Summary

- UiPath is the leader in robotic process automation, which is a promising market with strong growth tailwinds.

- The company grew ARR at a 58% clip in the latest quarter.

- Guidance for the next quarter was robust, but underappreciated due to the stock having traded much higher earlier.

- I rate shares a buy as one of the more attractive growth stories today.

UiPath (PATH) is one of those “Cathie Wood” stocks (it makes up 3.5% of all Ark funds) that have seen their valuations stripped quickly over the past few months. PATH is now trading below its IPO price in spite of having materially grown its underlying business over that time period. I have previously expressed cautiousness based on valuation, but my concerns have subsided amidst the tech volatility. I rate shares a buy based on the attractiveness of the underlying growth story and reasonable valuation.

PATH Stock Price

After pricing its initial offering at $56 per share and closing that day 23% higher, PATH peaked then headed on a straight downward trajectory to its current $41 price, which is notably below the IPO price.

Like many other tech peers, the recent volatility has shined a spotlight on the promising story stocks which were largely ignored by Wall Street veterans due to their bubbly valuations. Now, those stocks, like PATH, suddenly are trading at much more reasonable valuations, with many in clear buyable territory.

UiPath Stock Earnings

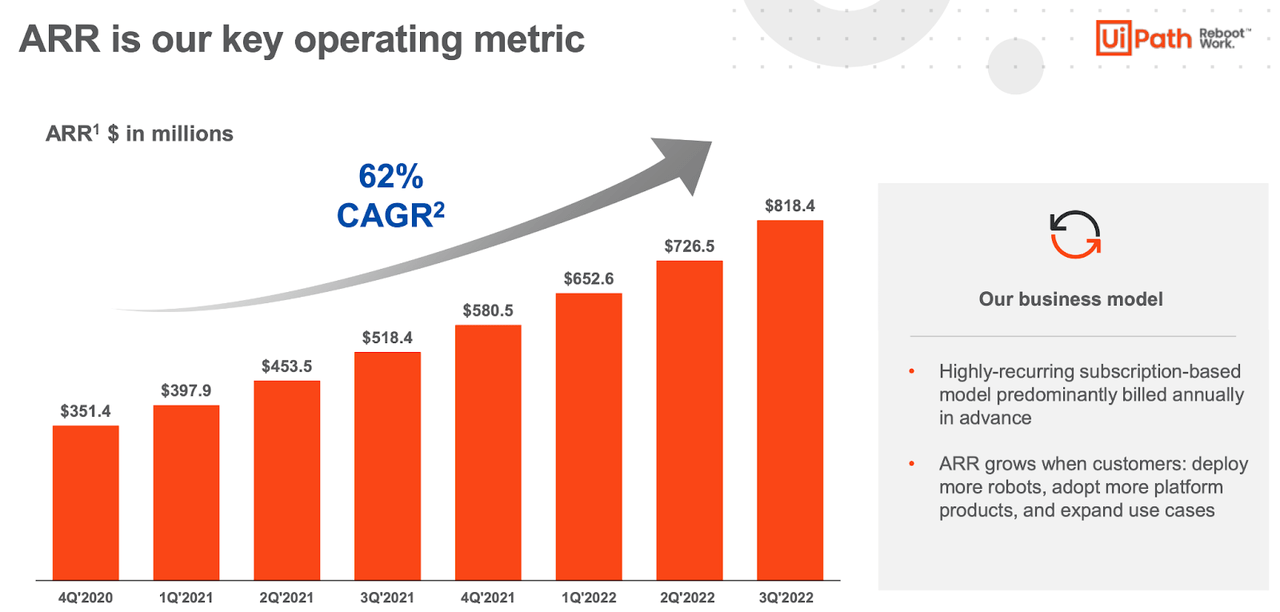

PATH was able to show strong growth in the latest quarter, with annual recurring revenue (‘ARR’) growing at a 58% clip. While this is a deceleration from the 62% average growth rate since the end of 2020, it nonetheless is a very impressive achievement.

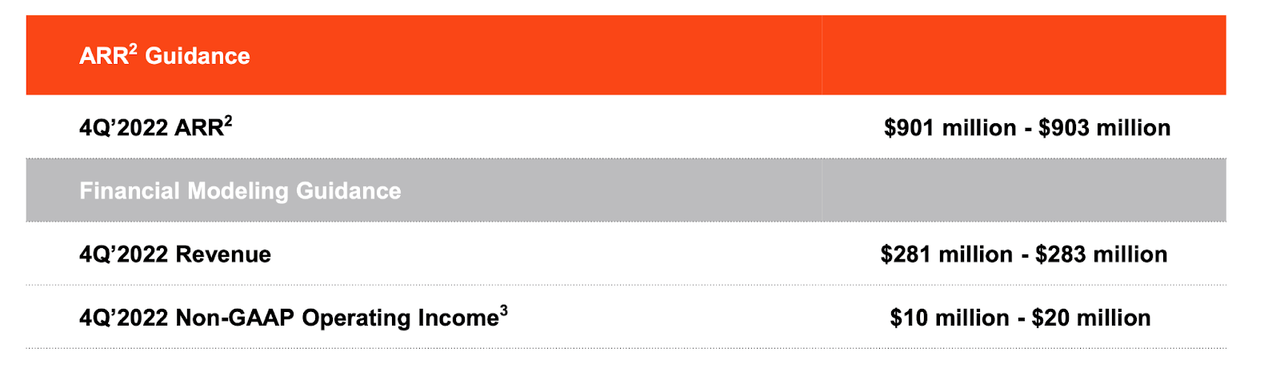

The company also saw non-GAAP operating margins rise sequentially from 3% to 4%. This is the third consecutive quarter of non-GAAP profitability, and the company expects to complete the year with another profitable quarter.

While this technically does not constitute “true” profitability, as non-GAAP results ignore the hefty stock-based compensation, the company undoubtedly benefits from its free cash flow positive profile. I expect free cash flow to rise steadily over the coming years as operating leverage takes hold. The 56% projected ARR growth is solid and does not reflect the same deceleration seen at many other tech peers.

Revenue or Annualized Recurring Revenue

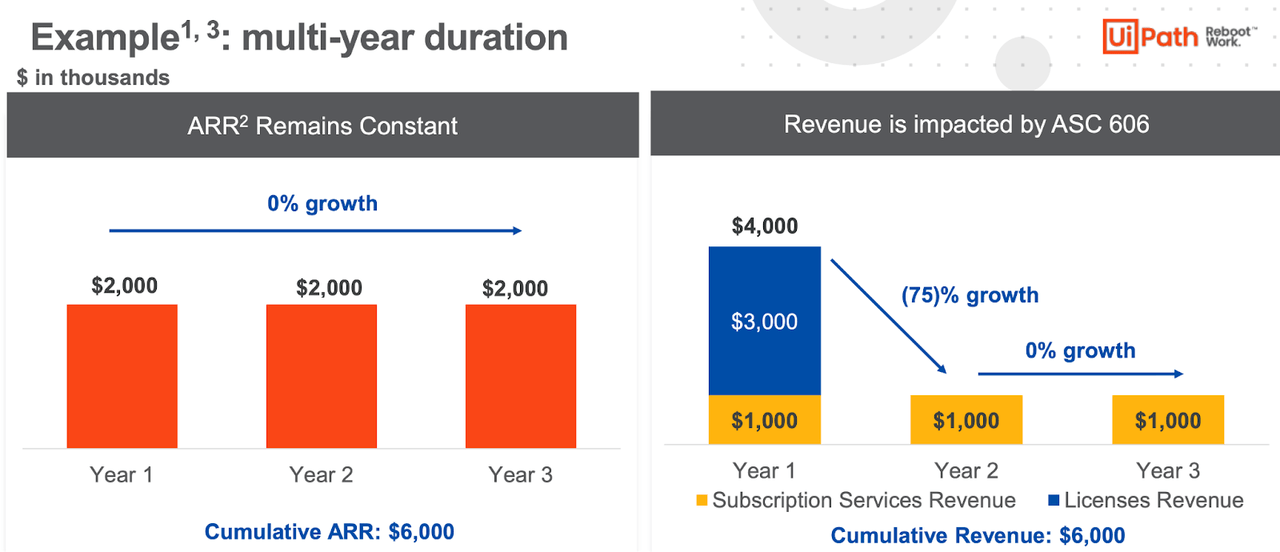

With PATH, it is worth discussing that the company wants Wall Street to look at ARR instead of revenue. What is the difference? ARR is calculated as taking total subscription revenues, dividing by term length, and multiplying by 365. Revenues, on the other hand, differs in that license revenues are recognized in the first year, since that is technically when the “product” is delivered. We can see below an example of this difference in action.

As we can see above, normal revenue would see growth drop off in subsequent years since all of the associated revenues would have only been recognized in the first year. In ARR, on the other hand, the revenue gets evenly distributed across its term, hence the term “annual recurring revenue.” I expect there to be a substantial discrepancy between revenue growth and ARR growth, which much of Wall Street might be quick to misinterpret as a deterioration in the business (but something that the reader will understand to be irrelevant).

Is PATH Stock A Buy, Sell, or Hold?

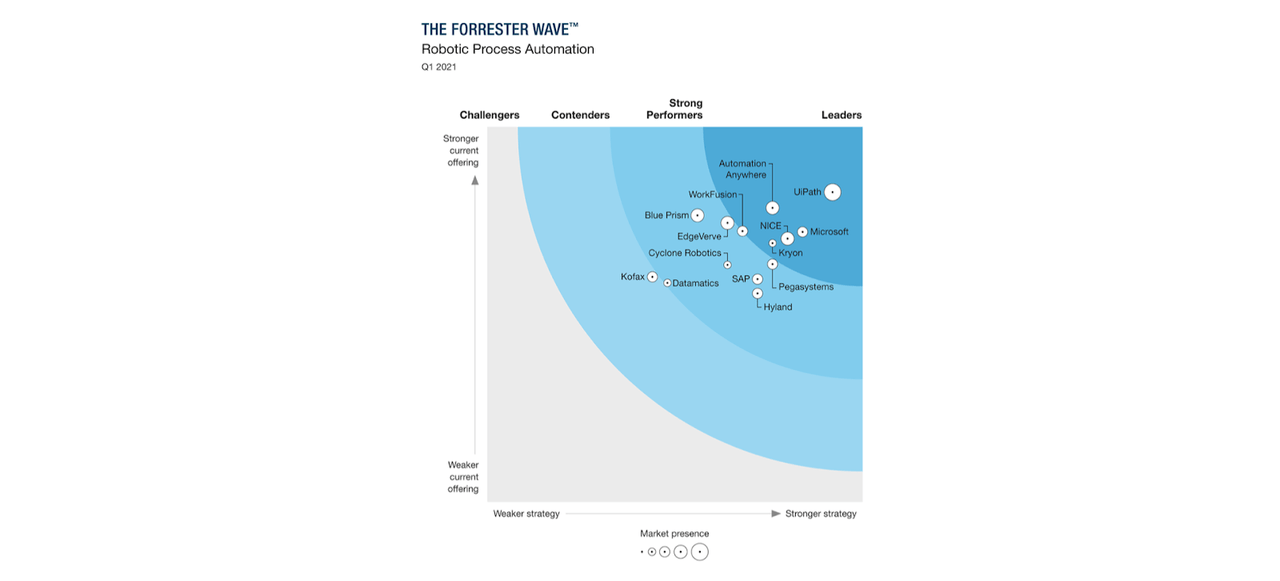

Previously in the year, I expressed cautiousness on the name as the valuations remained steep in comparison with the risk profile. Many investors tend to grow pessimistic when stocks fall so aggressively. It is tempting to think that something is wrong in PATH’s business to warrant or even justify the steep declines. Yet that is not the case and we must remember that it is only the valuation of PATH that has been impaired - or improved for the better. PATH is ranked as the clear leader in robotic process automation (‘RPA’).

I consider RPA to be a strong secular growth story because of humans’ incessant pursuit of efficiency. There are so many human tasks that can be automated and doing so helps improve both accuracy and save costs. As a result, I think Wall Street consensus for around 30% growth over the next few years is reasonable if not potentially conservative.

PATH is the kind of stock that I could see trading at a 2x price to earnings growth ratio (‘PEG’) due to the attractive secular growth tailwinds discussed above. Assuming 40% long term net margins, PATH is currently trading at a 1.5x PEG ratio, which may allow for some multiple expansion in addition to robust growth rates. I note that PATH has $1.8 billion in net cash, which is somewhat significant considering the $21.7 billion market cap. The company’s free cash flow positive profile may enable a share repurchase program, although I find it unlikely considering the slim 5% FCF margin. One key risk is that PATH is not as cheap as other high quality peers and thus may be ever-vulnerable to further downside. Another important risk is the potential for the company to not achieve my expected profit margins. However, PATH can be considered lower risk than cash guzzling peers, making it easier to buy the stock at these multiples. I rate shares a buy with moderate 25% to 30% upside - I expect that shareholders can achieve returns resembling underlying growth but while maintaining the current PEG ratio.

精彩评论