Summary

- We have swing traded this stock successfully multiple times.

- At these levels and below, it is a solid investment, but also once again a trading opportunity.

- SOFI truly has a competitive advantage as a result of its horizontally integrated offerings cutting across many areas of fintech and banking.

- The most recent quarter was decent, a banking charter is nigh, and this is going to be a winner you should own.

- This idea was discussed in more depth with members of my private investing community, BAD BEAT Investing.

We recommend buying SoFi Technologies (SOFI) on this most recent selloff. We think the stock is at levels that are strong buys. Period. End of the column. That was easy. But in all seriousness, while having traded this name successfully multiple times, we felt it prudent to put out another piece on the ticker to inform our readers that it is setup once again as both a long-term winner if you enter here, and has the potential for a rapid-return swing trade. While the market has many concerns, with this pullback and considering the most recent earnings, the company is moving right along. We fully believe this will be a solid winner. You should own it.

The stock is down hard from recent highs just weeks ago. Admittedly there may be some volatility, but we think the play is definitely to buy some now, and God willing if this drops more, buy it up.

Make no mistake, there have been some other great companies we still love that are new and growing and the stocks have struggled. We think it's good to go.

The play

Buy 1: $14.30

Buy 2: $14.00

Buy 3: $13.50

Shorter term profit target: $16.50-$17.00

Traders who need a stop should look to jump ship on negative momentum at under 13.00, but we think it is a mistake frankly. Build a position for the longer term.

For call options, consider the January 2023 $15 strike.

Discussion

The story of SOFI remains a great one. We know many who have used it in the years past, as they had attractive rates, terms, and made finance by the people, at least in the messaging. Here we are at the end of 2021, and SOFI now represents the next generation of banking, and plays into a growing fintech industry.

The stock got hit hard when SoftBank recently sold a massive stake. SoFi was also a bit of collateral damage in a recent New York court case, where a New York judge declined to approve Renren's (NYSE:RENN) settlement with shareholders who accused RENN insiders of taking the company's portfolio for themselves in 2018. The portfolio included a large stake in SoFi. Generally speaking, fintech has been weak of late. In fact, a lot of specialty tech has been hammered as we have noted in our chat boards, while the NASDAQ 100 index is largely holding up thanks to mega cap tech.

Regardless of the short term, when you look at SoFi, you have to be amazed at the growth they have shown! They started off as a simple provider of loans in the student loan market, and have since expanded their offerings to encompass a large array of services in the consumer finance sector. They have blossomed and now offer products ranging from personal loans, home loans, and even insurance, credit card services, cash management, brokerage services and recently to payments and financial services APIs for enterprises.

Of course, their diverse and integrated ecosystem of services in a single app has gotten SOFI tremendous user growth, as increasingly frustrated customers of traditional banks opt to switch to SOFI for the ease of convenience.

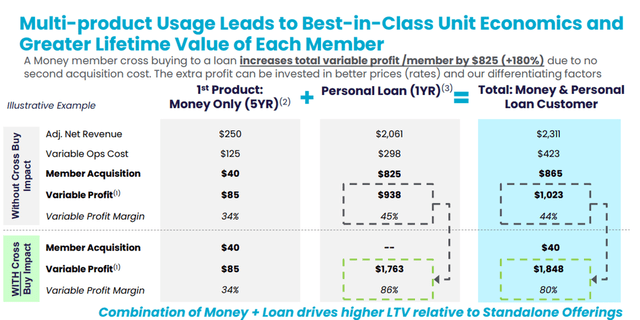

What we love about this company is that it has such a low cost to acquire customers, but makes what a bank makes margin wise with loans. The combination of low-value financial products and high value loans on the same app increases the opportunity that its customers cross-buy into these loans. What is more, since the customer was acquired with low cost into its low-value offerings, the variable profit per customer that comes in and the buys into high-value loans now increases significantly compared to when obtaining that same loan customer through traditional means. In fact, it can increase 180%:

This is absolutely winning. The long-term potential here cannot be understated. That said, the most recent quarter was quite decent.

Total revenue was $272.0 million in Q3 2021 which was up 35% from the corresponding prior-year period. On an adjusted basis, net revenue was $277.2 million, a record high for Q3, and 28% higher than last year's $216.8. Revenues were also up sequentially from Q2. There was continued strength in all three of SoFi's business segments, leading to these solid results, and the top line beat consensus estimates handily by $21.6 million.

Now the major complaint of course for the relatively new public company is that it is not consistently making money on the bottom line. But it will folks. Indeed, SoFi saw $30.0 million net loss for the Q3 2021, compared to a net loss of $42.9 million in last year's quarter.

The one thing to remember here is that the acquisition of Galileo was costly, and they lowered their valuation allowance. Just something to keep in mind. Anyway, we are pleased to see another quarter of positive adjusted EBITDA. It came in at of $10.3 million, and was positive for the fifth consecutive quarter, due to the combination of higher revenues across business segments, though this was a touch offset by increased spending to achieve incremental growth.

One of the most critical items we noted was SOFI continues to accelerate its year-over-year growth in both members and total products in the quarter. This is key. Total members grew 96% year-over-year to 2.9 million, up from 1.5 million at the same point last year, and total products grew 105% to 3.3 million at quarter-end compared to 2.3 million at the same point last year.

This is so critical to understand. The business metrics are largely improving, regardless of the stock moves. The stock is not the company. The company is not the stock. But the stock will recognize the moves in metrics eventually as the noise settles down and things improve. Growth in the member base and products continues to be driven by significant expansion in the offerings across business segments, particularly in the Financial Services segment, where growth in SoFi Invest and SoFi Money offerings more than doubled the number of Financial Services segment products, to nearly 3.2 million, up from approximately 1.2 million, at the same point last year.

As of the end of Q3, Financial Services segment products were nearly three times the number of Lending products.

Growth in personal and student loans largely drove the 15% year-over-year increase in Lending segment products.

Technology Platform accounts increased by 80% to nearly 89 million. All of this is solid growth. The results versus guidance are a key communication from the company that we love to see. It helps hold them accountable.

We won't go incredibly deeper into the numbers but the key here is that the company's performance trounced guidance all around. We do not think management sandbags in order to beat either. The company is simply growing solidly.

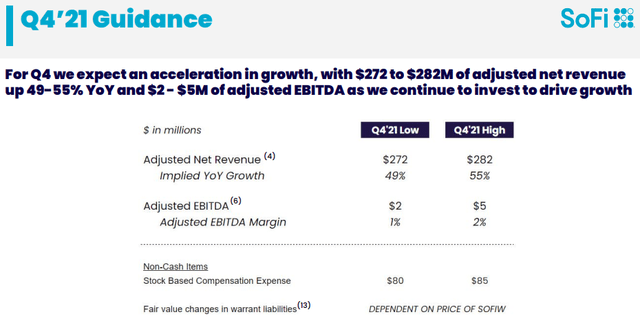

That said, management expects continued strong growth to finish the year. For Q4, they see expected adjusted net revenue of $272 to $282 million and expected adjusted EBITDA of $2 million to $3 million. That is strong growth on the top line:

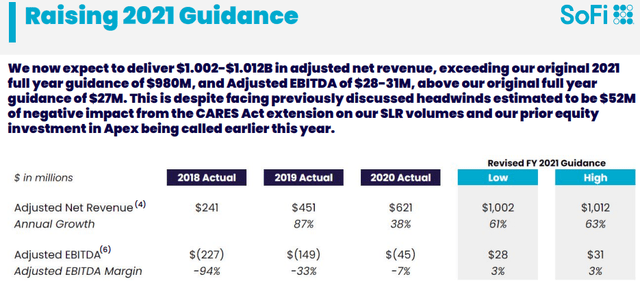

The company also raised its guidance. We love it when companies raise guidance:

Sure, there is a lot of noise around what will happen with rates, and the Fed, and with COVID and the economy. But in perspective, higher rates are good for companies that lend money, so long as they are securing funding at a nominal rate and profiting from a spread. The company sees annual performance being strong thanks to year-to-date performance and a strong Q4. We are most excited by seeing the company break a billion in revenues this year, with EBITDA possibly breaking $30 million. Growth from here is all but guaranteed.

A few catalysts and risks

One thing we want to point out again is how the extension of the government's student loan moratorium has hindered the company. But that is coming to an end. While that was costly in 2021, we expect that 2022 will see a nice boost in repayment. So keep that in mind.

Then there is of course the bank charter, which we see as very likely. For more on this, please see the many columns on SoFi on Seeking Alpha discussing this. We will say that as they have applied for a national bank license, if they get it, there are so many other products they could offer in addition to some other innovative things they could try as it relates to banking products.

Of course, a risk to the stock and to the company's growth would be if they were straight up denied a banking charter. That would hurt potential growth and we could see the stock being sold off pretty hard.

Another risk is if the government comes in and tries to regulate the massive uptick in the number of companies offering customers access to trading, or otherwise tries to limit individuals from trading. A lot of money is made from trading/investing, so any regulation here that limits this could be detrimental. Traders should keep their ears and eyes on the regulatory wire for anything that could hurt SoFi or its competitors in this regard.

Take home

While the company and stock are not risk-free, the pullback has been massive. The secondary, as well as institutional selling, along with broader fintech weakness, has set up a great trading opportunity here. Take advantage of the selloff here and you will thank yourself down the road for buying this gem.

精彩评论