Summary

- Shares of Beyond Meat have crumbled more than 40% from highs.

- The company has been plagued by a number of issues, including slowing growth and a decaying margin profile.

- Retail velocity is declining, suggesting that Beyond Meat's pandemic arguments of limited in-stocks have faded.

- The stock remains expensive against long-term profit expectations.

These days, the market certainly has no shortage of expensive growth stocks that have very little substance. One stock that I think is at particular risk of crumbling further is Beyond Meat (BYND), one of the first purveyors of the faux-meat trend and one of the most recognizable brands in the space.

Despite the growing appeal of plant-based meats, I continue to see huge fundamental flaws in this stock. The market seems to agree, as Beyond Meat shares have slid by roughly half relative to all-time highs around ~$200 notched last October.

In my view, Beyond Meat shares have even more downside left. I continue to cite that there's a "story" risk to Beyond Meat: plant-based meats are popular now, but are they a passing dietary fad? The list of diet fads is a long one, ranging from keto diets and paleo diets to complete-nutrient drinks like Huel. While Beyond Meat may find itself a core customer base, I view the category's growth to be limited especially with concerns that plant-based meats are unhealthy from a sodium angle.

Yet there are shorter-term risks here, too. In particular, investors should be aware that Beyond Meat's growth and demand indicators have weakened in recent quarters. Profit margin slippage is another big concern, especially when the stock is still trading so expensively as a multiple of outer-year profits.

The bottom line here: Beyond Meat is a spoiling stock, and I think there's little the company can do to get back on the right track.

Slowing growth, decaying velocity

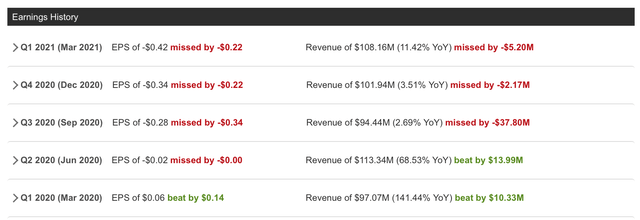

The first thing investors should note is that Beyond Meat has missed Wall Street's expectations for three quarters in a row. It's a small wonder that the stock has landed in investors' "penalty box" - in a time when a reliable "beat and raise" cadence has become expected for growth stocks, Beyond Meat's earnings gaffes are a huge sore spot.

In Beyond Meat's most recent quarter (Q1), the company saw relatively tepid 11% y/y growth to $108.2 million in revenue, missing Wall Street's expectations of $113.3 million (+17% y/y) by a huge six-point margin. As shown below, that's an even wider miss than the $2 million gap to expectations in Q4:

Figure 1. Beyond Meat earnings vs. expectations

At a channel level, in Q1, Beyond Meat its U.S. retail sales grow by 28% y/y, but foodservice sales domestically saw a -26% y/y decline. This is concerning because throughout the March quarter, most areas and restaurants around the country had already lifted lockdown restrictions. We note that the kinds of chain locations that Beyond Meat is typically sold at, from Carls' Jr. to Dunkin' Donuts (DNKN), largely remained open during the pandemic anyway. So Beyond Meat can't really say that lockdowns and the pandemic were to blame for weaker foodservice sales: perhaps the pandemic had ended up ultimately changing consumers' menu preferences toward "real" meat, which is often also substantially cheaper than Beyond Meat.

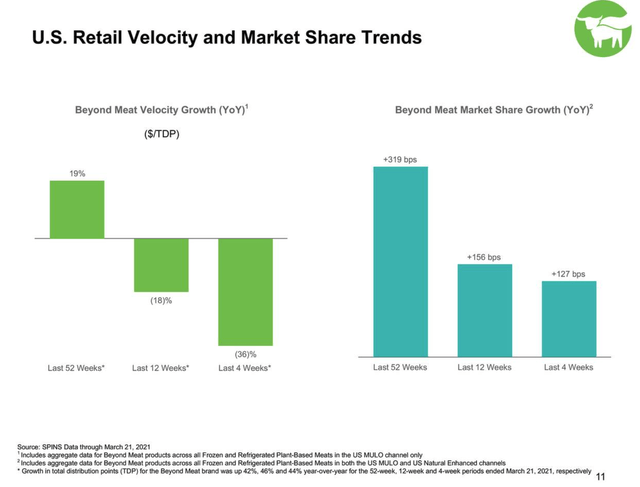

On the retail side, we note that Beyond Meat's velocity is dropping (a measure of how quickly inventory is selling through on store shelves). Beyond Meat argued that during the pandemic, retail sell-through was constrained by limited supply - but now, what you can see in the chart below is that retail velocity has dramatically dropped over the past four weeks. The company noted that on a year over year basis, velocity is down -18% y/y in Q1.

Figure 2. Beyond Meat retail velocity

We note as well that Beyond Meat's market share growth in the retail space has slowed as well. The past four weeks only saw Beyond Meat expanding its market share by 127bps, versus 319bps over the past year.

Margin decay

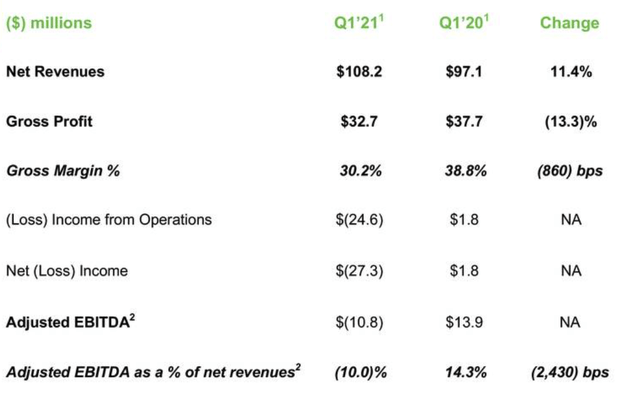

Slowing growth isn't the only troubling indicator for Beyond Meat. The company's gross margin profile, already thin to begin with, is at risk as well. We note that in Beyond Meat's most recent quarter, gross margin slipped to 30.2%, a huge 860bps reduction from 38.8% in the year-ago quarter.

Figure 3. Beyond Meat margin trends

The company cited a myriad of reasons behind the decay. The company blamed the decay on rising storage/warehousing and transportation costs, which is similar to what many other consumer products companies are citing. Even more concerning, however, the company has cited rising fixed overhead costs at its production facilities. And perhaps riskiest of all is the fact that Beyond Meat notes that unfavorable product mix and higher trade discounts have also worked to push margins down.In spite of the fact that Beyond Meat leaned in more heavily on trade discounts to grow sales, the company still saw tepid revenue growth and thinning market share gains.

We note as well that Beyond Meat's adjusted EBITDA gains of $13.9 million from last Q1 turned into a -$10.8 million loss in the most recent Q1, indicating a 24-point decay in adjusted EBITDA margins. We have to wonder: is Beyond Meat structurally set up to be a profitable business?

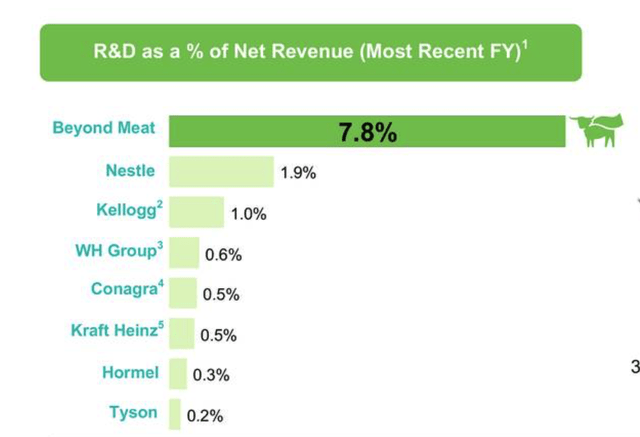

The company likes to tout the fact that it spends ~8% of its revenue on R&D as a positive signal of the brand's innovation. But the other brands shown on the company's below slide are also innovators. Food brands like Kellogg and Kraft Heinz are constantly coming up with new cereal types and new flavors of their existing foods. Beyond Meat doesn't have a sole claim to innovation in the food space - yet it's spending considerably more than its peers on R&D. When we note the fact that Beyond Meat's gross margin is only ~30% to begin with, spending a further 8% of revenue on R&D is a steep ask.

Figure 4. Beyond Meat R&D spend

Valuation and key takeaways

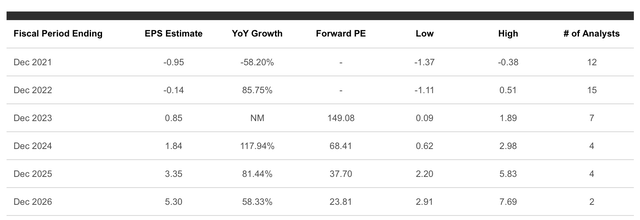

Analysts aren't really expecting Beyond Meat to generate significant profits until years down the road. As shown in the chart below, the company is only expected to pass breakeven in 2023.

Figure 5. Beyond Meat earnings estimates

And even against 2026 earnings expectations of $5.30 per share, and even after Beyond Meat's correction from all-time highs above $200, the stock's current price at ~$125 sits at a steep 23.6x P/E ratio against earnings five years down the line.

With the risks of Beyond Meat's slowing growth and unsteady gross margins, I think the chances of Beyond Meat justifying its current share price (let alone rallying substantially from current levels) are slim.

Continue to avoid this stock.

精彩评论