Summary

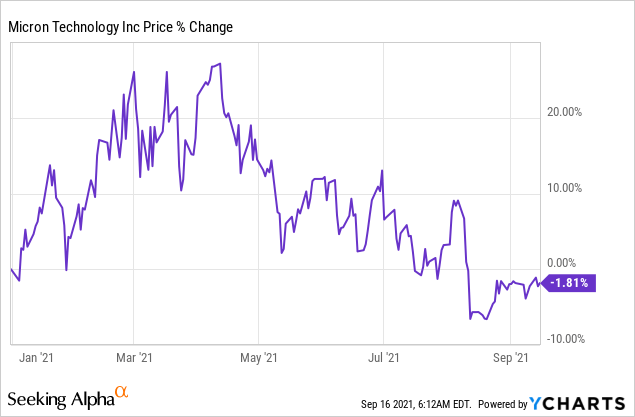

- Shares of Micron just fell into negative territory for the year.

- But, Micron’s revenues and gross margins are still in a period of expansion.

- ASP growth in DRAM and NAND and increased bit shipments could push Micron’s margin closer to 50% in the fourth quarter.

- Micron’s growth is cheap.

While Micron Technology's (MU) commercial performance is excellent, the firm’s shares have trended downwards since April. But with Micron set to open its books for the fourth quarter at the end of September, the memory company could initiate a new upleg.Micron’s growth has a discount valuation

There is a big disconnect between Micron’s business and stock performance. Although the memory firm has enjoyed strengthening revenue growth in its main DRAM business and higher gross margins in FY 2021, shares of Micron have not performed nearly as well. Micron now posts a negative return of 1.8% year to date, but the firm’s fourth-quarter earnings card, set to be put on the table on September 28, 2021, could re-energize the shares.

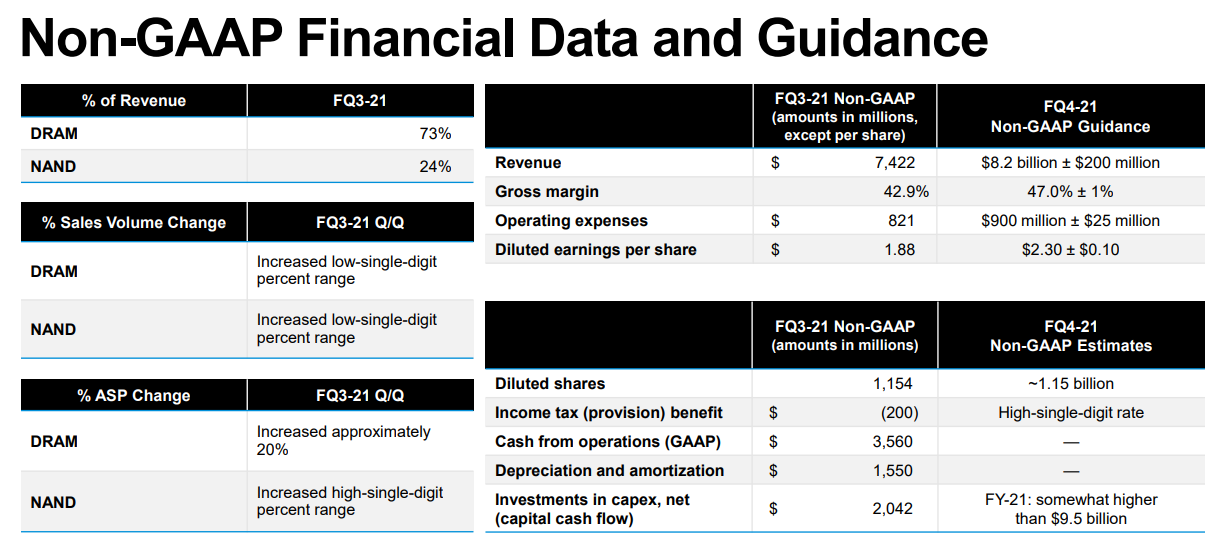

Based off of Micron’s commercial scorecard for the third quarter, the memory firm is in its best shape in years. Micron’s third-quarter revenues soared 36% year over year to $7.4B. The big driver of Micron’s revenue growth this year has been the DRAM business which benefits from strong demand from end markets and increasing average selling prices/ASPs. Micron’s DRAM business generated revenues of $5.4B in the third quarter, showing an increase of 52% year over year and a 23% top line improvement over the prior quarter. DRAM revenues generated 73% of all revenues for the firm and while bit shipments increased only slightly in FQ3’21, average DRAM selling prices jumped 20% quarter over quarter, strongly supporting Micron’s revenue growth.

Micron’s second business, the NAND segment, saw relatively moderate revenue growth of 9% year over year to $1.8B in the third quarter and it is not nearly as important as the DRAM business regarding revenue contribution. The NAND segment represents just 24% of Micron’s total revenues, but the percentage is set to increase going forward as the firm accelerates the roll-out of its new 176-layer NAND node which promises better performance and higher read/write speeds compared to previous gen technology.

Micron’s earnings card for the fourth quarter is just three weeks away, which makes this a good time to discuss what we can expect from Micron’s last fiscal quarter of the year.

Based off of Micron’s guidance, the firm expects sustained business momentum in the fourth-quarter, with revenues expected to shoot up to $8.2B +/- $200 million and gross margins to grow to 47.0% +/- 1%. If Micron hits the base-case forecast, the memory firm is set to increase its revenues 10% quarter over quarter and expand its gross margin by 4.1 PP. In the high case, Micron could generate $8.4B in fourth-quarter revenues (13% quarter over quarter growth) and gross margins of 48.0%, signaling an increase of 5.1 PP, quarter over quarter.

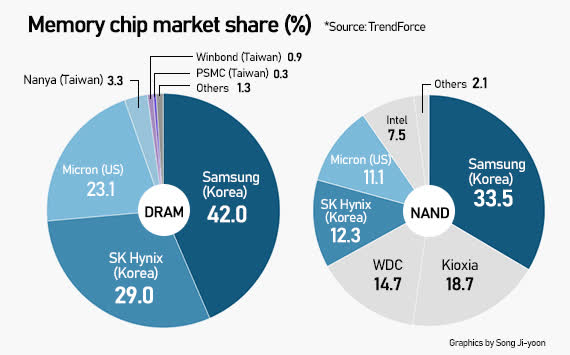

It is likely that end markets remained strong in Micron’s fourth quarter - Samsung and SK Hynix forecasted strong memory chip demand for the second half of the year (Source 1 and Source 2) - and, because of this, that both DRAM and NAND ASPs continued to see quarter over quarter growth. Samsung is the world's largest DRAM memory chip manufacturer by sales and market share, followed by SK Hynix and then Micron. All three companies saw a boost to their earnings in FY 2021 due to strong market conditions in memory chip markets.

The DRAM market is still in a severe supply shortage which is why Micron's average selling prices surged 20% in the last quarter. Micron has said that it expects the chip supply crunch is going to drag into 2022. The supply shortage has its roots in the COVID-19 pandemic and resulted when a quicker than expected rebound in chip demand from the auto industry coincided with surging demand for consumer electronics. By some estimates, the supply shortage could last until 2023.

I don’t expect strengthening DRAM ASP growth for the fourth quarter, but Micron could still see mid-single digit ASP growth in its core DRAM market. For that reason, I estimate that Micron will see an increase in the percentage of revenues generated from DRAM product sales. In FQ3’21, Micron generated 73% of sales from DRAM shipments and this percentage is poised to rise even higher in FQ4’21. Depending on how resilient DRAM product pricing was in Micron’s fourth quarter, the firm could move closer to a 50% gross margin and issue a new, strong forecast for FQ1’22.

Micron’s 1-alpha DRAM and 176-layer NAND nodes will likely have seen higher shipment volumes in the fourth quarter. Longer term, I expect Micron’s NAND business to see stronger growth and Micron’s DRAM business to decelerate as the supply shortage in the DRAM market gets resolved and Micron accelerates shipments of its new 176-layer NAND node. Because of Micron’s investments in NAND innovation, Micron could grow the share of NAND-generated revenues from 24% in FQ3’21 to 30-35% over the next 1 or 2 years.

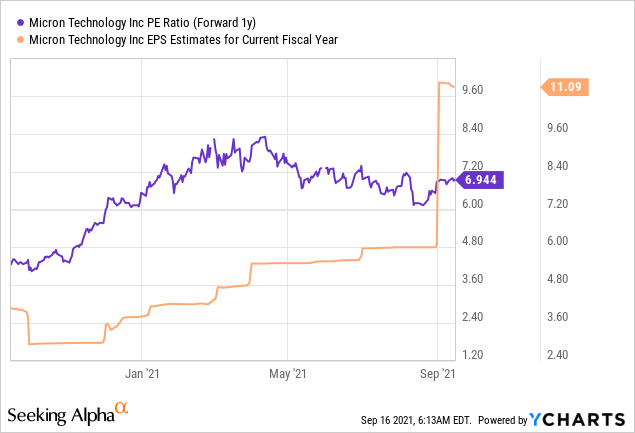

Micron is growing rapidly and there is no indication that this growth is slowing down. Micron is set to add one billion dollars to its top line in the fourth quarter alone, and growth, so far, is still strengthening. Estimates call for $37.0B in revenues (33% year over year growth) and $11.20 in EPS (87% year over year growth) for FY 2022, implying that Micron’s growth is undervalued at an earnings multiplier factor around seven. Micron’s estimates are rising and refreshed updates after the release of the FQ4’21 earnings card could create fertile ground for a new upleg.

Turning to risk, the supply shortage in Micron’s DRAM business fueled DRAM ASP growth this year, but as the market corrects this imbalance, DRAM prices could come down substantially... which is a risk for the stock. Since DRAM sales account for 73% of Micron’s total revenues, falling average DRAM selling prices are poised to weigh on Micron’s commercial performance more than a similar decrease in NAND ASPs would. However, Micron could, potentially, counter some of these DRAM pricing risks by increasing shipments of its newest NAND products. As the company gets ready to scale its NAND business, a decline in DRAM revenues could be counterbalanced by higher NAND revenues. Besides falling DRAM prices, a slowdown in revenue growth and lower gross margins would indicate the end of the current semiconductor cycle and lower capital/stock returns.

Conclusion

For the last fiscal quarter of the year, I expect Micron to table a very strong earnings card with revenues coming in at the top of guidance and gross margins potentially exceeding Micron’s own forecast… which could push shares of Micron into a new upleg.

Due to strength in consumer end markets, ASPs in both DRAM and NAND segments likely grew at a positive rate in Micron’s fourth quarter. Increased bit shipments for 1-alpha DRAM and 176-layer NAND nodes and a DRAM supply shortage all help to set Micron up for continual growth in FY 2022.

精彩评论