Summary

- AMD is no longer an "underdog", and future growth projections do not necessarily justify its current valuation. In this note, we review AMD's Q3 results and guidance.

- Furthermore, I provide a pro-forma valuation of AMD (+Xilinx). The easy money has been made in AMD over the last six years, and future returns may look very different.

- AMD is a decent buy at $122, however, potential investors should buy through Xilinx at $185 (a discounted proxy for AMD) (after Dr. Lisa Su's reassurances about the merger).

Introduction

Advanced Micro Devices (AMD) is probably one of the greatest turnaround stories ever, and investors have made incredible returns in this counter over the last six years. Under the leadership of Dr. Lisa Su, AMD has showcased tremendous business execution, and the company delivered yet another blowout quarter on Tuesday.

As some of you may already know, I am an "Intel (INTC) bull"; however, I am not an "AMD bear" like some of the commenters in my recent articles have suggested. Today, I would like to explain my positioning in the semiconductor sector in some greater detail. First of all, we own Intel as a part of our dividend growth portfolio, which also consists of the likes of Broadcom (AVGO). Since AMD offers no dividend, it is unsuitable for BTM's DGI portfolio. On the other hand, AMD's risk/reward is keeping the stock out of our Goldilocks Zone (high growth) portfolio. Within this portfolio, we own Nvidia (NVDA) from a very low cost-basis; however, we are not adding at current valuations.

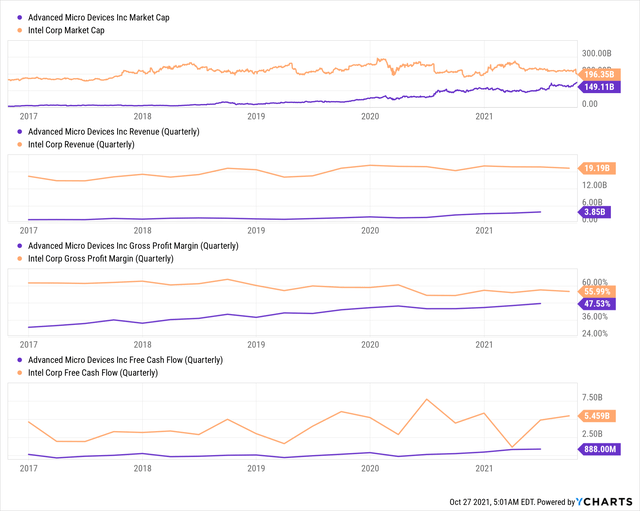

Today, AMD's market cap stands at ~$150B, and it is quickly closing the gap on Intel, which is now valued at just ~$195B. Now, Intel does ~5x AMD's revenue, commands higher gross margins, and produces ~6x AMD's free cash flow. Considering these numbers, AMD seems expensive; however, growth is on AMD's side due to superior products, product roadmap, and business execution.

In this note, we will briefly analyze AMD's Q3 report and formulate its valuation to see if this stock is a good long-term investment. Furthermore, we will explore a merger arbitrage play available in the AMD-Xilinx (XLNX) deal. So, let's get started.

Reviewing AMD's Quarter And Forward Guidance

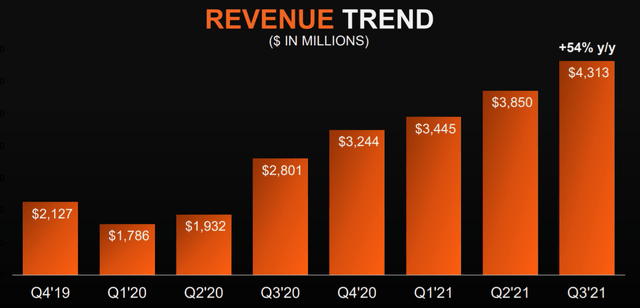

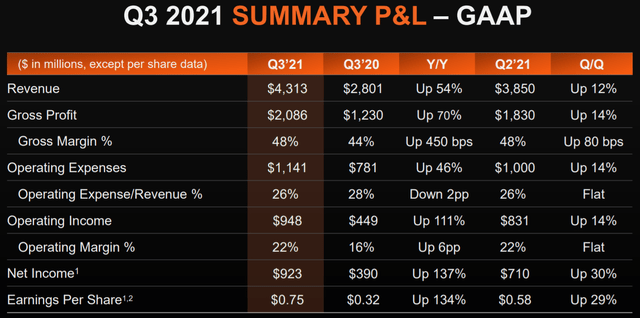

In Q3, AMD's revenue blew past analyst estimates to come in at $4.3B (up 54% y/y), and looking at the quarterly sales trend, it is fair to say that AMD's business is gaining momentum. Although the growth rates are decelerating due to tough comps from last year's PC boom, AMD's data center business is on fire and set to deliver greater numbers in 2022 and beyond.

Here are the highlights from each of AMD's business segments:

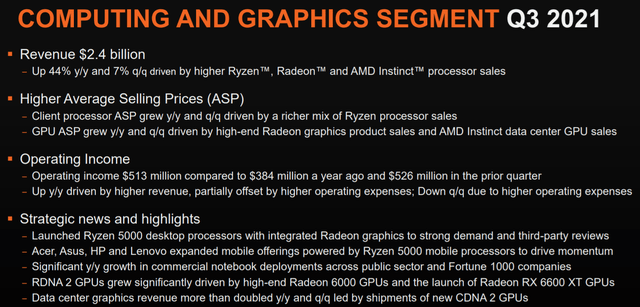

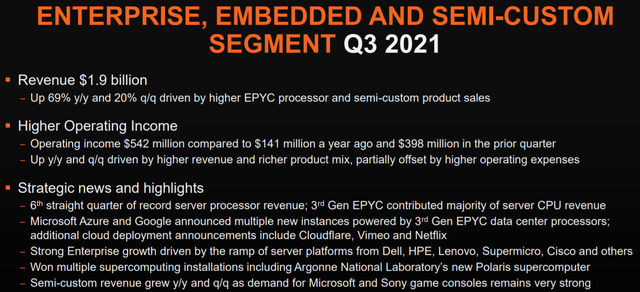

With its Ryzen, Radeon, and EPYC processors, AMD is winning market share across the CPU, GPU, and server (data center) markets. Over the last few years, AMD's products have been far superior to those of Intel's, and with a strong product roadmap, AMD looks good value for a greater chunk of the expanding semiconductor industry.

As the industry continues to grapple with supply shortages, AMD has focused its resources on higher-value chips. Naturally, AMD's gross margins have expanded significantly over the last few quarters. In Q3, AMD's gross margins improved by ~450 basis-points y/y to reach 48%. With a sharp rise in margins, AMD is delivering massive operating leverage, as evidenced by the ~111% y/y jump in operating income. As you can see below, AMD's operating margins have risen from 16% (Q3 2020) to 22% (Q3 2021). Overall, AMD's business is firing on all cylinders with rapid sales growth, massive margin expansion, and a big jump in profitability.

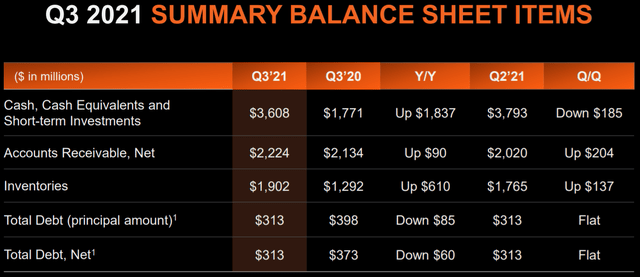

As it turns into a cash printing machine, AMD's balance sheet is turning into a fortress. At the end of Q3, AMD had cash balances of ~$3.6B with total debt of just ~0.3B. After teetering near bankruptcy at the start of the 2010s, it is fair to say that AMD has come leaps and bounds. Right now, AMD looks very well-positioned (from a financial and technological perspective) to win a more significant market share in a secular growth industry. With ample cash on its balance sheet, AMD used nearly all of its free cash flow on repurchasing shares as the company bought ~$750M worth of its own stock in Q3. In the future, we can expect these buybacks to become a routine affair.

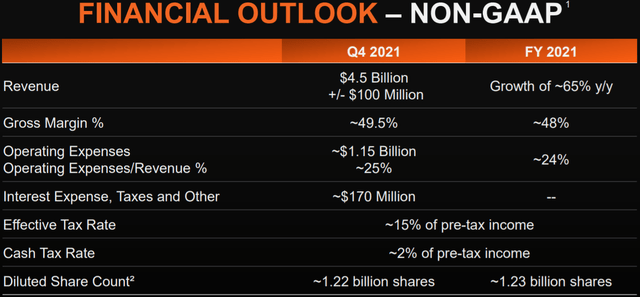

For Q4, AMD is guiding for $4.4-4.6B in revenue on higher gross and operating margins of 49.5% and 25%, respectively. Hence, AMD's business momentum is likely to continue in the next quarter.

When answering questions from an analyst on the earnings call, Dr. Lisa Su, AMD's CEO, said that the semiconductor shortages might end in 2022, and while competitive pressures are rising, she is confident in AMD's product roadmap. Furthermore, she affirmed that the demand environment is set to remain strong throughout 2022, with data center demand coming in hot, while the PC market is expected to remain flattish.

Although AMD's management stopped short of guiding for 2022, the company is likely to deliver rapid growth next year too (my estimate is ~25% y/y (tough comps)). With a strong leadership team at the helm, AMD is rapidly turning into a dominant semiconductor company. I am not convinced about AMD's ability to maintain its margins in 2022 due to growing expectations of a price war (and more competitive products) from Intel. Regardless, I see AMD as a secular growth stock with massive potential. With all of this information in mind, let us now attempt to find AMD's fair value and expected returns to see if it is a good investment.

AMD Stock's Fair Value And Expected Returns

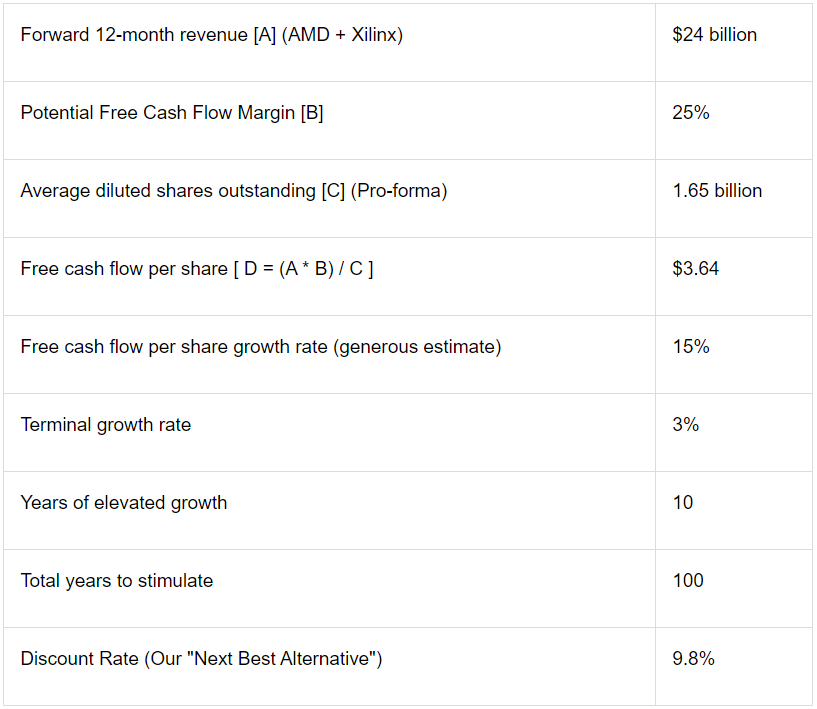

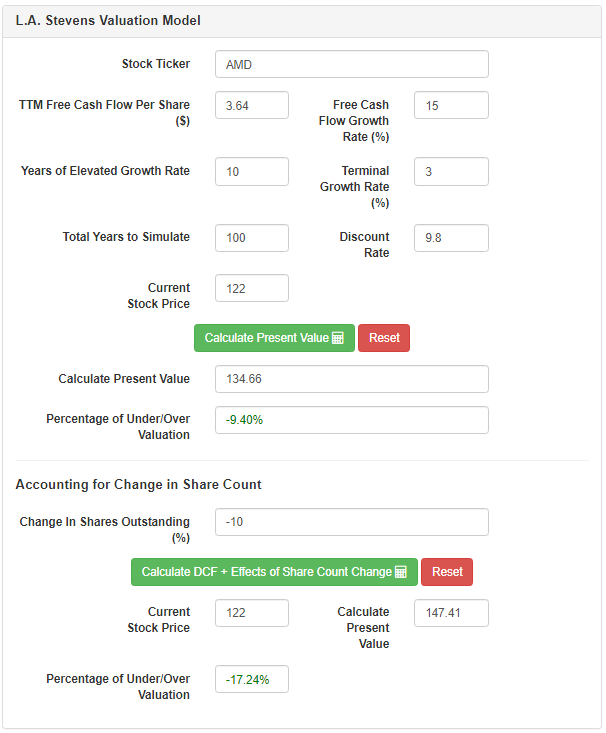

To determine AMD's fair value (including Xilinx), we will employ our proprietary valuation model. Here's what it entails:

In step 1, we use a traditional DCF model with free cash flow discounted by our (shareholders) cost of capital.

In step 2, the model accounts for the effects of the change in shares outstanding (buybacks/dilutions).

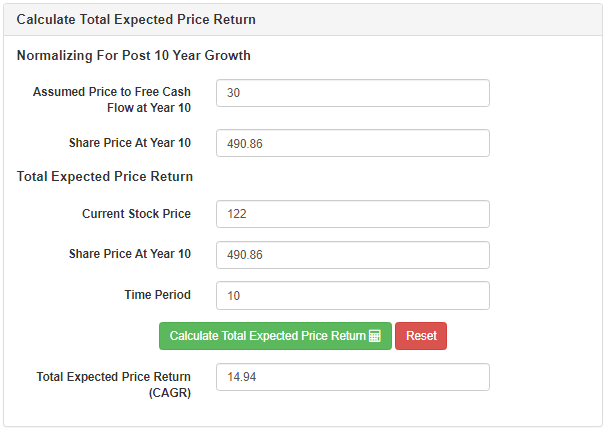

In step 3, we normalize valuation for future growth prospects at the end of the ten years. Then, we arrive at a CAGR using today's share price and the projected share price at the end of 10 years. If this beats the market by enough of a margin, we invest. If not, we wait for a better entry point.

- In step 4, the model accounts for dividends.

Assumptions:

Here are the results:

As you can see, AMD is worth ~$147.5 per share, i.e., it is undervalued by ~17.24%. Now, let us analyze AMD's expected returns:

Since AMD's expected return is equivalent to ~15% (our investment hurdle rate), it is only a modest buy at the current price. However, buying AMD via Xilinx could improve future returns, making it a worthy option. We will discuss this merger arbitrage play in just a moment, but before we do so, let's discuss something critical to our valuation.

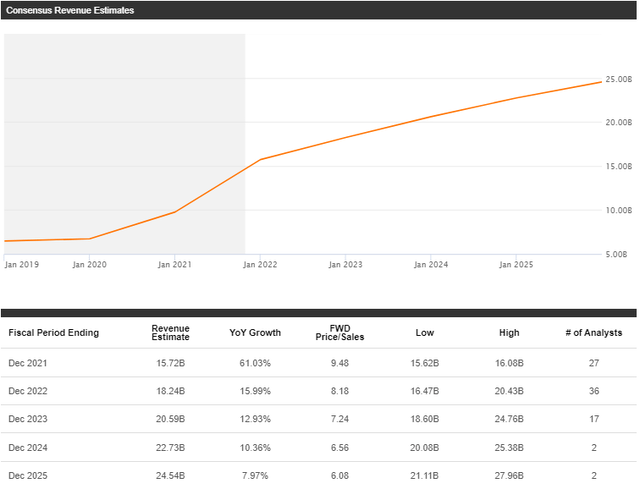

The growth assumption of 15% CAGR from a base of $24B implies a 2031 revenue figure of $100B. If AMD fails to win a monopolistic market share (comparable to Intel's past dominance) over the next decade, these revenue growth targets may not be achieved. We must be cognizant of the fact that AMD is up against the likes of Nvidia, Apple (AAPL), Intel, ARM-based chip makers, and all other big-tech companies making their own chips in-house. Now, let's take a look at consensus analyst estimates for AMD's revenue growth rates:

As you can see, AMD's growth rate is expected to decelerate significantly over the coming years. Now, I understand that Wall Street analysts are wrong most of the time, and I can envision a world where AMD does $100B in revenue every year. However, I don't think we have an ample margin of safety while investing in AMD due to aggressive growth projections priced into its stock.

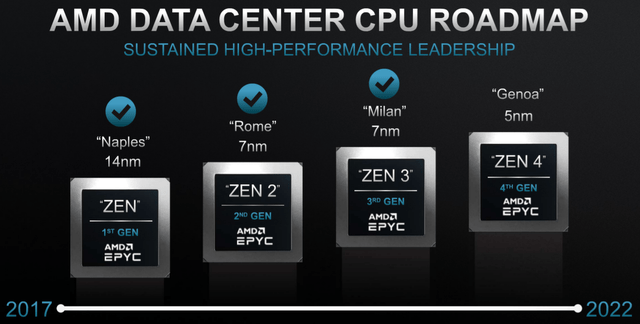

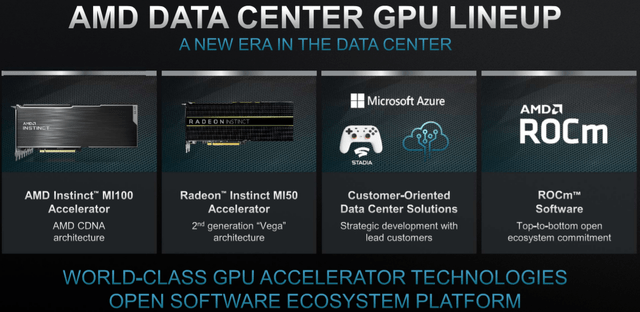

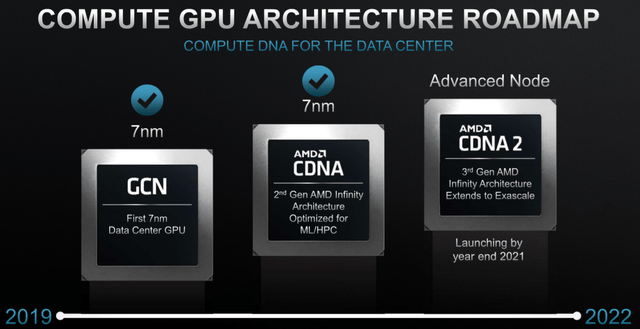

With the acquisition of Xilinx, AMD is expanding its total addressable market from ~80B to ~$110B. Currently, AMD's product portfolio is not as broad as Intel and Nvidia (AMD project's data center TAM for its products at just $45B, Intel and Nvidia have data center TAM's of ~$230B); however, this should be viewed as an opportunity for growth. With that being said, AMD's 3rd Gen EPYC processors (the fastest x86 server CPUs) are winning market share in the data center (still heavily dominated by Intel), and the company has a strong product roadmap for further enhancing its presence in high-performance computing, AI, and data center markets.

With the impending 2022 launches of Zen4 powered EPYC CPU processors and CDNA2-powered GPUs, AMD is set to maintain its product leadership over Intel, and capture more market share in the data center in 2022 and beyond. As we know, Intel is struggling with its manufacturing process, and a move to outsource advanced node manufacturing (to TSMC(NYSE:TSM)for Ponte Vecchio and a few other upcoming Intel products) is not enough to stop AMD's higher-performing, less power consuming products from winning market share (at least in the medium term). Hence, AMD can deliver another spectacular year of sales growth in 2022 (far better than what analyst estimates suggest).

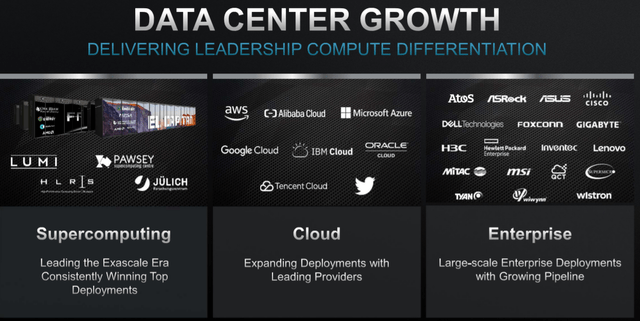

After years of solid execution, AMD has regained customer trust in the data center markets as evidenced by its recent partnerships with some of the largest cloud providers in the world. Under the exemplary leadership of Dr. Lisa Su, AMD can become a true heavyweight in the burgeoning semiconductor industry over the next decade and beyond.

AMD-Xilinx: Merger Arbitrage Play

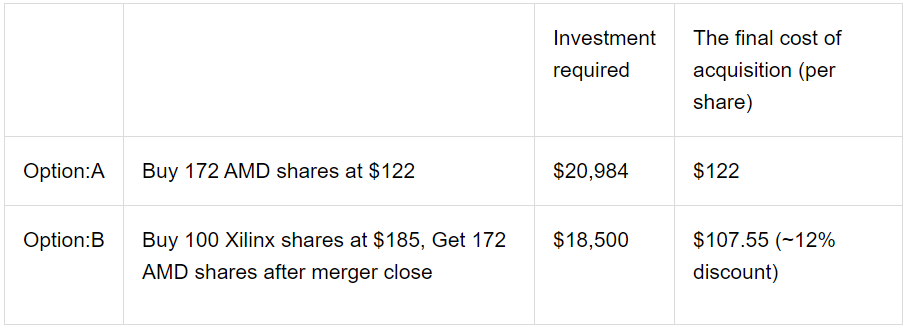

During the earnings call, AMD's CEO, Dr. Lisa Su, reiterated the expectation of deal closure on the Xilinx acquisition by the end of this year. As you may know, AMD agreed to buy Xilinx in an all-stock deal, and each Xilinx stock will convert to 1.7234 shares of AMD. Due to market inefficiencies (or expectation of deal failure), investors can buy AMD via Xilinx's stock to avail of a massive discount. Here's how:

Hence, investors looking to buy AMD can get a 12% discount by purchasing it via Xilinx. Furthermore, I think this is an excellent opportunity to establish a merger arbitrage trade - "Buy '1x' Xilinx, Short '1.7234x' AMD". With this trade, investors can pocket a 12% return in just two months (if the transaction closes as per the timeline provided by AMD's CEO).

Concluding Thoughts

AMD is performing exceptionally, and business will remain strong in the near term due to a strong demand persisting in a semiconductor supply crunch. The stock is still undervalued; however, AMD's risk/reward makes it only a modest buy. If you still want to buy AMD, I recommend buying it through Xilinx to avail of a ~12% discount on the purchase.

Key Takeaway: I rate AMD a modest buy at $122 and Xilinx a buy at $185.

精彩评论