Summary

- GameStop continues to be a struggling video gaming retailer with limited upside and no ability to create additional shareholder value anytime soon.

- With short interest of less than 15%, investors shouldn’t expect to see another squeeze happening in the following months.

- We stick to our opinion that it’s better to avoid GameStop, especially since its stock is extremely overvalued at the current price.

It’s safe to say that GameStop’s (GME) squeeze has run its course and with a short interest of less than 15%, investors shouldn’t expect to see another squeeze happening anytime soon. In addition, as GameStop continues to struggle to improve its performance, while the gaming industry experiences double-digit growth, it’s unlikely that the retailer will be able to create additional shareholder value in the foreseeable future. Considering this, we stick to our opinion that it’s better to avoid GameStop, especially since it’s extremely overvalued at the current levels.

Nothing To Look At

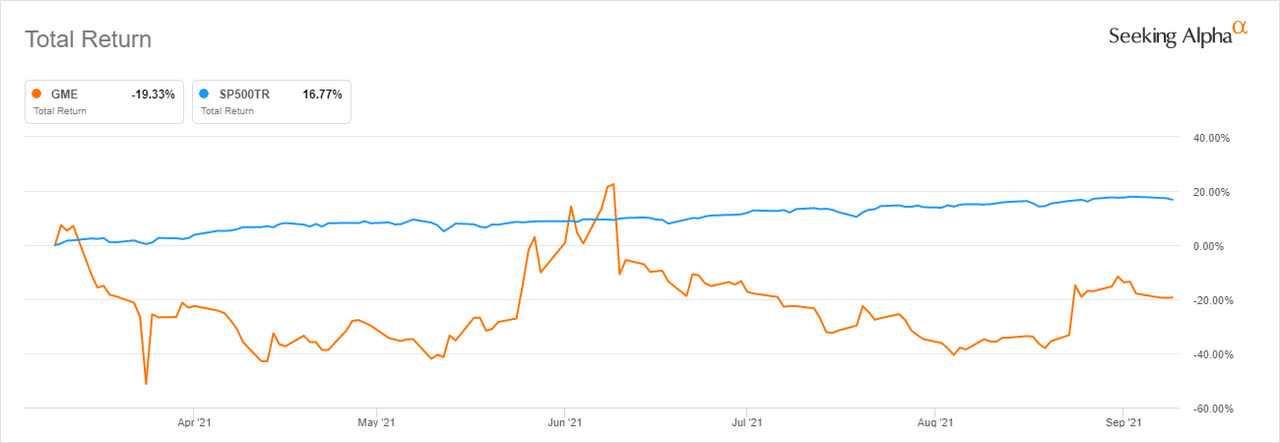

GameStop continues to be a struggling video gaming retailer at this stage. Its business failed to significantly improve during the greatest growth of the video gaming industry in a decade, and it’s unlikely going to improve anytime soon. While retail traders managed to squeeze short-sellers earlier this year, GameStop’s stock failed to gain any traction in recent months. We were right when we said that its momentum is fading away, as the stock is down nearly 7% from when our last article on the company was published in late June, while the S&P 500 is up over 5% for the same period. Going forward, we continue to believe that GameStop’s shares will depreciate even more in the foreseeable future.

Just last week GameStop released its Q2 earnings results. During the period, the company managed to generate only $1.18 billion in revenues, up 25.3% Y/Y, barely beating the estimates by $60 million. The problem is that a 25.3% Y/Y growth is terrible for a company such as GameStop since lots of its stores were shut down during the same period last year due to the pandemic and a minimal amount of revenue was generated. On top of that, the company’s non-GAAP EPS was -$0.76, below the estimates by $0.09, while its net loss stood at $61.6 million.

The biggest downside of GameStop is that it doesn’t have any unique positioning in the video gaming industry. The company acts as a middleman with no clear advantages to publishers or consumers, while at the same time its retail-focused business model is unable to adapt to the new reality where games can be easily and legally downloaded online. Another problem of GameStop is that at the end of Q2 most of its revenues come from the sale of hardware such as consoles, which were released last year. Once the demand for new devices decreases over time, the sales of the hardware side of the business will decline as well.

With Ryan Cohen as the new chairman of the board, the goal of GameStop right now is to pivot to the eCommerce business. However, we find it hard to believe that the company has a decent shot of becoming a video gaming behemoth in the eCommerce field. The problem is that GameStop doesn’t have any pricing power in the software business, as publishers such as Microsoft (MSFT), Sony (SNE), Ubisoft (OTCPK:UBSFY), Electronic Arts (EA), and others are already ahead of GameStop in online presence. Most of them have their own first-party subscription services that make it more attractive for gamers to use the services directly and play games at a significant discount rather than buy games from GameStop. On top of that, cloud gaming becomes more of a reality with each passing year thanks to the introduction of services such as PlayStation Now and Xbox Cloud Gaming, which let consumers play games without owning them in the first place. As the industry continues to digitize more and more every year, GameStop will continue to lose market share, as its retail stores will continue to drain the cash, while eCommerce efforts are unlikely going to generate meaningful returns anytime soon.

Another downside of GameStop is that the management has been quiet about how GameStop will transform itself, leaving investors in the dark. No questions from analysts were taken during the last three conference calls and no guidance was issued as well. We consider this to be a major red flag and believe this to be one of the main reasons why GameStop is an unattractive investment.

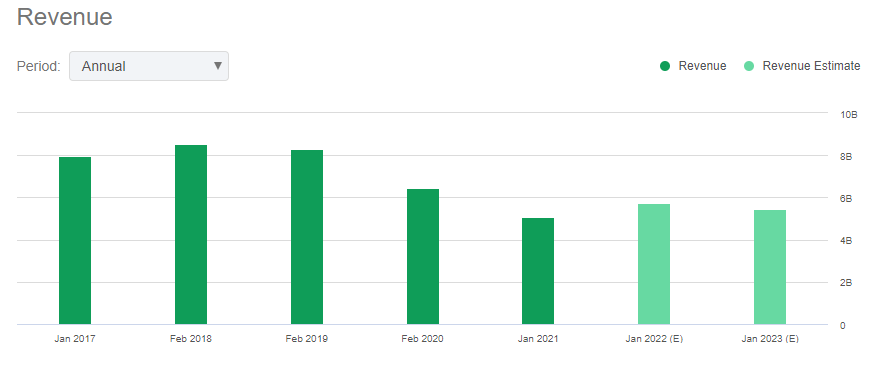

The only positive thing about the company is that it doesn’t have an overleveraged balance sheet, as its liquidity at the end of Q2 stood at $1.72 billion, while long-term debt was only $47.5 million. However, other than that, we don’t see any other upside of GameStop and believe that its momentum will continue to fade. It’s already safe to say that the squeeze has run its course, as the stock has a short interest of less than 15%, and there are no catalysts for growth at the current levels. On top of that, the company’s annual revenue is unlikely to return to pre-pandemic levels anytime soon. Currently, the business is expected to continue to generate less than $6 billion in annual revenues this year, as its retail-focused business model is slowly dying, while the video gaming industry continues to grow at a double-digit rate every year.

In addition, GameStop’s business has been unprofitable in the last three years when the gaming industry was growing, and it’s likely going to remain unprofitable this year, as nearly all of the company’s profitability metrics are below the sector median, while most of its margins are negative.

Considering all of this, we find it hard to justify buying GameStop’s stock at a ~$15 billion market cap, as we see no catalysts that could’ve helped the business to improve its performance in the future. Also, most of the street analysts remain bearish on the stock, as the current consensus price target for GameStop’s shares is $37.50 per share, which represents more than 75% downside from the current market price. For that reason, we stick to our opinion that the momentum is fading away and it’s better to avoid GameStop at this stage.

精彩评论