Summary

- Walmart’s international segment is expected to lead the company’s revenue growth in the years ahead.

- The company’s leadership through Flipkart in the rapidly growing India market is expected to be a key competitive advantage as it scales up to compete against Amazon India.

- At the current price, Walmart is not expensive, and offers an attractive entry point for investors to partake in its international growth drivers.

Investment Thesis

Walmart (WMT) has very exciting growth prospects in its international markets, especially in India where the market is expected to overtake Canada as the second largest international market segment, behind the leader Mexico by 2025. In addition, the company’s astute investment in Flipkart has given it the key leadership in the e-commerce segment in India which is expected to grow rapidly in the years ahead.

Setting the Stage for International Expansion

Walmart has grand ambitions on the international stage. After the completion of the divestiture of Asda and Seiyu last quarter, the company has set its sights on driving its international growth in the faster growing markets. The company also discussed at length its international priorities and opportunities in two recent conferences (DBAccess, andBaird) on how to take its international business to the next level.

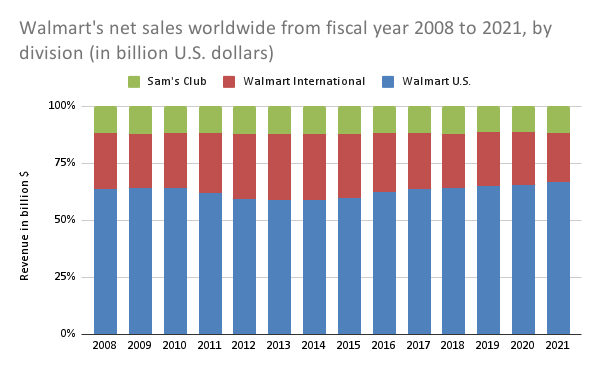

Walmart’s international sales accounted for about 21.9% of FY 21 revenue. As we could observe from above, WMT’s international business as a whole has been largely stagnant in recent years even though its U.S. operations saw relatively stable and consistent growth. The company’s exit from Seiyu [Japan] and Asda [UK] in order to reallocate capital to its higher growth regions, notably in India and China, is an important step towards aligning its growth priorities and rejuvenating its international business segment. In fact, Walmart had even received pretty nasty press on its operations in Japan, asNikkei Asiaremarked: “Walmart's foreign flops can be attributed largely to tone-deaf management, which failed to take into account local business customs, dietary habits and labor relations, among other glaring oversights.” Notwithstanding the sensational allegations made by the Nikkei, I think WMT has actually performed admirably in its international business as it’s aprofitable segmentfor the company that posted an operating margin of 4.4% in Q1’22, as well as 3% in FY 21, 2.8% in FY 20, and 4% in FY 19, respectively.

Ask Amazon How Hard It Is To Make Money Overseas

In order to understand how difficult it is to make money operating a retail business in international markets with a footprint as large as WMT, investors need to look no further than Amazon (AMZN), notwithstanding its focus on the e-commerce segment.

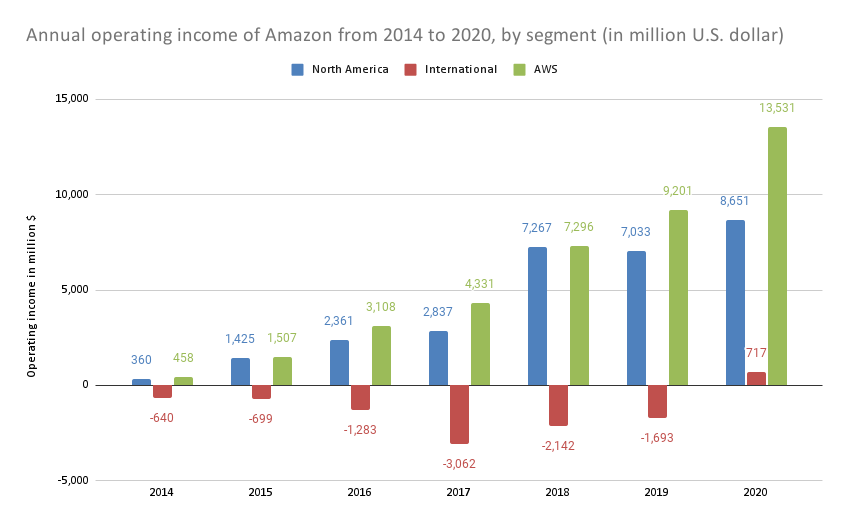

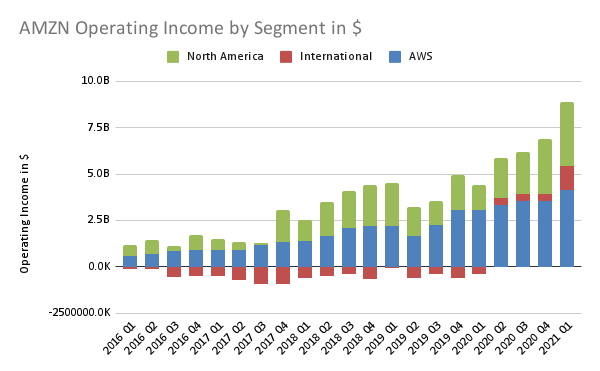

As we could observe from the 2 charts above, AMZN’s international segment only recently started to turn an operating profit in Q2’20 after experiencing losses over the last 6 years, even though the North America segment continued to do well. It’s a good reminder to investors that WMT knows how to manage its large international footprint well and it’s really very difficult to run an operation as geographically diverse and huge as Walmart’s and be profitable at the same time, giving the company an extremely wide moat.

India and China Expected to Lead Growth

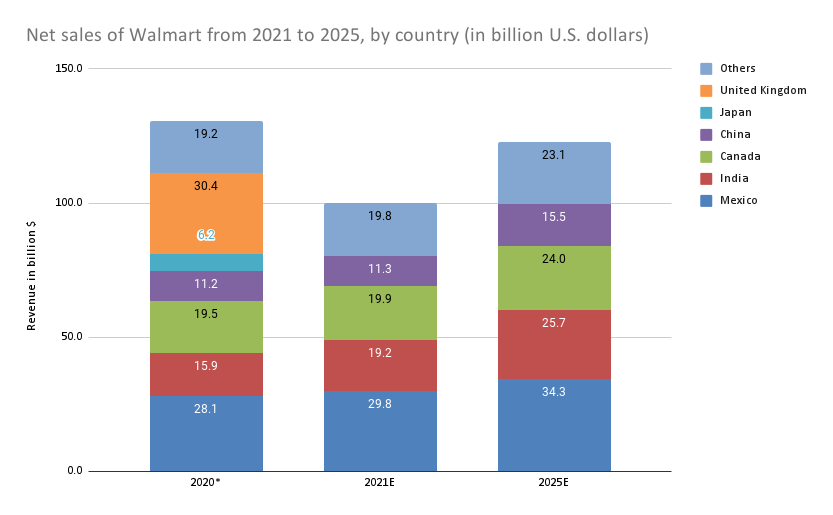

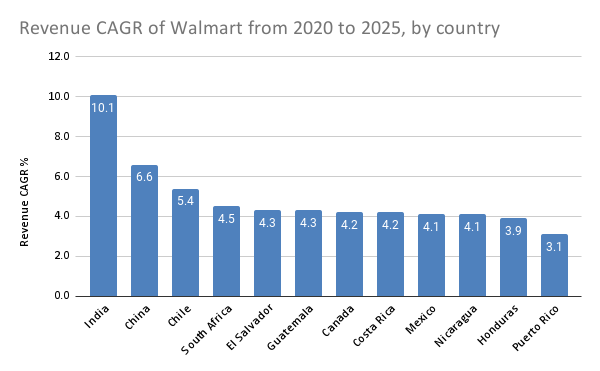

Although Mexico is still expected to remain as International’s most important revenue driver by 2025, India and China are expected to lead the growth, with India expected to be the company’s second largest international market by 2025.

India’s 5Y CAGR of 10.4% is expected to outperform the rest of its international peers, followed by China in second place with a 5Y CAGR of 6.6%. The rest of its international markets are also expected to grow relatively fast, including the leader Mexico (5Y CAGR: 4.1%).

If we consider the company’s overall expected revenue growth in the next few years, investors should now be able to appreciate the importance of WMT’s international markets to drive the company’s topline and therefore managing the growth of its international segment well would provide the company a highly significant lever to drive results over time.

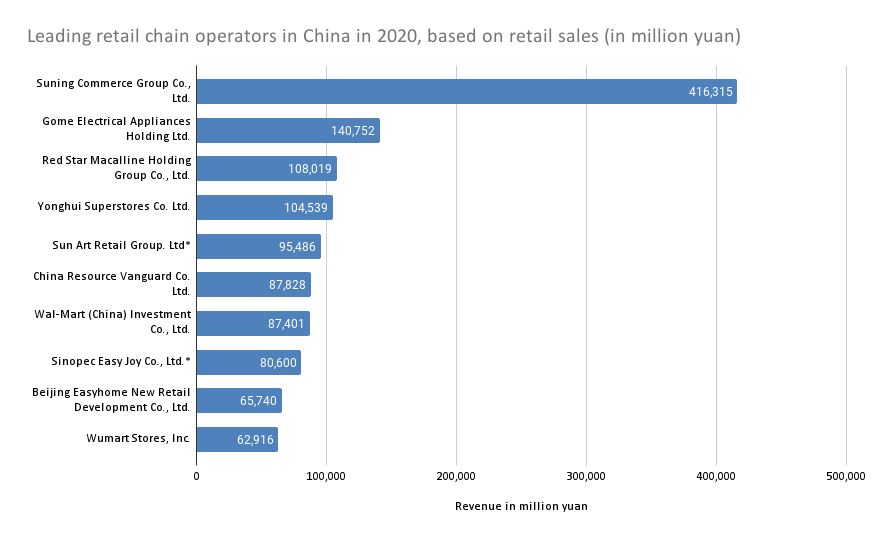

Although WMT’s leadership in the U.S. is undisputed, it may not be the same in China. The competitive landscape in China is strongly dominated by Suning Commerce Group, and WMT’s China operations was actually ranked 7th in this survey. Therefore, there is a tremendous amount of sales potential for WMT to make up in order to move up the ranks among China’s retail leaders.

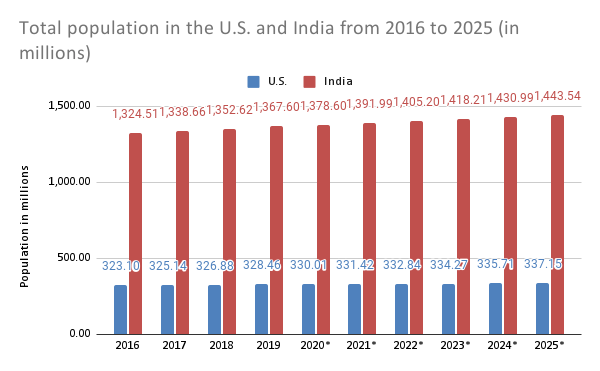

In the market where it is expected to lead the company's growth: India, this is where the excitement for WMT’s international business really begins. India’s population is expected to grow from 1.324B in 2016 to 1.443B by 2025, which would represent a CAGR of 0.96%, faster than the U.S. population CAGR of 0.47%, that is twice as fast, despite having a population size that’s already 4x larger to start with.

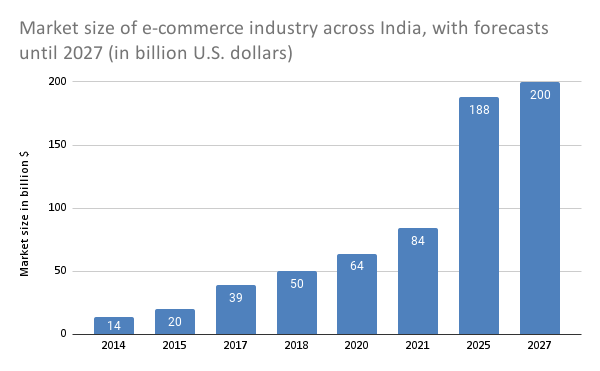

India’s e-commerce industry (WMT’s main channel in India) is expected to grow from just $14B in 2014 to $200B by 2027, which would represent a whopping CAGR of 22.7%, an incredible growth rate. More importantly, WMT is an e-commerce leader in India (though Flipkart), as Flipkart had a 31.9% market share as of Oct 20 according to Forrester Research, just ahead of its fierce rival, Amazon India, who had a 31.2% market share. Therefore, WMT looks very well positioned to compete strongly in India as the leader of a rapidly expanding e-commerce market.

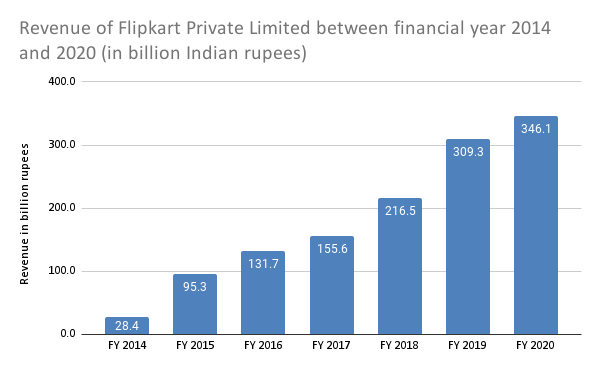

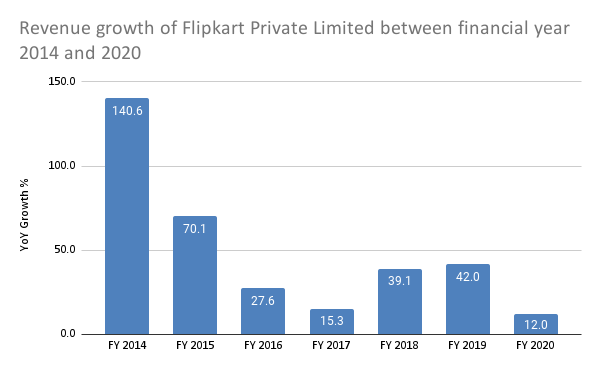

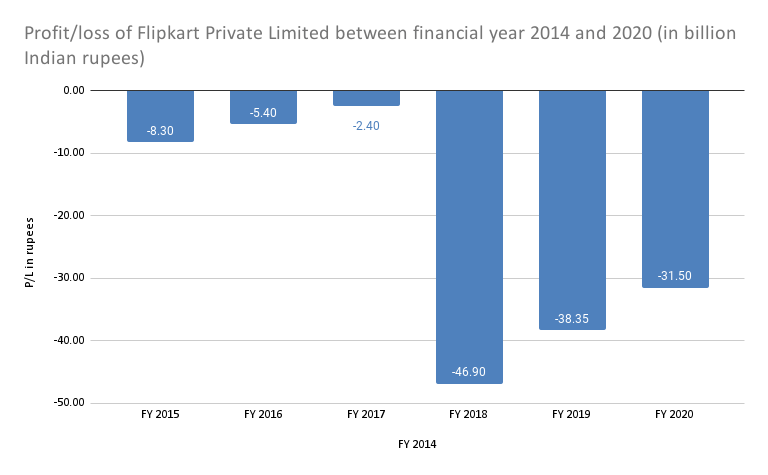

As we could observe from above, Flipkart’s FY 20 revenue of 346B rupees (equivalent to about $4.72B) has barely scratched the surface considering the market size of India’s e-commerce industry that was worth $64B in 2020. Even though the revenue growth of 12% YoY was an egregious deceleration from the previous year’s 42% YoY growth, the company has managed to reduce its net loss from 38.35B rupees to 31.5B rupees (see below), an improvement of 17% YoY. It would thus be important for investors to continue monitoring the health of its growth trend moving forward to evaluate whether there is a persistent deceleration that needs to be addressed by the company.

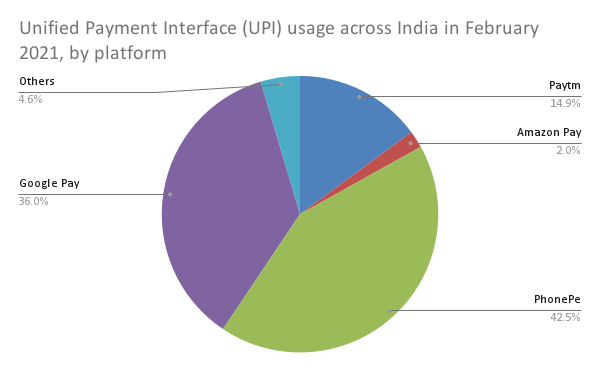

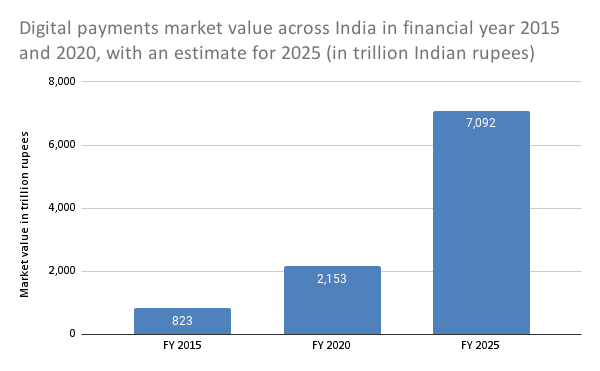

Meanwhile, the company’s UPI platform PhonePe is also the leader in UPI usage across India. UPI has become the dominant payments infrastructure across India with a 73% share of all digital transactions volume as of Feb 21. However, due to the 30% transactions restriction cap placed on all third-party payment apps that include PhonePe by the authority [NPCI] on the leaders, PhonePe and Google Pay would need to meet a 2-year deadline to bring down their transactions share to within the 30% cap. In addition, WhatsApp Pay is also expected to play an increasingly important role in this rapidly expanding market and compete against Google Pay and PhonePe. Notwithstanding the cap placed by NPCI, the digital payments market in India is expected to grow from 2,153 trillion rupees in 2020 to 7,092 trillion rupees by 2025 (see below), which would represent a CAGR of 26.9%, thus giving us a high level of confidence that there is ample room for all the major competitors to grow. Walmart definitely looks incredibly well-positioned in the India e-commerce market, where its e-commerce growth is still very much in its infancy.

Considering Walmart's Valuations

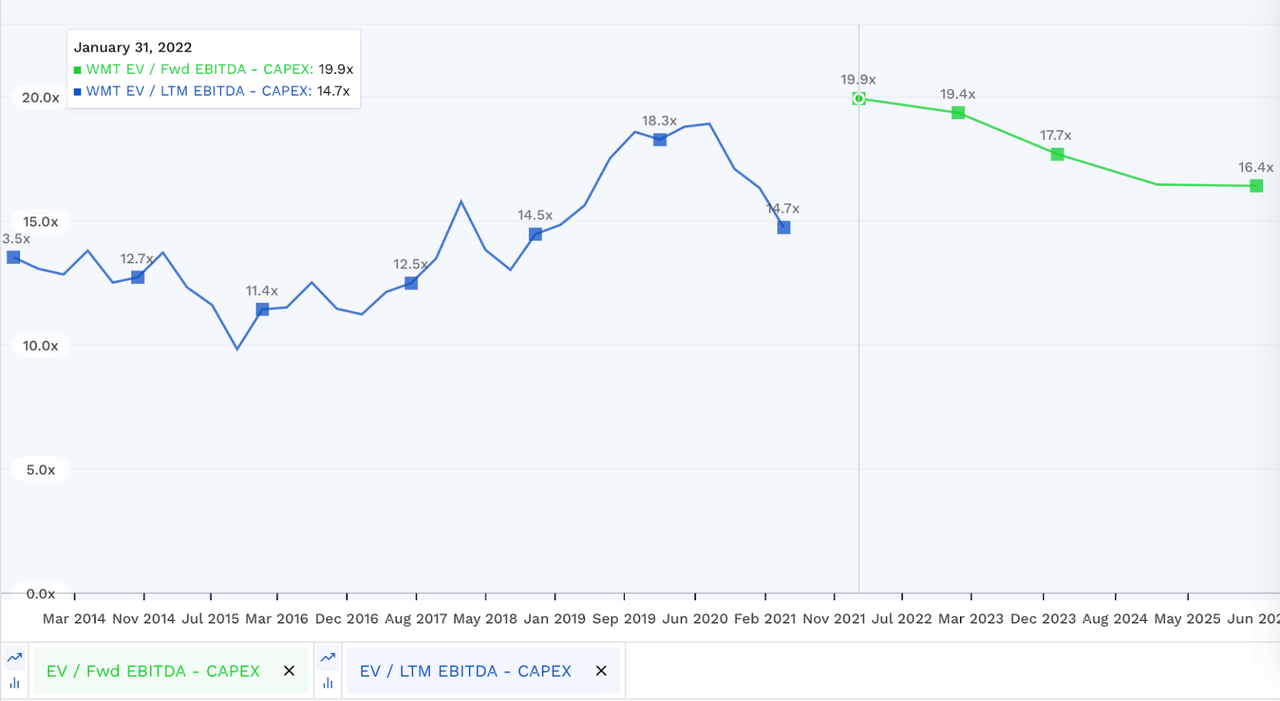

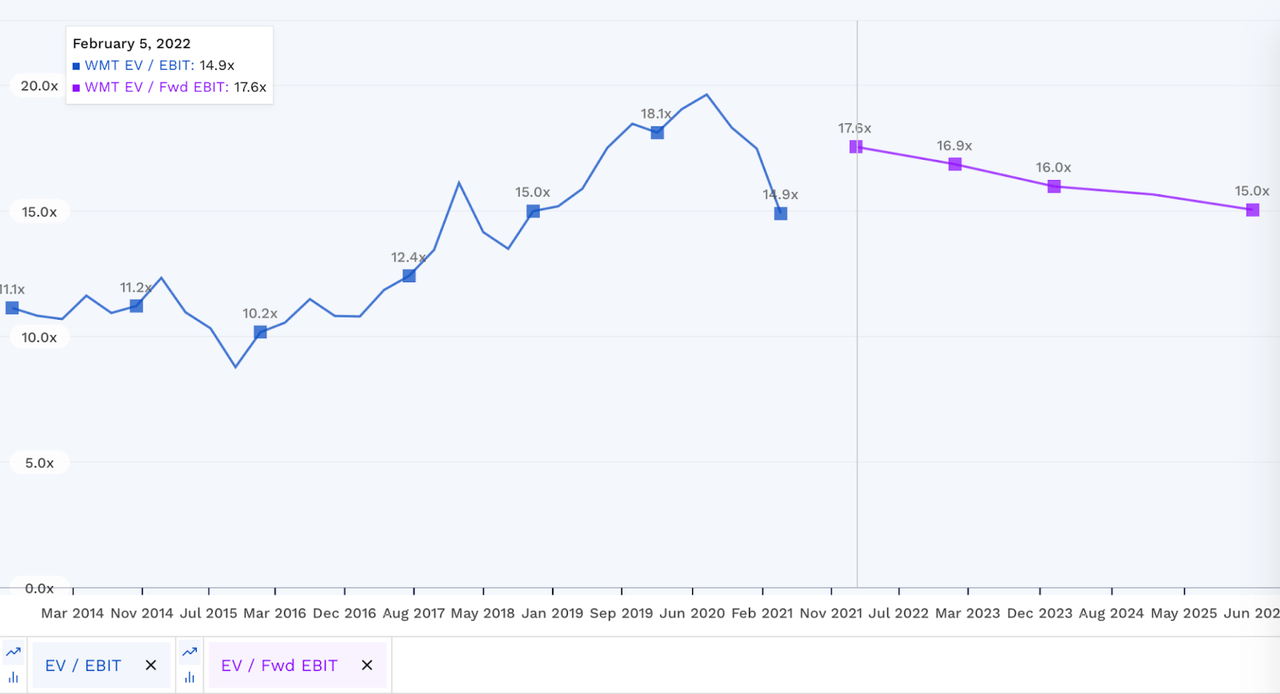

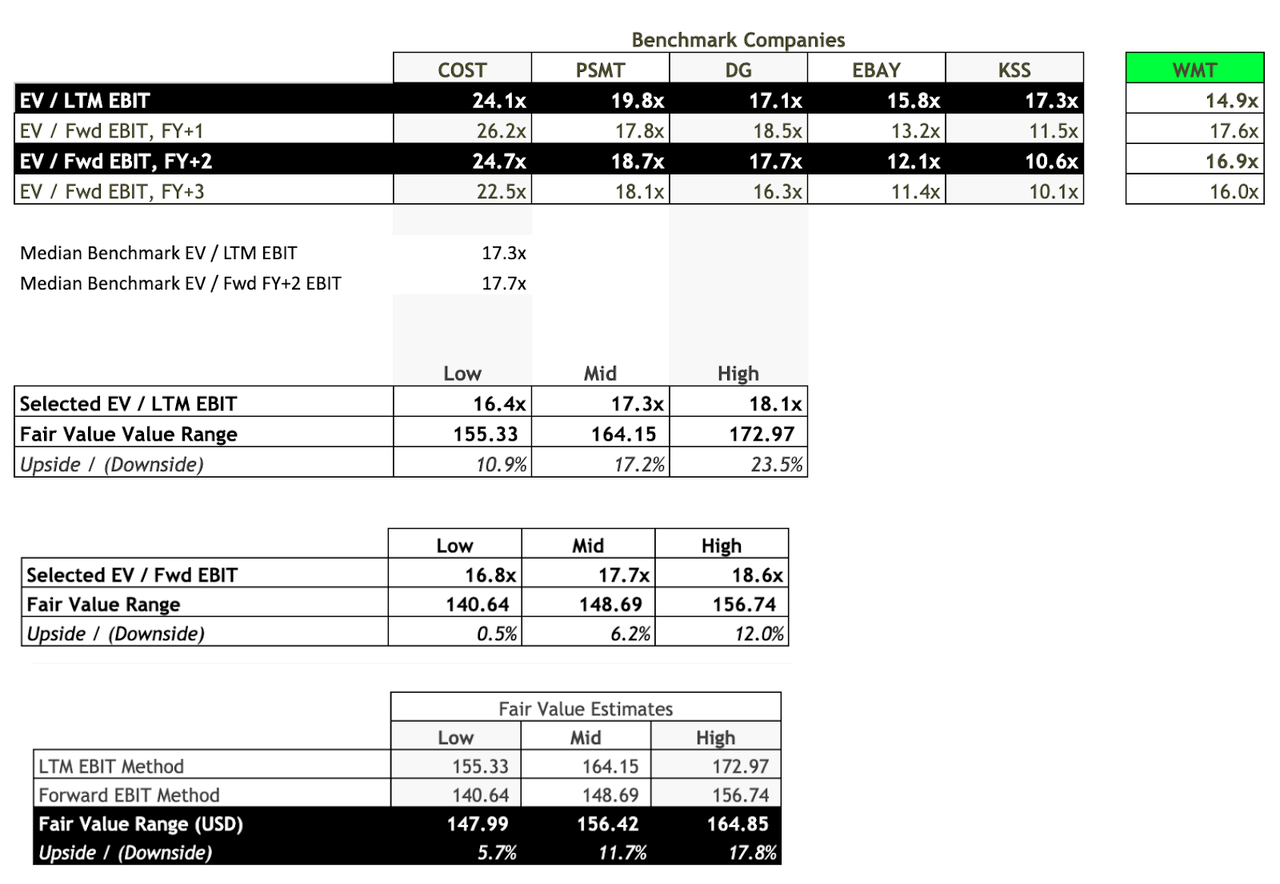

When we consider WMT’s FCF and EBIT relative valuations using both EV / EBITDA - CapEx (as a proxy for FCF) and EV / EBIT, WMT is currently valued near the higher end of both valuations range (EV / LTM EBITDA: 14.7x, EV / LTM EBIT: 14.9x) over the last 5 years. In fact, when we consider the company forward valuations, we could observe that the market seems to have priced in quite a bit of optimism into WMT’s future EBIT and FCF growth in which the company is expected to execute well moving forward.

Therefore, in order to have a basis on whether WMT’s forward valuations are also in line with what we expect from other companies, it would be useful to conduct an EV / EBIT comparison across a set of benchmark companies for us to have a reasonable basis to value WMT. We also observed that WMT’s EV / EBIT metrics have not been excessive when compared against this set of benchmark companies.

Using a blend of their EV / LTM EBIT metric and their EV / Fwd EBIT metric, we arrived at a fair value of $156.42 at the midpoint of the fair value range, representing a potential upside of 11.7% from 15 Jun’s closing price of $140.

Price Action and Technical Analysis

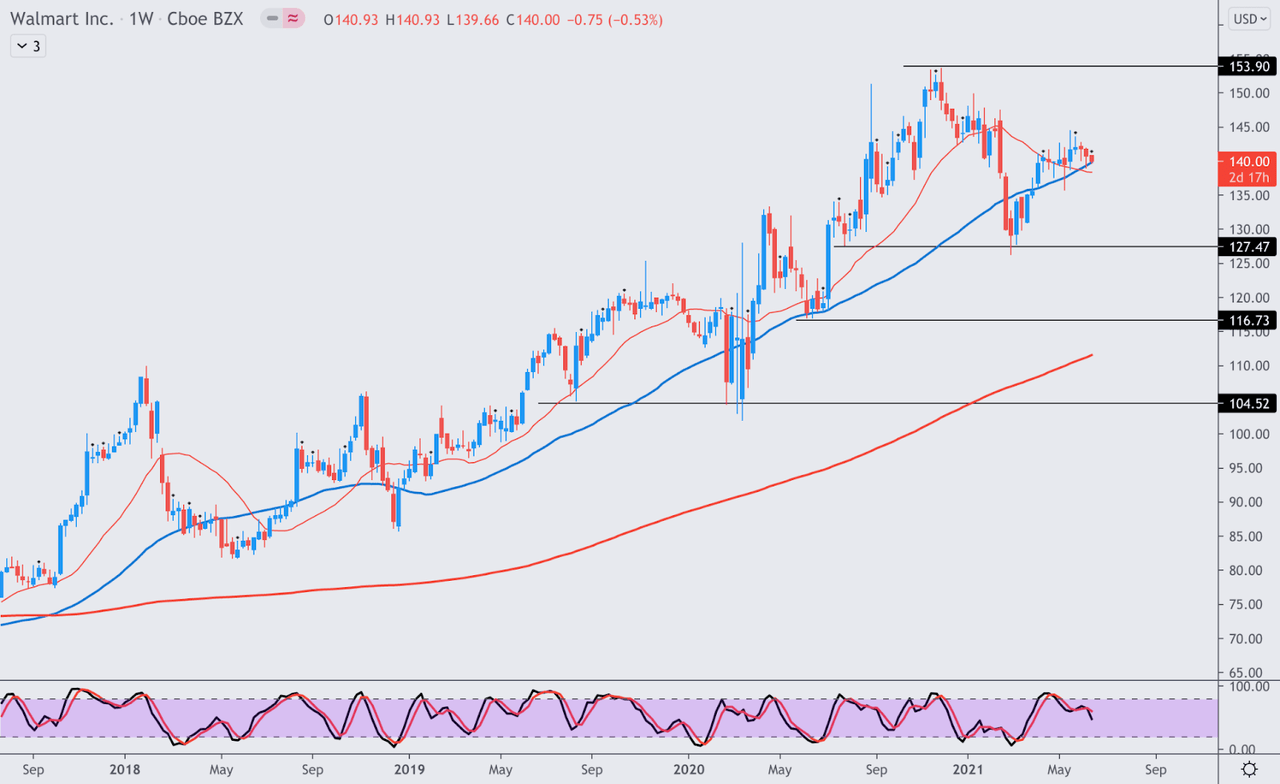

WMT is a strong stock that has always been well supported along its long-term uptrend over the last 3 years. The 50W moving average has always acted as its key dynamic support level, including during the 2018 bear market, and the 2020 COVID-19 bear market, demonstrating the confidence of the market in this customary market leader. The support level at $127 also looks like an extremely strong support level that attracted strong buying interest during the retracement in Feb - Mar 21 and investors should consider this as a "Buy more" entry point if the price retraces to that level in the future. Currently, the stock is right at the 50W MA support level again, and I think at the current price level of $140, it still represents an optimal technical buy entry. Investors should however avoid buying near $154 in the near term as it’s expected to be a near term resistance level.

Wrapping it all up

Walmart’s international strategies, especially in India are looking very exciting and is expected to be the company's main international growth driver. Although its international segment is still a relatively small segment of the company’s overall revenue, it’s expected to lead the group’s growth in the foreseeable future and the market definitely thinks so as well as WMT is expected to be valued at higher multiples than what was observed historically. Investors should therefore take advantage of WMT’s current price weakness to add to this fantastic stock in view of its attractive valuation right now.

精彩评论