Summary

- Palantir’s valuation is impossible to defend.

- Palantir will remain dependent on government for income.

- The private sector opportunity is over-hyped.

Palantir (PLTR) is a software business with one of the most ridiculous values in the stock market today. Palantir has developed into a valuation that neither makes sense nor is supported by concrete business results, despite its growth opportunity in AI-assisted software analytics.

Palantir: Heavily Dependent On Government

Palantir must be one of the most overvalued stocks in history because it ticks all the conditions. Palantir manages to trade at a market value of $43 billion by specializing in surveillance, big data, and having the US government as a client. After the company issued its shares on the exchange through a direct listing, its market value was significantly larger than $43 billion. Insiders of a corporation sell shares while the company receives no money in a direct listing.

Instead, an IPO raises funds to invest in the company. Roughly a year ago, Palantir’s shares started trading at $10 a share. The stock, and the market capitalization, have proven highly volatile, as the stock price surged as high as $45. PLTR has since settled for a trading range of $20 - $30 and the company, as well as its business model, continues to attract a great deal of interest and attention.

Palantir Has One Of The Best Features A Stock Can Have: A Sexy Story!

Palantir is right in the thick of a massive money-making opportunity: big data analytics. Information, or data, is a valuable commodity, and the ever-increasing speed with which businesses are embracing full digital transformation makes for a compelling story. Palantir's principal business is to assist organizations, particularly governments, in sifting through massive volumes of data in order to forecast and enhance decision-making. In the corporate realm, this can mean increasing conversions, whereas in government, it might mean supporting public health measures or assisting the US military in dealing with bad guys.

Palantir is collaborating closely with the US government in a number of ways, and in exchange, Palantir is getting a lot of federal cheese. The company recently obtained an $823 million deal with the US military to assist in the development of data architecture for intelligence systems.

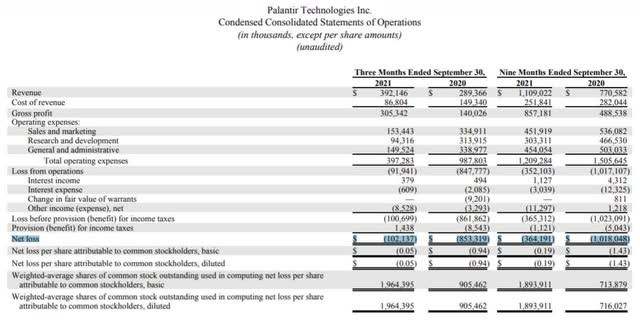

Palantir's revenue is rapidly increasing, but keep in mind that the company is primarily reliant on governments. Revenues from government bodies have increased by 57% year-to-date, to $658.4 million. Revenues from companies were reported as $450.6 million, compared to $350.3 million a year ago. Relative revenue contributions of the government and the private sector were 59% and 41% and last year, 55% and 45%. These percentages tell an important story deserving to be clarified, as they contradict the prevailing narrative.

The prevailing narrative is that Palantir will move away from the government business and generate significant growth in the private sector. Expanding on the above-mentioned percentages, Palantir’s reliance on government has increased in 9M 2021, compared to 9M 2020, and government revenues are growing at a much faster rate than revenues sourced from the private sector.

Persistent Losses Despite Soaring Revenues

Palantir's long-term growth possibility in big data is frequently mentioned in bullish analysis, and with good cause. We've all learnt this through the rise of Metaverse Platforms (FB), which was one of the first corporations to collect massive amounts of data in order to monetize its customers. Palantir does have attractive growth prospects: It just reported that 3Q revenues were up 36% to $392 million, and the company expects an annual revenue growth rate of 40% for the year. The company has also stated that it expects at least 30% revenue growth from this year until 2025. While I do not contest that Palantir has potential for revenue growth, there are concerns I think are inadequately reflected in the company’s valuation.

One anticipated issue is that, while Palantir may be experiencing considerable revenue growth, how much of that increase actually reaches Palantir's shareholders? The answer, not a lot. Reviewing the last filing of financial statements, we can see that despite an eye-popping sales increase of 44% year-to-date, Palantir is not anywhere close to generating profits. Losses in 3Q were $102.1 million and the loss year-to-date is $364.2 million.

Palantir's lack of profitability is a major issue, and I keep asking myself, "How long will shareholders tolerate Palantir losing so much money every quarter?"

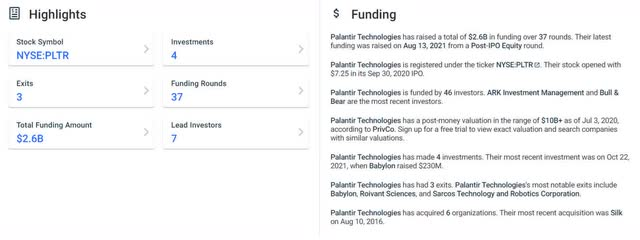

The fact that Palantir is not a startup adds to my concerns (which would be a feasible justification for losing so much money). Palantir, on the other hand, which was formed nearly two decades ago and has raised an estimated $2.6 billion in funding, continues to lose money. This is a track record that I find difficult to justify, particularly given Palantir's present multiple.

What Are You Paying For, Exactly?

Palantir is doing an excellent job of presenting its potential, and the stock has a growth stock feel to it.

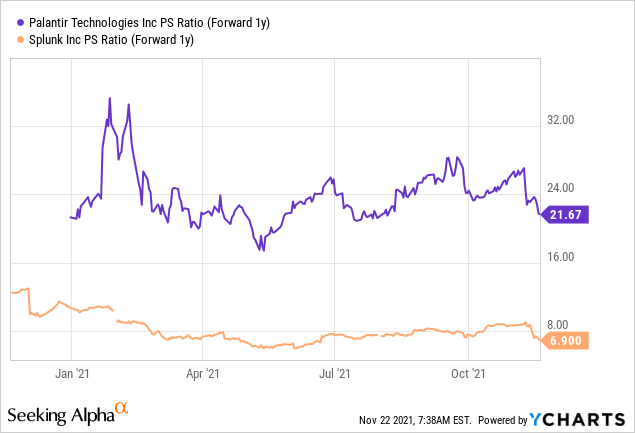

But since profits are not showing up on the profit statement after nearly two decades of operations, why exactly are investors paying a multiple of 28? Not even Netflix (NFLX) gets a multiple of 20 and it has been one of the fastest growing companies not only in the U.S., but in the world over the past two decades. The multiple is very hard to defend and not fitting for a company that is growing sales quickly.

On that note, Palantir isn’t exactly doubling sales every year. A 30% growth rate is good, but not impressive. And why would anyone want to overpay for Palantir’s sales growth, if competitors such as Splunk (SPLK) can be acquired for far lower sales multiples?

A Few Words on Risks

Palantir is growing revenues at around 30% annually, but if this growth can be maintained over the long term is another question. Also, can Palantir really turn a profit in the future, and if so, when? Why Palantir receives such a high multiple is beyond me. The big data company is one of the most overvalued and overhyped I've ever seen, which is why I consider Palantir's biggest risk as the excessively inflated multiple.

My Conclusion

It's absurd to pay 28 times revenues for a company that is losing money. The potential for revenue growth is undeniable; after all, big data is big business. However, after two decades of operations, shareholders should be able to expect a little more from Palantir, particularly management, in the form of profits or stock buybacks, or something similar. Palantir has done a fantastic job benefiting its selling shareholders, yet there is no deal to be had because there are no earnings. Palantir's valuation is a fairy tale, and like all fairy tales, it ends in a nasty awakening.

精彩评论