Summary

- Despite what some have characterized as a disappointing quarter, Amazon remains one of the highest quality stocks in the market with a long runway still ahead.

- After previous pandemic-fueled results and this year's reopening excitement, the results were bound to retreat at the margin leaving the new CEO with some upcoming heavy lifting.

- Despair not! This is an opportunity for long-term investors to accumulate shares incrementally as the stock retreats.

Investment Thesis:

Amazon (AMZN) (also, "the Company" hereafter) reported results that disappointed some who may not have anticipated a retreat from the pandemic-fueled growth rates seen previously. As an investor who is still accumulating chips, I see this as more opportunity than setback and see the stock's retreat as missing the forest for the trees - a market hallmark. The metrics are stronger than many reports indicate and this pullback also acts to keep the stock from going euphoric and decoupling from underlying metrics. Accumulating incrementally during the likely brief downtrend may be the best course of action.

By The Numbers

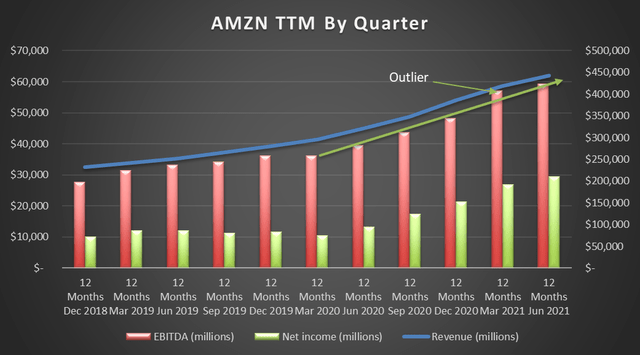

Q2 2021 top-line revenue came in at $113B compared to Q1 2021 $108.5B, a 4% quarterly increase. Revenue was up 27% compared to Q2 2020. EBITDA for Q2 2021 was up a whopping 36% over the same period in 2020, however was down 14% from Q1 2021. However, due to the cyclical nature of retail, I prefer to analyze the data using the trailing twelve months (TTMs) by quarter.

Over the TTMs Amazon generated $443B in revenues and an impressive $59B in EBITDA. While growth certainly slowed from Q1 2021 savvy investors understand that data does not exist in a vacuum and must be put in proper context. Covid created immense growth that was known to be inorganic as many who would typically frequent brick-and-mortar stores shopped from home. Many of these folks will continue to frequent Amazon, while some will return to previous habits. Still, others likely returned to retail upon lifting of restrictions just to leave the house and feel normal and will utilize online retail more once the novelty wears off. The same logic applies to Amazon's digital offerings. For these reasons, Q2 2021 growth was destined to slow from the breakneck pace of the prior periods, however, the Company still managed to grow revenue nearly 6% over the prior TTMs and, as stated above, 4% over Q1 2021 - no small feat. The Delta variant and likely return to restrictions and caution from shoppers will again change the game for the final 2 months of Q3 and likely for Q4 2021. Frankly, and amazingly, I believe we are about to be caught flat-footed against this variant which will be bad for many, but possibly positive for Amazon's sales in Q3 and Q4 2021.

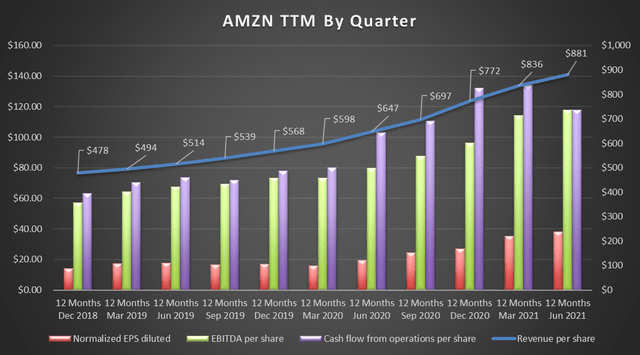

The data on a per share basis tells much the same story as above.

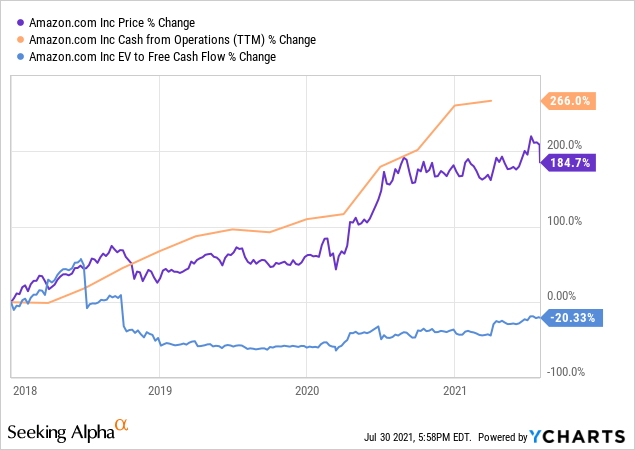

Revenue growth per share is solid while EBITDA and cash from operations per share have stalled. Many have expressed concern with the decrease in cash flow from operations, however, I prefer to use levered free cash flow (LFCF) as I believe it is a better metric to determine true cash available to shareholders. Cash flow from operations (CFO) is impacted by temporary changes in accounts receivable and accounts payable (changes in working capital), and does not account for capital expenditures (CAPEX) or debt payments. LFCF is a better measure of the cash available once all obligations have been met.

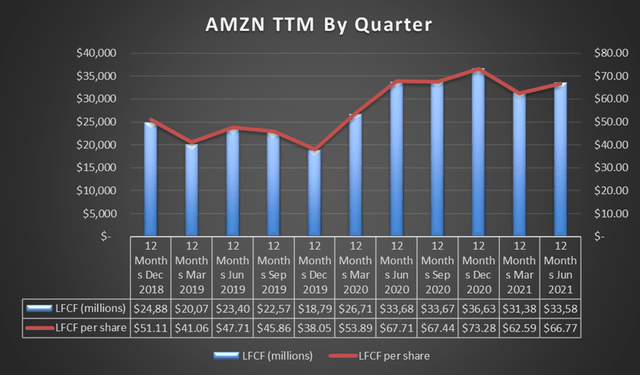

The Company's LFCF is down from the Covid holiday boom, but still rose significantly from 2019 results and was still up on a quarterly basis.

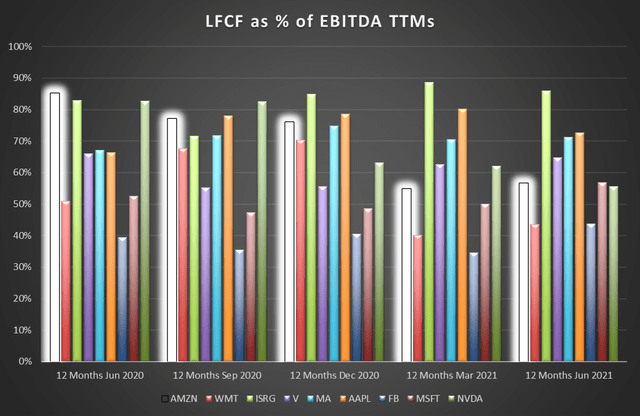

Further, when measuring results, the quality of the earnings can be brought to light by measuring LFCF as a percentage of either net income or EBITDA. I compared Amazon's LFCF/EBITDA to some of the most successful companies, including a lesser-known name, Intuitive Surgical, Inc (ISRG) that, if you are unfamiliar with this company, I encourage you to explore this juggernauthereandhere.

As shown, Amazon has come back to earth a bit from the pandemic heights, however still produces better LFCF/EBITDA consistently more than retail competitor Walmart (WMT), and also Microsoft (MSFT) and NVIDIA (NVDA), while lagging Visa (V), Mastercard (MA), and Apple (AAPL) which generally spend much less on CAPEX. It is also clear why I am so bullish on Intuitive Surgical. For Amazon, it is apparent that the pandemic boost lost steam in Q2 2021, however, the results were still quite positive.

Valuation & Opportunity

While Amazon's quarter was impressive by most standards, it disappointed many who decided to take profits last week.

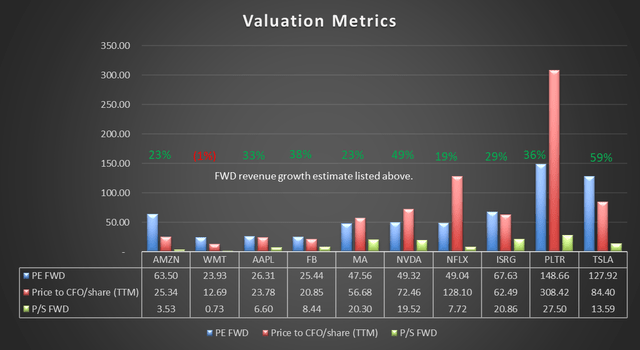

For long-term investors, this is not necessarily a negative. If one is still adding money to investment accounts or looking to take profits in other holdings and reallocate funds, the drawback represents an opportunity. I prefer to accumulate incrementally during a downturn rather than trying to call a bottom. How long it continues and how low the stock falls is unknown, however, I believe the downtrend will be short-lived. Another reason not to be rattled by the sell-off last week is that the stock has avoided the dreaded euphoria that likely would have caused the valuation to decouple from results leaving long-term investors in a poor place to add shares. The pullback will allow the fundamentals to catch up to the valuation a bit. Below I have compared Amazon's valuation to some of the outstanding companies above and also added digital rival Netflix (NFLX), Seeking Alpha fan-favorite Palantir (PLTR), and the ever-polarizing Tesla (TSLA) for additional context.

Note that forward revenue growth estimates (YOY) are listed for consideration.

I have also seen concern expressed for the enterprise value to cash from operations (EV/CFO), however, this does not convince me that there is long-term trouble in this area, especially in light of the increase in LFCF.

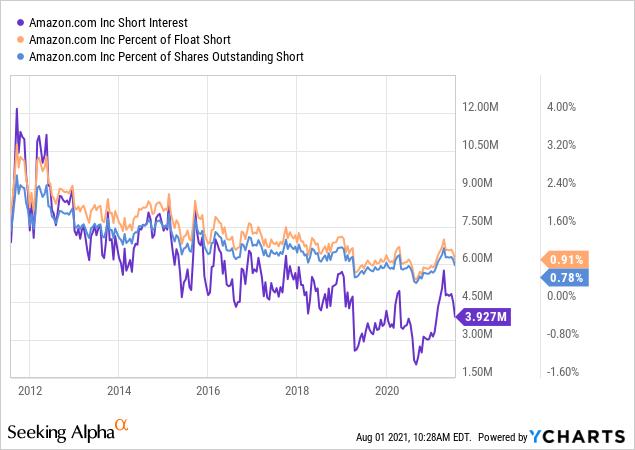

Finally, the short interest can be a useful tool to determine when the stock has become overvalued. Amazon is again running less than 1% of the float short, which is an indication that the downswing may be short and shallow.

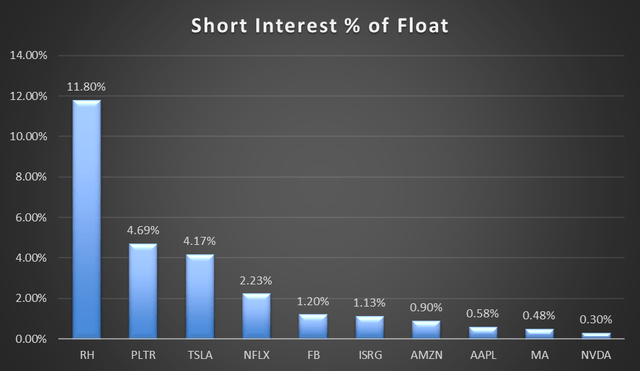

The short interest is near historic lows, pandemic notwithstanding, and after a brief rise as shares touched $3,700 is again falling. The short interest at this level tells me that while some grumble about the Company's value, few are willing to put their money where their mouth is at this point. I have included the short interest of other stocks discussed below for comparison.

CEO Transition & Obstacles Ahead

Jeff Bezos is an extremely savvy executive and likely could see that, post-pandemic, the heavy lifting would begin in earnest. He chose to enjoy his billions and take a rocket into space while on top. I certainly don't blame him. Meanwhile, new CEO Andy Jassy assumes command after 24 years with the Company. While some may see Bezos stepping down as a negative, it can also allow an opportunity for the new CEO with a fresh voice and something to prove. Apple has thrived after the transition from Steve Jobs to Tim Cook and hopefully, this will also be the case at Amazon. His job won't be easy as congress seeks increased regulations on large tech and the labor force presents challenges on multiple fronts. Jassy is largely credited for growing the highly profitable AWS arm of the Company which shows from where management believes much of the future growth is likely to come.

Risks and Uncertainties

As mentioned above, congressional leaders from both parties have expressed concerns with the power of large tech companies and pledged to reign them in. This could negatively affect results and there is the possibility that some large tech companies would be forced to spin-off segments. Spin-offs would not necessarily be detrimental to current shareholders, however, the market despises uncertainty and this could cause the share price to further retreat. On the other hand, congress is full of tough talk and weak action so I am skeptical.

Also mentioned above are the labor issues. The workforce becoming unionized could affect profit margins. More generally, the entire labor market is tight at the moment causing shortages of workers and rising wages. Rising wages across the economy will also serve to increase the spending power of consumers which has potential benefits for a company like Amazon.

The market wasnot impressedby Q2 2021 earnings and the stock took a substantial hit. This downtrend may continue while investors exercise caution post-Bezos and post-retail reopening, which is why I recommend incremental buying.

Conclusion

When I see a headline on Seeking Alpha that "Department store stocks rally, while online retailers sell off", I see an opportunity. This development is remarkably short-sighted and unlikely to last.

Amazon's Q2 2021 results have caused many investors to take profits and some to claim that the Company's stellar run is over. The numbers, while tempered from the pandemic highs, are still impressive and a growth runway remains in the Company's most profitable segments. The new CEO will face the coming challenges with heaps of LFCF and the stock's valuation has become more favorable to long-term investors. This is not the first time the stock has pulled back from a seemingly weak quarter and in every instance, the correct move for long-term investors is crystal clear.

精彩评论