Summary

- In its short history as a public company, Oatly has developed into a battleground stock.

- Recent accounting fraud allegations have caused the stock to give up all of its post-IPO gains.

- Dietary benefits of its products are questionable and consumer preferences for oat milk over other plant-based alternatives may change.

- Trading for 20X TTM sales, its high valuation leaves little margin for error.

- Investors should wait for a better entry.

Investment Thesis

After going public in late May, Oatly (OTLY) shares soared from an IPO price of $17 reaching a high of $29 in mid-June. However, over the last few months, Oatly shares have crashed nearly as quickly following a short report which claimed a series of accounting irregularities were made by the company prior to its IPO.

If these claims are ultimately proven true, Oatly shares will have further room to fall as its shares are currently valued over 5 times their final private funding round just one year ago.

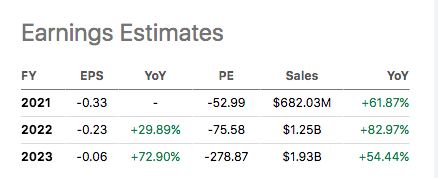

Earnings Projections

Oatly is projecting excellent revenue growth over the next 3 years, with expectations to grow revenue nearly 5-fold during this time. The company may have a massive runway to build out its business, but its competition is strengthening. Oatly is not projecting profitability for at least the next 3 years and paying SaaS valuations for an up-and-coming food company could be a recipe for disappointing future returns.

Riding the Wave of ESG Investing

Continuing Commitment to Doing Right by the Planet

As a people and planet organization, our goal is to drive a positive societal shift towards a more sustainable food system, rooted in plant-based eating, by putting sustainability at the core of our strategy and products. We are a new generation company appealing to a new generation of consumers. The current food system requires change, and we strive to be a driving force behind this change. We are actionably addressing society’s greatest sustainability and health problems, and for that, we believe we will find further success in the marketplace. As a company, we have been on this mission for decades and are not bound by the traditional interests or structures of the food industry. Due to our powerful voice and authentic and clear brand values, we believe we are well-positioned to capture the tailwinds created from these changing consumer behaviors.

Source: Company F-1

In my article aboutBeyond Meat(BYND), I mentioned that one of the appeals of investing in plant-based alternative companies is their sustainability potential. However, relying solely on a company's sustainability focus does not warrant an effective investment decision. It is important to assess the competitive landscape in which the company operates, risk factors which could derail their growth projections, and attempt to determine if there is any defensible economic moat present.

As with Beyond Meat, the company appears to have a massive runway to build out its business.

We participate in the large global dairy industry, which consists of milk, ice cream and frozen dessert, yogurt, cream, cheese and other dairy products. According to Euromonitor, the global dairy industry retail sales were estimated to be $592 billion in 2020 and are expected to reach $789 billion in 2025, growing at a compound annual growth rate (“CAGR”) of 5.9%.

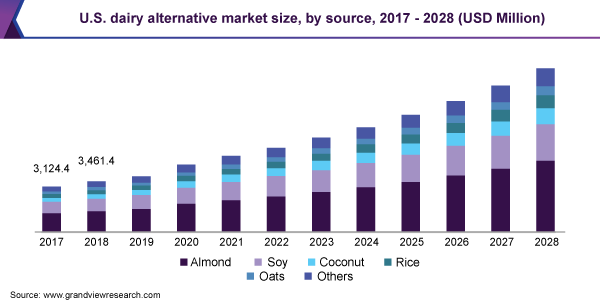

The global plant-based dairy industry retail sales were estimated to be $18 billion in 2020 according to Euromonitor, representing approximately 3% of the global dairy industry (excluding soy drinks in China). Within the global dairy industry, plant-based milk represented approximately 9% of the global dairy milk category (excluding soy drinks in China) in 2020. As of 2020, alternatives in other dairy categories have a penetration of less than 1%, highlighting the opportunity ahead across the broader plant-based dairy sector.

According to Nielsen, sales of oat milk products in the United States grew by 203% year over year from 2019 to 2020. In the United States, oat milk products reached $267 million retail sales during 2020, making it the second largest dairy alternative after almond milk.

Source: Company F-1

Given its current trajectory, oat milk may at some point surpass almond milk as the largest dairy alternative. However, an important question that Oatly investors will need to answer is can the companysuccessfully scale up productionto meet this growing demand?

Our business is focused on the development, manufacturing, marketing and distribution of branded plant-based, and more specifically, oat-based, products as alternatives to dairy products. Consumer demand could change based on a number of possible factors, including dietary habits and nutritional values, concerns regarding the health effects of ingredients, shifts in preference for various product attributes, consumer confidence in plant-based products and perceived value for our products relative to alternatives. Consumer trends that we believe favor sales of our products could change based on a number of possible factors, including a shift in preference from plant-based to animal-based dairy products, economic factors and social trends. While we continually strive to improve our products through thoughtful, innovative research and development approaches to meet consumer demands, there can be no assurance that our efforts will be successful. If consumer demand for our products decreased, our business, financial condition and results of operations may be adversely affected.

Source:Company F-1

Oatly is aware that consumer preferences may change and they have highlighted this as a unique risk to their business in their F-1. By betting on only one form of plant-based dairy alternatives, the company is making a substantial bet on just one of the horses in the race to replace dairy from our diets.

Alternative Dairy Competition

The industry is expecting a 13.3% CAGR growth through 2028, growing to over $50 billion in market value.

With Oatly being valued at over $10 billion and increased competition to contend with, the best outcome for the company appears to be priced in. If one wants to get exposure to this fast-growing segment of the food sector, I would recommend purchasing shares in SunOpta (STKL) instead. As a private label producer of various dairy alternatives, it trades for just 1.5X TTM sales compared to 20X for Oatly. The company has exposure to many types of dairy alternatives and is expanding production with a new mega factory which will enable the company to double its production capacity over the next 5 years.

Putting all your eggs in one basket is usually a risky long-term strategy. Oatly's lack of diverse dairy alternative products could put it in a precarious situation should consumer preferences for its oat milk specialty start to wane.

精彩评论