Summary

- Qualcomm is well-positioned to benefit from secular growth trends of 5G, IoT, and industrial and auto connectivity.

- Its recent operating performance has been quite good and momentum should remain strong in the next few quarters, even though growth is expected to moderate in the medium term.

- After a strong stock rally, the upside is now more limited and investors should buy more during potential pullbacks.

QUALCOMM(QCOM) has interesting growth prospects over the coming years supported from 5G, IoT and industrial and auto connectivity, but its share price performance has been quite strong over the past couple of months and Qualcomm is now a ‘hold’.

Background

About two months ago, I have recommended Qualcomm as an interesting play in the 5G and Internet of Things (IoT) secular growth theme, even though there are some medium-term risks, such as competition from MediaTek(OTCPK:MDTKF) in the mobile segment and the possibility of losing Apple’s(AAPL) modem business.

Since my article, Qualcomm’s share price has been on fire, up by more than 39% in about two months, supported by strong earnings and an upbeat investor day in the past week.

After a strong run, I think it’s time to see if Qualcomm still offers value to investors if its shares are now expensive. In this article, I review its most recent earnings and investor day, plus I check if its valuation is still attractive or not, considering Qualcomm’s medium-term earnings expectations.

Recent Earnings

Qualcomm has reported positive results regarding the fourth quarter and fiscal year 2021 (FY 2021 - for the year ended on September 26, 2021), at the beginning of this month. The company reported revenues 5% higher than expected related to Q4, while its bottom-line beat estimates by close to 13%.

For the full fiscal year, the company was able to beat targets set at its investor day in 2019 for revenue growth and margin expansion, boding well for growth ahead.

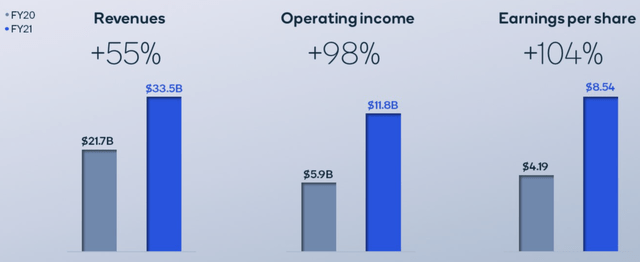

In FY 2021, Qualcomm’s revenues amounted to $33.56 billion (up by 43% YoY), while its operating income was close to $10.3 billion (+80% YoY). Its net income increased by 74% YoY to more than $9 billion, reaching a net profit margin of 26.9% (vs. 22.1% in FY 2020).

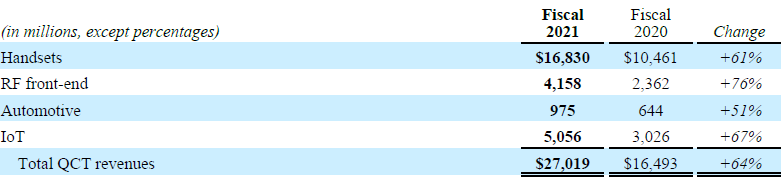

Qualcomm’s growth engine was the QCT segment (technologies), with revenue up by 64% YoY, while the licensing segment (QTL) reported 26% YoY revenue growth. In the QTL segment, Qualcomm’s growth was broad based, with radio filters and IoT being particularly strong.

Despite the company’s diversification strategy, Qualcomm is still heavily exposed to the mobile market (handsets) which represented some 62% of its QTL revenues. However, this weight is expected to gradually decrease over the next few years, as other segments such as IoT should have higher growth rates over the medium to long term, given that handsets have benefitted cyclically from the rapid shift to 5G phones over the past year.

I see these results as quite good and above my own expectations, with the company being able to report annual revenues in excess of $10 billion for RF, auto and IoT together, a great milestone for Qualcomm and more than doubled compared to FY 2019.

This clearly shows that Qualcomm’s diversification strategy is progressing well and execution has been positive, which increases confidence on future growth targets. Beyond that, the current chip shortage is also impacting Qualcomm’s business, like for everyone else in the industry, making its recent growth even more impressive.

Regarding its shareholder remuneration policy, during the last fiscal year, Qualcomm has made close to $3.4 billion in stock repurchases and distributed dividends of $3 billion. Thus, its total capital return to shareholders amounted to $6.4 billion, which represented more than 70% of its bottom-line. However, its dividend yield is only about 1.5%, thus I see Qualcomm mainly as a ‘growth’ play, while income is not high enough to be a reason to buy Qualcomm’s shares.

Qualcomm’s outlook for the next quarter is also positive, with the company expecting more than $10 billion in revenues and diluted EPS in the range $2.53-2.73. Even though Qualcomm’s business has some seasonality, Q1 is usually a stronger quarter, this outlook implies annual revenues close to $40 billion, or up by 19% compared to the previous FY.

This is in-line with current street expectations, given that the current consensus is for FY 2022 revenues of $39.5 billion, showing that Qualcomm’s recent growth is not temporary.

On the other hand, as I’ve highlighted as a potential risk in my previous analysis, there were additional rumors recently thatApple(AAPL) will use its own 5G modem chip in 2023, instead of using Qualcomm’s chips. It is difficult to quantify how much revenue will Qualcomm lose from this, but certainly will be material and is a potential headwind for revenue and earnings growth in the medium term that investors should be aware of.

Nevertheless, the company has recently shown in its investor day that its business is well exposed to some secular growth trends, such as IoT or car and industrial connectivity powered by 5G. This bodes well for its growth prospects over the next few years, and also to smooth the impact of losing some business from Apple.

Investor Day

As I’ve discussed previously on Qualcomm, the company is well-positioned to benefit from secular growth trends of 5G and IoT, considering that it has adapted its product portfolio quite well in recent years for the expected higher demand for these wireless technologies over the next few years, beyond the mobile industry.

Its growth strategy has been to diversify its product offering so that it can offer solutions and products for more industries and different type of customers, namely in the automotive or the industrial sectors, increasing Qualcomm’s total addressable market and higher long-term growth prospects than relying too much on the mobile industry.

The company has several technologies for mobile and connectivity that have great growth prospects due to the ongoing digital transformation, which is not expected to slow down in the future. Indeed, in its recent investor day, Qualcomm said that its total addressable market is expected to expand significantly over the next decade, from about $100 billion currently to some $700 billion by 2030. This is justified by the rising number of devices that are expected to be connected to the internet, generating a vast amount of data, being a strong tailwind for the company’s growth ahead.

Qualcomm also discussed again its technologies spanning several end-markets beyond handsets, with IoT, automotive or virtual reality devices being, in my opinion, segments that are still relatively small for the company and have great growth prospects to become a sizable part of Qualcomm’s business in the next few years. For instance, Qualcomm targets annual revenues from IoT of around $9 billion by FY 2024, compared to $5 billion last year, while in Automotive it expects to grow from annual revenues of $1 billion last year to around $3.5 billion in five years.

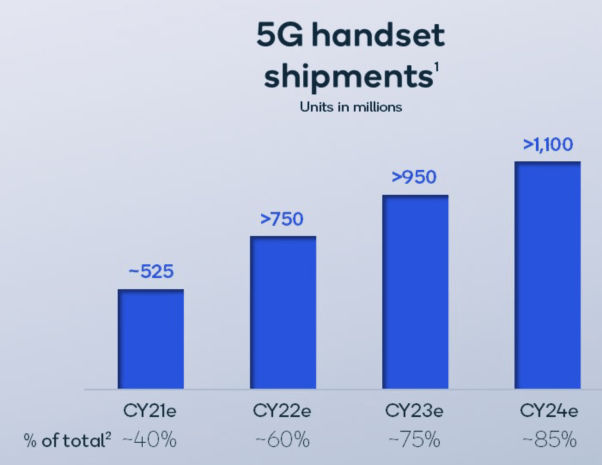

In the mobile segment, Qualcomm also sees good long-term growth prospects due to 5G, with 5G handsets expected to gradually increase the weight in total shipments to about 85% by fiscal year 2024 and double from the total shipments delivered in the last year.

Regarding its capital structure and shareholder remuneration policy, Qualcomm intends to maintain its policy of distributing a large part of its free cash flow to shareholders, both through a growing dividend and opportunistic share buybacks. As the company’s financial leverage is strong, measured by its net debt-to-EBITDA ratio below 0.5x at the end of FY 2021, it doesn’t need to retain much cash so I expect Qualcomm to distribute close to 100% of its free cash flow to shareholders over the next few years.

However, this could change if the company pursues acquisitions, especially if it performs a large acquisition financed mainly by debt. That would increase the company’s financial leverage and, most likely, its strategy would then change towards reducing leverage in subsequent years until it reaches again a strong balance sheet as it has today.

Estimates & Valuation

Regarding medium-term estimates, Qualcomm’s revenues are expected to grow at about 7.3% per year, over the next four years, slowing down significantly compared to FY 2021. I think these are conservative estimates and there is upside potential for upward revisions over the coming months if operating momentum remains strong.

For the fiscal year 2025, revenues are expected to be about $44 billion, which seems too much low considering that for FY 2022 revenues are expected to be around $40 billion. I’m more bullish than current consensus and see revenues of around $50 billion by FY 2025, expecting annual revenue growth of around 7-8% per year between FY 2023 and 2025, which I think is still quite conservative.

Its bottom-line is expected to increase to more than $14 billion in FY 2025 in my estimates, slightly above consensus because I’m expecting higher revenues, which implies an EPS of around $12 by FY 2025.

Regarding valuation, my approach is to look into the next few years of revenues and earnings rather than just focus on this year or the next, to see if the stock has upside potential over a time frame of two to four years. Therefore, I use FY 2025 estimates to see if Qualcomm’s stock has upside potential over the medium term or not.

Based on Qualcomm’s EPS estimate of $12 by FY 2025 and its historical valuation multiple over the past couple of years regarding its blended forward earnings (next 12 months) of 17.3x, my price target for Qualcomm by September 2024 is $207 per share.

This means that Qualcomm’s upside potential, based on these assumptions, is about 15% over the next three years, which is not impressive and show that a good part of its growth in the medium term is already reflected in its share price.

Note that over the past two years Qualcomm’s forward earnings multiple has been somewhat volatile, trading between 13-22x forward earnings. When I wrote my previous article on Qualcomm, its shares were trading at the bottom of this range and the stock was clearly a buy, while now is trading close to its historical value. This means that there is more upside potential over the medium term, as Qualcomm is clearly well-positioned to benefit from 5G, IoT, and industrial and automotive connectivity, thus a re-rating to higher multiples is possible in the next couple of years.

Bottom Line

Qualcomm’s operating momentum has improved markedly in recent quarters and growth prospects are good in the coming years, as the company’s product diversification strategy is making good progress and is expected to support growth in coming years.

However, its stock has rapidly incorporated improved fundamentals with the company’s recent earnings and investor day, and now upside potential is more limited than it was a couple of months ago. Investors who are exposed to Qualcomm should ‘hold’ and buy more during potential pullbacks in the future.

精彩评论