Summary

- Fastly is the leading cloud-based content delivery network worldwide.

- Its stock has massively underperformed this year. Its YTD gain of -48.6% is in stark contrast to its massive gains last year.

- We think the stock is undergoing an extended consolidation phase. Its valuation has also fallen dramatically.

- We discuss whether the appropriate time has come for investors to add Fastly stock now.

Investment Thesis

Fastly (FSLY) was a huge winner for investors in 2020. The leading cloud-based content delivery network (CDN) benefited greatly from the "lockdowns-inspired" surge on its platform. However, 2020 has proven to be a challenging time so far. The stock has lost much of its gains from last year. The company also had to deal with the unexpected outage in June. Coupled with the drop in its net revenue retention (NRR), Fastly couldn't escape from its quagmire.

In our previous article in September, We shared that Fastly still offers one of the best cloud-based CDN opportunities for investors. Interestingly, the stock escaped the recent September retracement unscathed. FSLY stock managed a 2.61% gain since our article was published. It outperformed the SPDR S&P 500 ETF's (SPY) 0.54% advance over the same period.

We think FSLY stock is undergoing an extended consolidation phase. Its valuation has undoubtedly fallen off a cliff since the feverish days of 2020. We will discuss whether the current price level represents a reasonable point to add exposure.

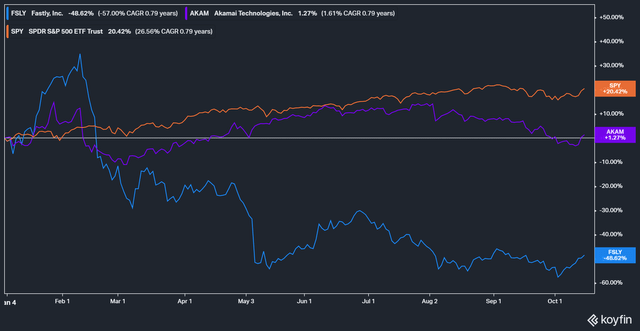

FSLY Stock YTD Performance

FSLY stock has had a disappointing year in 2021. It had a brief momentum surge in February, as its YTD returns reached 40%. However, it soon transpired to be an astute bull trap. The stock's momentum quickly turned bearish. It soon lost all its gains for the year and went into the red. At the moment, FSLY stock is down 48.6%. The stock has been consolidating at a level it first established in May this year. It has significantly underperformed compared to Akamai (AKAM) and the SPDR S&P 500 ETF.

What's Wrong With Fastly's Fundamentals?

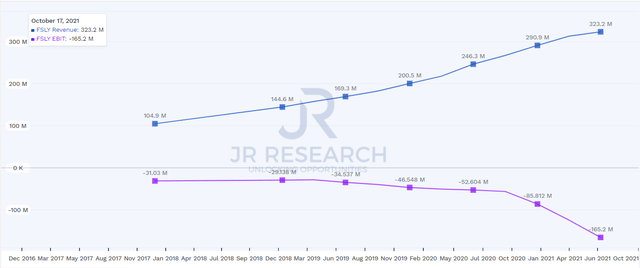

Fastly, Inc.'s business model is based on usage-based pricing. Its revenue enjoyed a massive surge in 2020 as the COVID-19 lockdowns intensified. People were fixated on their mobile and TV screens as they learned the life of being a couch potato.

However, if we look further back, readers will realize that FSLY has already been growing its revenue remarkably. On a last-twelve-months (LTM) basis, Fastly grew its revenue by a 4Y CAGR of 32.5%.

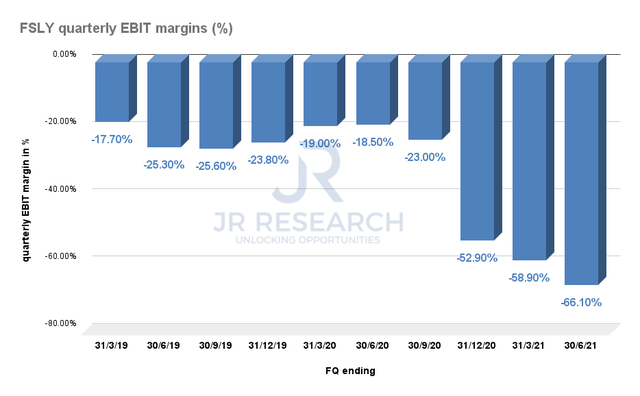

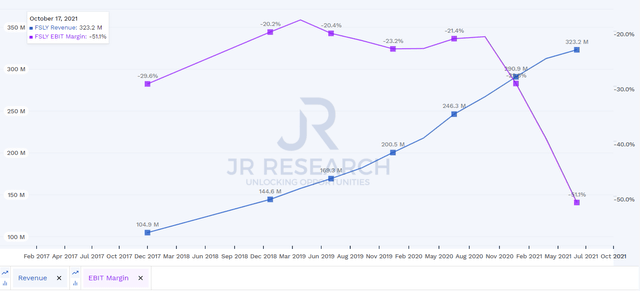

The main problem lay with its EBIT margins. FSLY has undoubtedly been growing its topline swiftly. However, the company's EBIT profile has been deteriorating. The picture is consistent from both the latest quarterly figures and from an LTM basis. FSLY seems to have serious problems with its operating efficiencies as it scales up.

Notably, Fastly's SG&A margin trend follows closely to its declining EBIT margin trend. Therefore, Fastly has not been able to scale efficiently. Its operating efficiencies have been getting worse as it scales. Despite its stellar revenue growth, Fastly doesn't come close to approaching EBIT profitability. Little wonder investors were concerned. Its high valuation before its massive sell-off didn't help matters as well. It was a double whammy for Fastly stock.

Fastly Needs to Show That Its Platform is Sticky

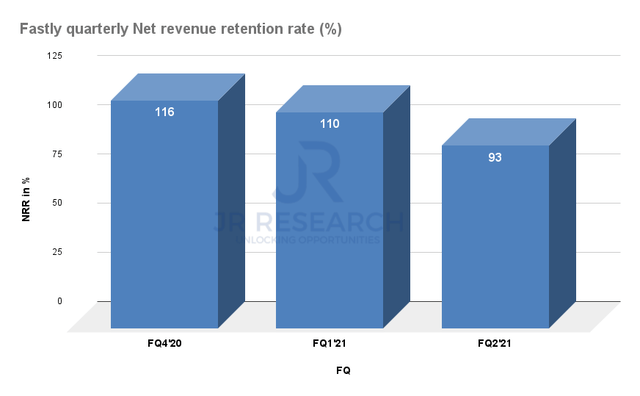

Fastly's net revenue retention (NRR) rate has fallen sequentially over the last few quarters. In FQ2'21, it reached a low of 93%. It clearly shows excessive churn, even though revenue was essentially unchanged from FQ1'21. Fastly pays particular attention to its NRR. The company specifically highlighted: "Our ability to generate and increase our revenue is also dependent upon our ability to retain our existing customers. In addition to measuring expansion using DBNER, NRR and LTM NRR also allow us to track customer retention, which demonstrates the stickiness of our edge cloud platform."

Therefore, a consistently falling NRR rate on its platform doesn't bode well in terms of platform stickiness. Compared to FQ2'20 NRR of 137.8%, its performance in FQ2'21 was hugely underwhelming.

Notably, the company highlighted that it had recovered most of its enterprise usage since the outage. We also discussed it in our previous article. Therefore, we encourage investors to pay attention to its NRR moving forward. FQ3's earnings should reveal telling information on its recovery prospects.

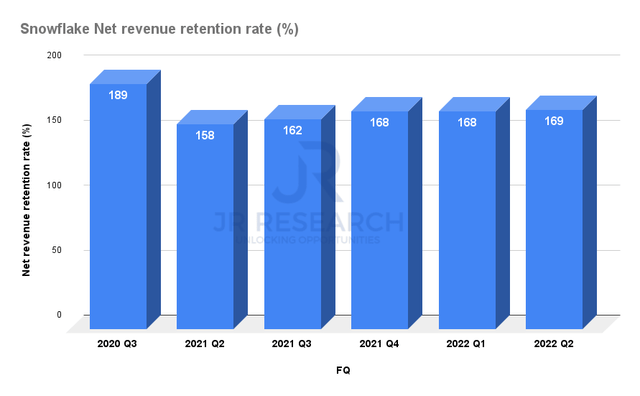

In contrast, we can also observe Snowflake's NRR as a guide. Both companies operate vastly different business models. However, we wanted to highlight that SNOW also uses a usage-based pricing model. But, the company has continued to maintain industry-leading NRR metrics. It clearly shows that its customers have been consistently increasing their usage on its platform. It proves that SNOW's platform growth drivers are highly sustainable.

On the other hand, FSLY's platform might have suffered from tremendous pull-forward effects from last year. As a result, that usage guidance might have been unsustainable. Perhaps, Fastly's business model is more cyclical than it seems. Fastly doesn't break out its enterprise customer base for analysis. Without it, we wouldn't be able to analyze specifically which business verticals they are primarily involved in. However, the company emphasized that they are less keen on competing in the "commoditized" media streaming vertical. Instead, they focus on customers who can provide a more lucrative value-add to Fastly's business model.

Hence, investors should continue to pay close attention to Fastly's NRR metrics moving forward.

Fastly is Still Expected to Grow Rapidly

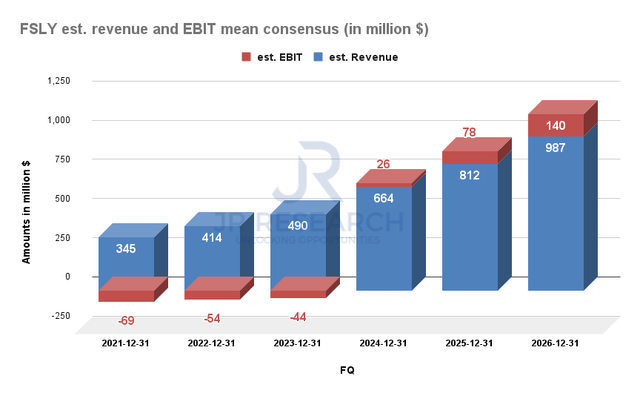

Fastly's estimated 5Y revenue CAGR is about 23.4%. It's a marked deceleration from its historical 4Y revenue CAGR of 32.5%. Therefore, the Street has also marked down Fastly's expected growth rates moving forward. However, it's still in line with Grand View Research's estimates. The research firm postulated that the global CDN market will grow at a CAGR of 22.8% by 2028. Therefore, we think it's reasonable to assume that Fastly can grow in line with market expectations. Hence, we are not unduly concerned with the revised projections for FSLY. In any case, it shows that there are still plenty of growth opportunities for Fastly.

We think executing revenue growth doesn't seem to be a concern for FSLY. The recent misses to its guidance might have been transitory due to the outage. Of particular concern is whether FSLY can improve its operating leverage. Fastly haven't demonstrated that it can cascade down its remarkable topline growth to its bottom line. Mean consensus estimates point to EBIT profitability by FY24. Hence, investors are asked to be patient while FSLY works out its operating leverage.

So, is FSLY Stock a Buy Now?

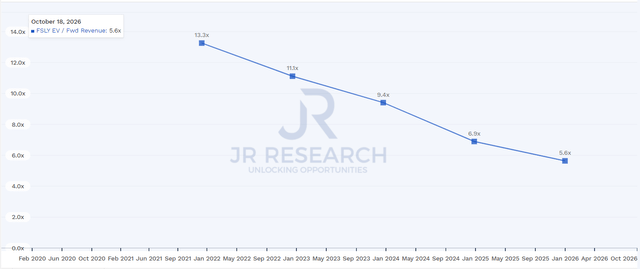

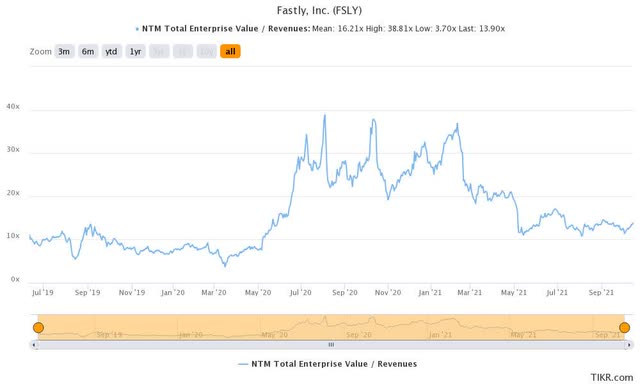

FSLY stock currently trades at a forward revenue multiple of 13.3x. It's noticeably below its 2Y mean of 16.2x. Therefore, it's unequivocal that FSLY stock valuation has fallen dramatically this year. It also trades well below Cloudflare (NET) stock's "nosebleed" forward revenue multiple of 70.4x. However, it still trades well above Akamai stock's forward revenue multiple of 4.6x. However, FSLY is still expected to grow much faster than AKAM. If Fastly could execute better and improve its operating efficiencies, the stock might be rerated moving forward. We remain quietly confident of the stock's opportunities at the current price level. However, the Street's mean target price of $37.13 might continue to be headwinds against its progress.

We are retaining our Buy rating on FSLY stock. However, we wish to caution that we adopt a speculative stance on the stock. Hence, we encourage investors to size their entries properly if they intend to add exposure.

精彩评论