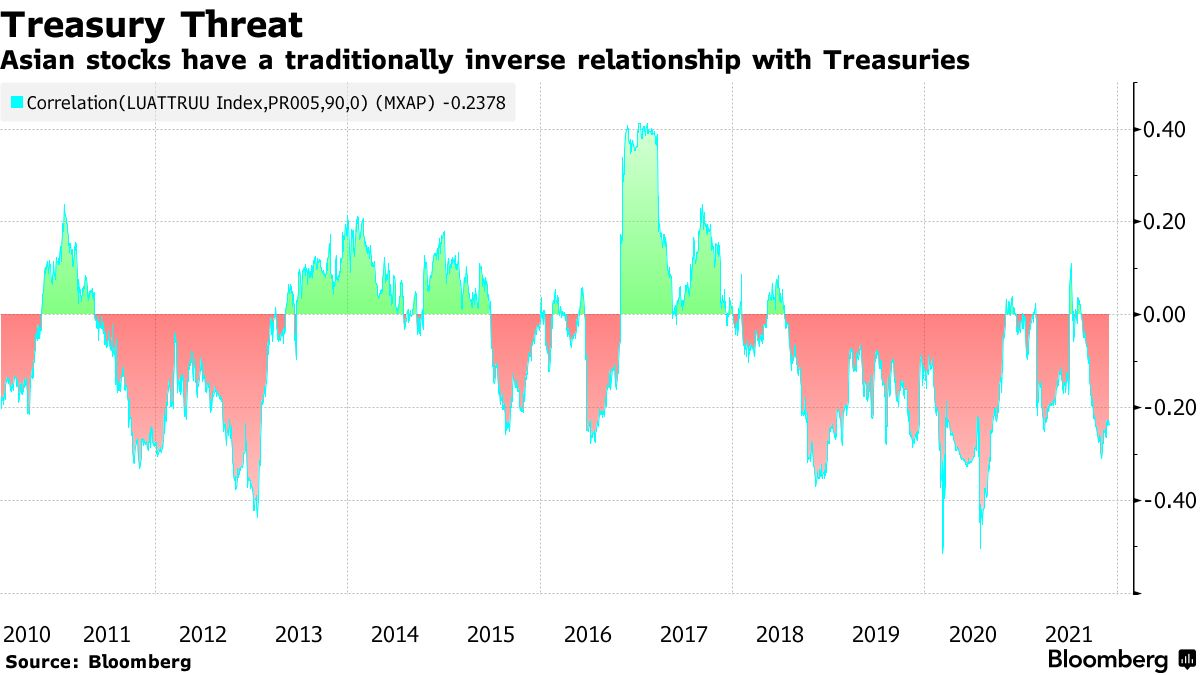

- Strategists bearish on implications for Asia equities and FX

- Higher U.S. rates could trigger capital flows out of region

Jerome Powell sent a stir through global markets Tuesday, paving the way for quicker-than-expected U.S. hikes, which would ripple through rate-sensitive Asian assets.

The Federal Reserve Chair told Congress that policymakers will discuss whether to wrap up bond purchases a few months earlier and retired the word “transitory” from his commentary on inflation. Higher U.S. rates would have a significant impact on Asian assets if capital flows to America. A stronger greenback has implications for Asia’s export-heavy companies and economies and the dollar-denominated debt of the region’s sovereign and corporate borrowers.

Still, Asia stocks and currencies are rallying Wednesday with some strategists saying Powell’s comments about a faster taper weren’t unexpected. His nod toward the uncertainty caused by the omicron variant has also blunted the hawkish tone, according to Tomo Kinoshita, global market strategist at Invesco Asset Management.

Here are the thoughts of Asia watchers on what Powell’s shift means for the region’s markets:

Deferring to the Dollar

“Prospects of quicker taper and higher U.S. rates will stress test the allure of higher returns in EM Asia and as a consequence the ‘stickiness’ of funds parked in this part of the world,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd in Singapore.

“We have long maintained that the outcome will be ‘KokomoFed,’ that gets there fast and then takes it slow after,” he said, referring to a Beach Boys song. “And this in turn will prompt a ‘Kokomo dollar,’ whereby the bias is for the dollar to be skewed to strength.”

Bad for High Beta

“The threat of faster tapering is bad news for high-beta markets such as EM,” said Sue Trinh, managing director for global macro strategy at Manulife Investment Management in Hong Kong.

“Yet we have been of the view that Asia is well-placed within EM to withstand any potential monetary volatility -- inflation in Asia more contained and Asia is less reliant on foreign capital than other EM,” she said. “The not-so-good news for Asia is that the region is far too reliant on foreign demand to absorb its exports.”

Risk Asset Pressure

“Expect more pressure on risk assets in general, including Asian equities,” said Alvin T. Tan, head of Asia FX strategy at RBC Capital Markets in Hong Kong.

“However, Asian FX have held up really well in this latest risk-off bout, and that was because the whole market was furiously loading up on U.S. dollars right into the omicron news,” he added. “So it is U.S. dollars that are being unwound this time. In that way it has been an unusual ‘risk-off’ experience, though JPY has behaved more conventionally.”

Focus on Renminbi

“We expect the Thai baht to be most at risk, especially since it has an additional negative that the re-emergence of Covid-19 concerns will potentially further set back the return of tourism,” said Terence Wu, a foreign-exchange strategist at Oversea-Chinese Banking Corp. in Singapore.

“More importantly, we will be watching closely developments in the renminbi. The RMB has been strong on a basket basis, and that has sheltered the Asian currencies. Should the RMB start to show signs of weakness, expect the flow-through of dollar strength to the EM Asian currencies to be stronger.”

China Chance

“Extreme dollar strength because of higher U.S. interest rates is a headwind for Asia and EM equities, but China and large Asean markets such as Indonesia could still outperform western markets in 2022 because of reversion to mean,” said Michael Rainer Preiss, portfolio strategist at Golden Equator Wealth. “China already had a big correction and the valuation argument for China equities is getting stronger.”

Mixed Asian FX

“While Powell’s comments suggest the Fed could bring forward their rate hike to as soon as the middle of 2022, the dollar failed to rally on the back of this.,” said Khoon Goh, head of Asia research at Australia & New Zealand Banking Group in Singapore. “This is likely because the Fed Chair’s statement is only matching market expectations.”

“The impact on Asian FX will likely be mixed. With export growth still strong in the region, as shown by today’s stronger than expected Korean numbers, currencies of export driven economies like KRW, CNH and SGD will fare well. Prospects for higher U.S. yields could weigh slightly on IDR due to reduced foreign bond inflows. THB will be more influenced by how the Omicron variant may affect Thailand’s tourism reopening.”

Thin Spreads

The spread cushion on Asian dollar bonds from rising Treasury yields is “thin at best” with valuations near multi-year tights, with the exception of China’s property issuers, according to Ek Pon Tay, BNP Paribas Asset Management’s senior portfolio manager in Singapore.

Tay recommends investors overweight investment-grade rated China property credits as these issuers are likely to survive in the event of a prolonged sector downturn and valuations offer ample spread cushion versus others.

精彩评论