Summary

- Fisker is on track to deliver its first vehicle by November 2022 and in line with the previously laid down cost structure.

- The finalized Foxconn deal of mass-producing an electric vehicle justifies the current valuation.

- The announcement of a climate-neutral vehicle goal by 2027 strengthens the long-term outlook.

- Fisker has a robust balance sheet position to support significant investments in product development and innovation.

Fisker (FSR) is up more than 65% since the publication of our previous article on Fisker last month (Fisker: High Risk, Very High Return) with a “very bullish” rating. Therefore, we believe now was the time to revisit the stock and revise our rating. After revisiting the stock, we continue to remain bullish as the mispricing persists and valuation fails to incorporate the long-term growth potential of the stock. However, valuation offers favorable risk-reward metrics to enter the stock but does not offer the same extraordinary returns with low risk as before, therefore, we would now reduce the rating from "very bullish" to "bullish".

We like Fisker's visionary leadership, competitive product, asset-light business model, and solid partnerships. This article focuses more on updates after our previous coverage, risk reward metrics at current valuation, and strengths that can help expand product portfolio. If you haven’t read our previous article, we highly recommend having a quick look to gain a better understanding of the overall business and strengths.

Business Summary

Fisker Inc. is a California-based EV company focused on designing and developing electric vehicles. Its first vehicle, Fisker Ocean, an electric SUV, is expected to be ready for sale by November 2022. The manufacturing process of Fisker Ocean is outsourced to Magna (MGA) that has an annual capacity to produce 240,000 units. The company went public in October 2020 through a reverse merger with a SPAC. (Source)

What changed since our previous coverage on Fisker?

The company signed an MOU with Foxconn (OTC:FXCOF) in February 2021, which later got converted into an agreementin May 2021. As per the agreement, Foxconn and Fisker will co-develop and manufacture an electric vehicle that would hit the market by Q4 2023 and will be sold under the Fisker brand name in North America, Europe, China, and India. The expected capacity of the vehicle would be 250,000 annually worldwide. The vehicle would be priced under $30,000 and would be a five-seater.

In the recent stockholders’ annual meeting, Fisker reassured that it was on course to deliver its Fisker Ocean in November 2022. It also reassured that it has sourced majority of parts for its first vehicle, and the cost structure is in line with expectations laid out by the company last year. The company announced its goal to produce a fully climate-neutral vehicle by 2027. It also announced plans to exhibit its Fisker Ocean vehicle at the LA Auto Show in November 2021.

Vision to make the world’s most sustainable vehicles

The company was founded with a vision to build the most sustainable vehicles in the world. So far, the company has been on track with its progress. Fisker Ocean has a solar roof that besides delivering a higher range to the vehicle, also generates a free of cost and greenest form of energy source. The company also uses recycled material within its car. In line with its vision, the company set a goal to produce a fully climate-neutral vehicle by 2027 with net-zero greenhouse gases over its lifetime.

Well-positioned to expand vehicle portfolio

Two major partnerships with international contract manufacturers (Foxconn and Magna) uniquely positioned Fisker to grow its vehicle portfolio and reach its goal of four vehicles by 2025. The partnerships enable it to make vehicle design and development the center of attention for the company, have an asset-light business model, build confidence among top suppliers, and enhance negotiation capabilities with suppliers.

In collaboration with Fisker, Magna will also develop a new ADAS feature that includes digital-imaging radar technology. The technology would be coming with Fisker Ocean initially and can be levered to all the upcoming models of Fisker and will play a material role in differentiating Fisker from other automotive manufacturers. The company is also expected to have one of the fastest development times for a vehicle of 2.5 years which can be more than 4 years for most of the automotive OEMs.

We believe that the company is well-positioned to grow its portfolio by leveraging its existing technology, partnerships, and unique asset-light business model. It outsources multiple areas where it believes that differentiation is not important such as manufacturing process, fleet management services, lease financing, other related services, etc. This helps the company focus primarily on product innovation and development, unlike other companies with their hands entirely filled.

More upside potential

As we discussed in a previous report, the Foxconn deal alone can generate $3.75Bn+ annually in revenue (after 3 to 5 years). Similarly, based on conservative estimates of 50,000 Fisker Ocean vehicles at an average price of $50K, Fisker can generate $2.5Bn annually starting 2023 from Fisker Ocean. Both combined are still greater than the current market capitalization of $5.5Bn despite a 65%+ price return in the last one month.

Furthermore, the company can deliver more than 20% growth in the medium-term (after 2025) even after the above two revenue sources are realized. This is because the company can continue to grow by adding more vehicles to its portfolio with the help of an asset-light business model, visionary leadership, and strong partnership.

The stock can justify its valuation based on estimates of barely two vehicles with a forward P/S ratio (FY3) of less than 1 as per our estimates discussed above. Announcement of the other two vehicles' development as per the company's defined 2025 goal would exponentially boost the company’s outlook and shareholder’s returns.

Risk to Thesis

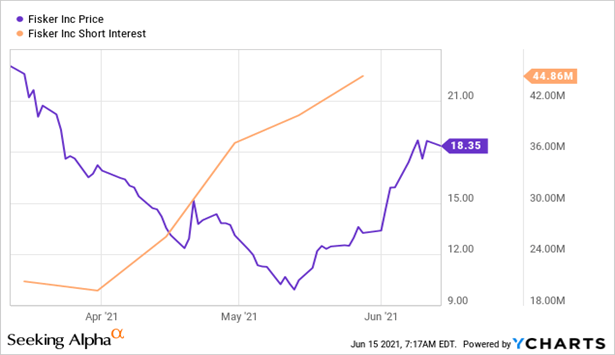

Rising short interest

Short interest has gone up significantly in recent months. Increased pressure from short sellers can push the stock downwards. Besides that, Fisker can also become a victim of short-sellers' attacks due to its lack of revenue and salable product. Short-sellers might publish short-seller reports citing unproven concerns and push the stock downwards for personal gains. This can lead to tarnishing the firm's reputation, which can reduce the ability to secure additional financing, credibility among suppliers, disrupt existing partnerships, as well as impact demand for its vehicles.

Conclusion

The stock continues to offer immense upside potential at the current valuation based on its growth trajectory. Asset-light business model ensures that equity dilution would be insignificant as capital requirements are lower than other EV startups like Workhorse (WKHS) and Lordstown (RIDE) (that are at the risk of facing liquidity crisis when they enter mass production). Moreover, Fisker has zero balance sheet debt and strong liquidity position of $985Mn to support R&D, CapEx, and Marketing costs. Fisker is still one of the best pure-play EV bets currently in the market despite the recent boom in stock price. We expect the stock to double in the next 2-3 years.

The stock would also see increased investments and recognition in the near term asit will be added to Russel 3000 index, which can lead to upside potential for stockholders.

精彩评论