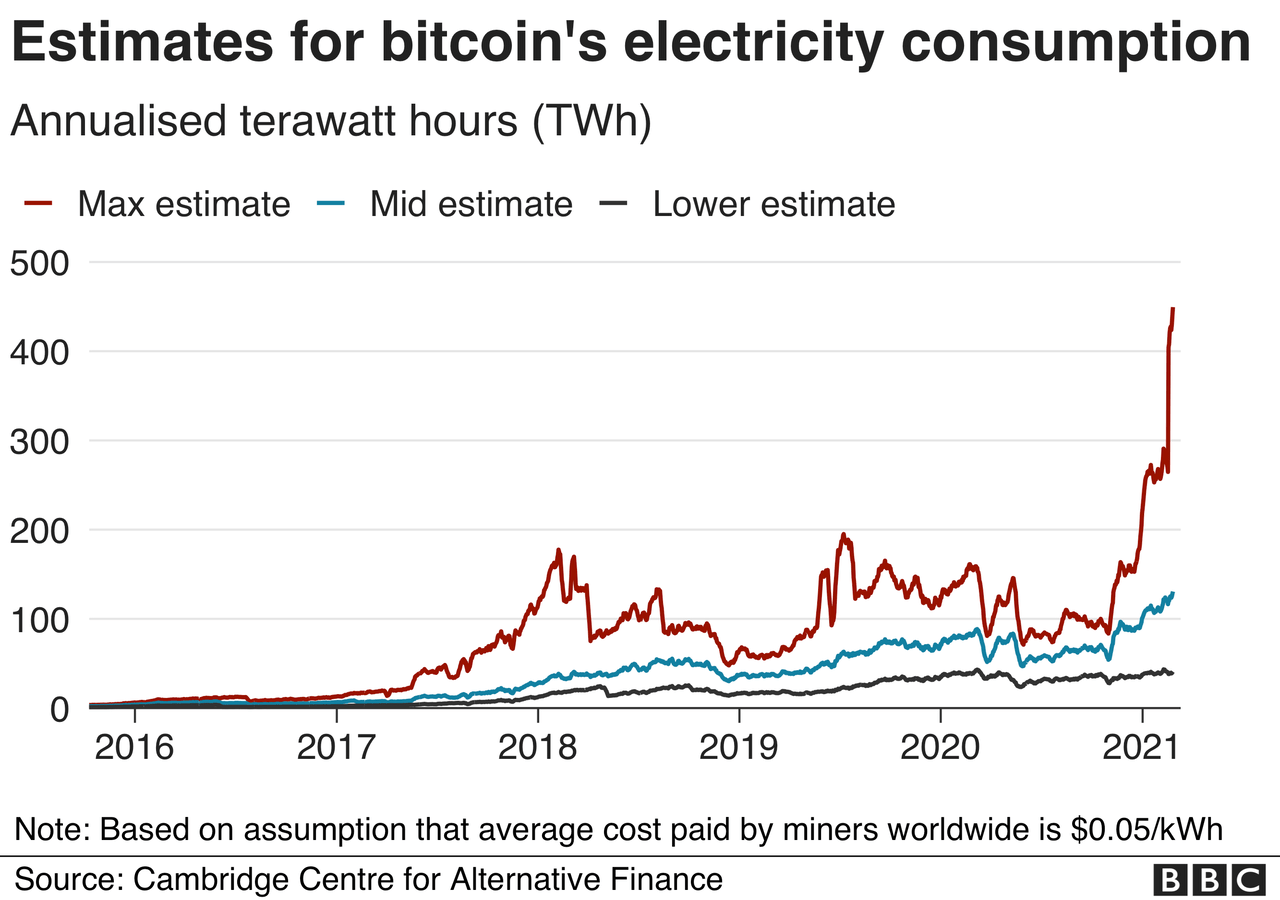

Last but not least, the tug-of-war between gamers and cryptocurrency miners has resulted in both higher volume sales as well as higher pricing of Nvidia's GPUs. The uptick in energy consumption for cryptocurrency mining, coupled with the overall preference for Nvidia GPUs was yet another tailwind for the company's Gaming division.

Implications for the Income Statement

The perfect storm for GPUs demand and Nvidia's leading position in the segment resulted in the 53% topline growth in fiscal year 2021 and 31% so far for the FY 2022.

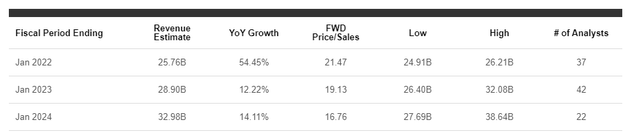

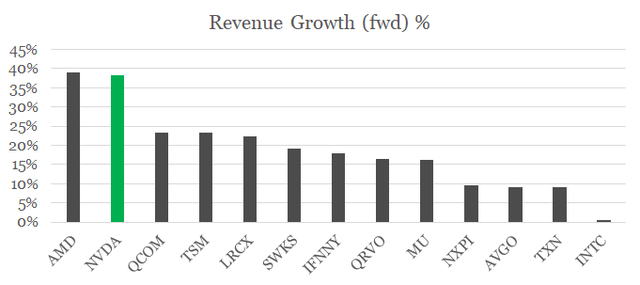

Going forward, NVDA is likely to sustain this high topline growth rate, which is expected to somehow cool-off following fiscal year 2022.

The forward growth rate of NVDA is comparable only to that of its other GPU rival - AMD (AMD), which is expected to grow at a similar rate over the next two fiscal years.

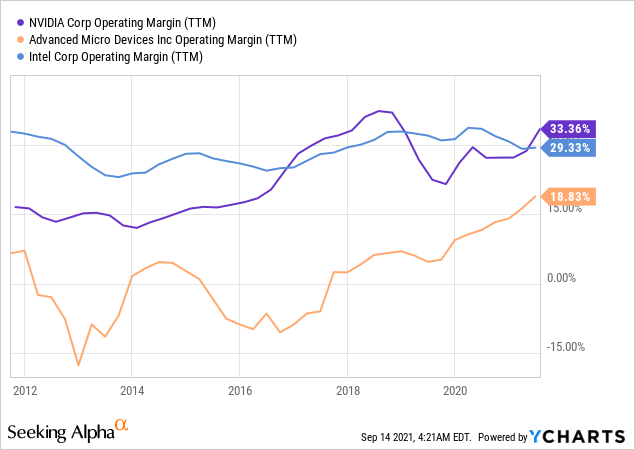

However, while AMD's share price benefited massively from the strong GPU demand and its recent comeback to the CPU stage, Nvidia retained an industry-leading profitability.

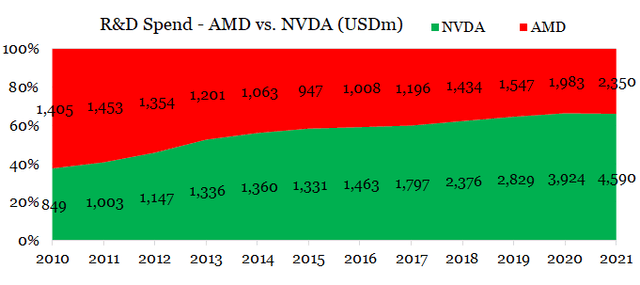

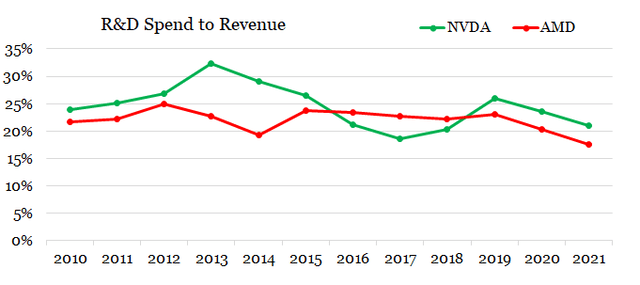

This allowed NVDA to spend significantly more than its rival AMD on Research & Development expenses.

Even adjusted for size, Nvidia has also been consistently outspending AMD on R&D investments.

While organic growth opportunities for Nvidia might seem endless at this point in time, the semiconductors industry remains highly cyclical and sooner or later even the GPU demand will cool off.

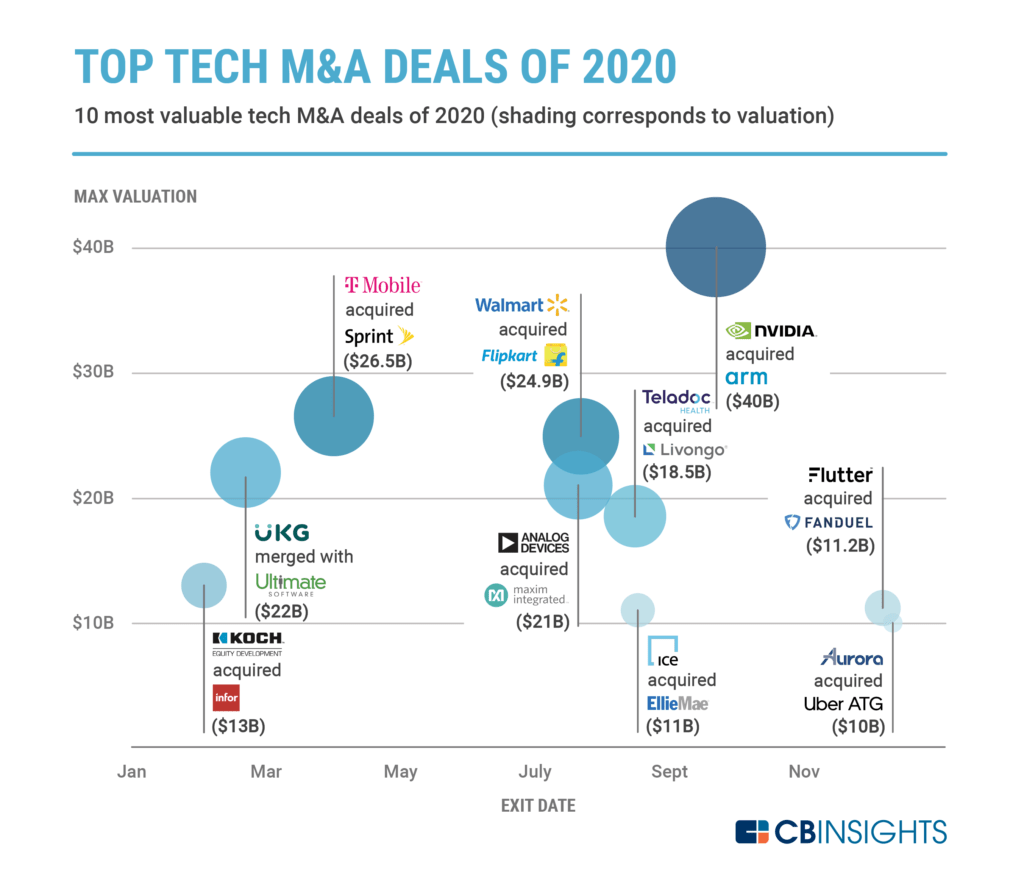

That is why, even in the midst of the GPU shortages, Nvidia management is capitalizing on its extremely high valuation by tapping into the strategic acquisition of ARM.

Under the terms of the transaction, which has been approved by the boards of directors of NVIDIA, SBG and Arm, NVIDIA will pay to SoftBank a total of $21.5 billion in NVIDIA common stockand $12 billion in cash, which includes $2 billion payable at signing.

Source:nvidianews.nvidia.com

The ARM deal, which is still under review by the regulators, was also one of the largest Tech deals for 2020.

In addition to high M&A activity being a sign of a peak in market valuations, analysts' sentiment on Nvidia is also exceptionally optimistic which suggests that the near-term growth is already priced in.

The value conundrum

As rosy as everything seems for NVDA right now, there should a price that is simply too high even when accounting for Nvidia's strong positioning. So far as growth accelerated so did the company's P/E ratio, which suggests an even more optimistic future scenario. However, neither Nvidia's bottom line nor its earnings multiple can go on an upward trajectory forever.

After everything we said so far, we have some solid reasons to believe that the earnings per share (EPS) growth will be sustained for the time being, even in the face of the cyclical nature of the industry. But at such high valuations, the price premium attached to EPS growth is far more important for future returns. In other words, Nvidia's bottom line could fulfil even the rosiest forecasts but the share price could still disappoint, if the premium paid for high growth decreases.

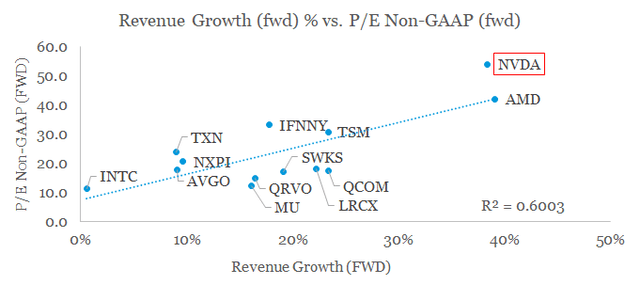

As we saw earlier, right now both NVDA and AMD are the two highest growth names in the semiconductors peer group and as such are rewarded by a proportionally higher earnings multiple.

Due to Nvidia's leading positioning and higher profitability, the company lies above the trend line on the graph above.

Interestingly enough, if we exclude the high-flying GPU companies, the R-Squared between the rest of the peer group is just 0.12 which means that there isn't a strong relationship between future growth and valuations for everything other than GPUs in the semiconductors space.

This is due to the fact that NVDA and AMD chips are expected to have a more sustained growth beyond next year as GPUs remain crucial for data centers, autos, digital currencies and a number of other workloads related to artificial intelligence (AI).

This also means that NVDA and AMD are among the highest duration stocks in the sample and as such the most sensitive to changes in interest rates. Meaning that all else being equal, NVDA and AMD shares will be hit much harder than those of their peers in an event of rising interest rates.

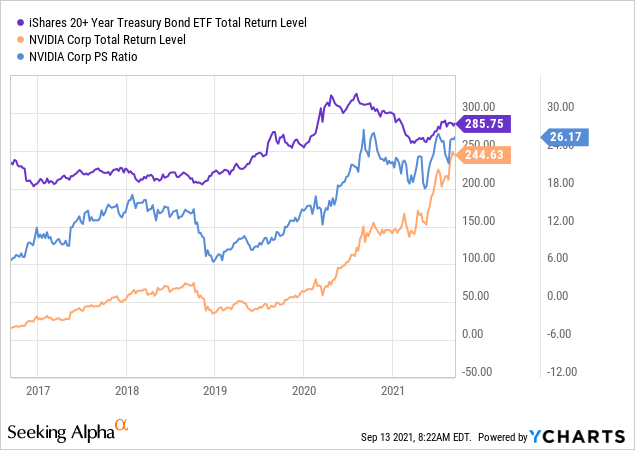

That is why, NVDA Price-to-Sales ratio trails the performance of iShares 20+ Year Treasury Bond ETF (TLT), which is influenced by long-term bond yields.

In the graph above, the TLT does a very good job at explaining movements in Nvidia's P/S ratio, with the exception of the last quarter of calendar year 2018, when crypto-related demand had a profound impact on the company's topline results.

Three factors contributed to the Q4 gaming revenue decline. First, post crypto inventory of GPUsin the channel caused us to reduce shipments in order to allow excess channel inventory to sell through. We expect channel inventory to normalize in Q1 in line with one to two quarter timeline we had outlined on our previous earnings call.

Second, deteriorating macro economic conditions,impacted consumer demand for our GPUs; and third, sales of certain high end GPUs using our new Turing architecture, including the GeForce RTX 2080 and 2070 were lower than we expected for the launch of a new architecture.

Source: Nvidia Q4 of FY 2019 earnings transcript

This also highlights the sensitivity of Nvidia share price to macroeconomic conditions in cryptocurrency-related demand as the share price halved from around $70 in September 2018 (4-to-1 split adjusted) to around $35 in January of the following year.

The elephant in the room

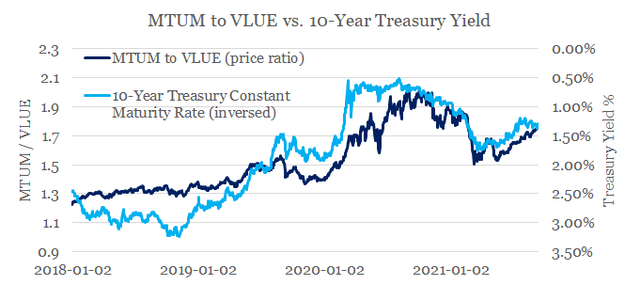

The unprecedented amount of liquidity within the equity markets has been a blessing for high growth momentum stocks, which was one of the best performing areas of the market over the last decade. That is why it is worth noticing that lower interest rates have profound implications for returns of momentum stocks (see the graph below).

In the graph below I measure momentum by taking a long position in the iShares Edge MSCI USA Momentum Factor ETF (MTUM) and a short position in the iShares Edge MSCI USA Value Factor ETF (VLUE).

After everything we said so far, it should come as no surprise that momentum stocks were one of the best performing areas of the market during 2020, when nominal yields on the 10-year government bonds fell below 1%. During this period, Nvidia share price more than doubled from around $60 (post-split) in January to $130 in December of the same year. And although the company does not make it into the largest holdings of MTUM, its share price was heavily influenced by the performance of the momentum factor.

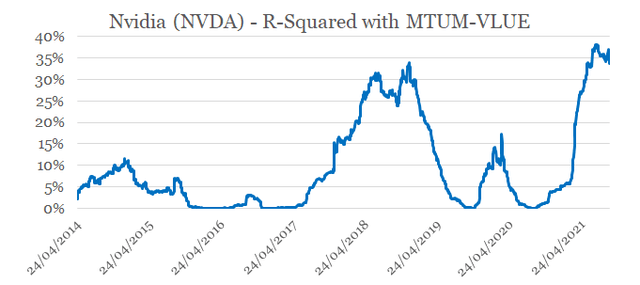

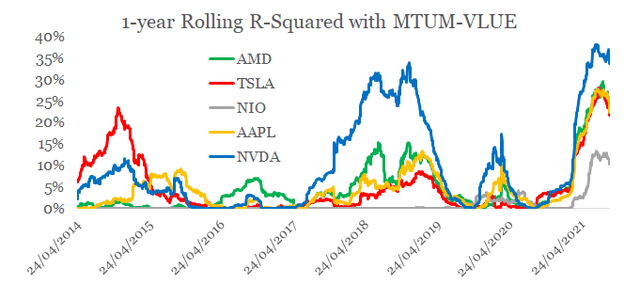

Nvidia's relationship with momentum factor (MTUM less VLUE) has become an even stronger over the recent months as its share price reached new all-time highs, with the rolling 1-year R-Squared of daily returns hovering above 0.35.

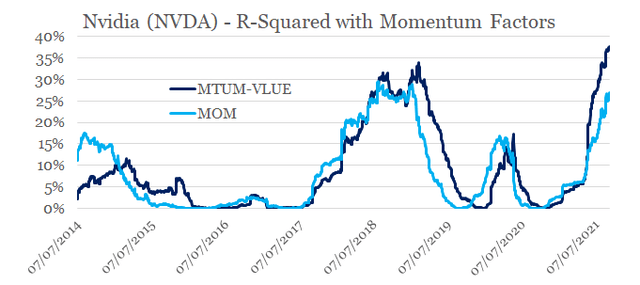

Since this might look as a coincidence, the relationship between NVDA and the momentum factor, as constructed by Fama & French, also followed a similar pattern to the one used above.

Nvidia's exposure to the momentum factor is also much stronger than those of other high-flying growth names, such as AMD, Tesla (TSLA) and NIO (NIO).

Nvidia was one of the growth stocks that benefited the most from the recent drop in interest rates and as such is at the highest risk of a sharp reversal, should bond yields normalize. Adding the risk of lower demand from cryptocurrency mining, and the prospects of Nvidia share price continuing to outperform look slim. That is why, investors should not be surprised, if going forward Nvidia share price disappoints even as management continues to deliver on its strategy.

Of course, there is always the possibility that the Federal Reserve will be unable to taper and bring bond yields to a more normalized level, which in itself will be enough to propel Nvidia's share price to new all-time highs. Nevertheless, this is a highly uncertain event that is also unrelated to Nvidia's business performance. Moreover, the outcome of this event will likely have a disproportionately higher influence on Nvidia's future share price performance than the company's products will.

精彩评论