Summary

- Roku's decelerating revenue growth rates are one part of the story.

- The other part is that active accounts growth is slowing down, which has an overarching impact on the business's prospects going forward.

- Why ROKU stock is still not in the bargain basement, even now.

Investment Thesis

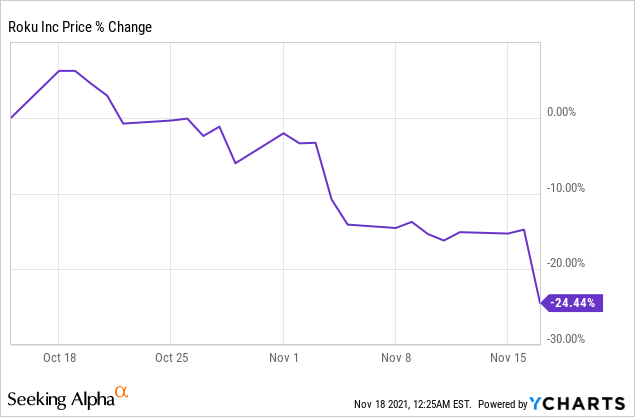

Roku (ROKU) has fallen out of favor with investors, with shareholders selling the stock at a rapid clip.

But as we go through, I make the case that investors shouldn't be too quick to buy the dip here. Indeed, I contend that paying 10x forward sales for the Platform business is not as cheap as it looks, particularly given that the growth in active accounts is slowing down.

Investors Sentiment Turns Negative For ROKU

Two weeks ago I wrote about Roku saying,

Having to pay 11x forward sales doesn't leave new shareholders to the stock with a large margin of safety. Best to avoid this name for now.[...]

I believe that the market has underreacted to Roku's near-term prospects.

Interestingly, even though the market's reaction post-earnings was muted, I took a rare bearish stance on Roku. Given that I've been a Roku shareholder in the past and that I was lucky enough to get out with meaningful gains, I have very positive associations with the company's prospects. To paraphrase Daniel Kahneman, I've been primed to like the stock.

So let's unpack why I'm bearish this name.

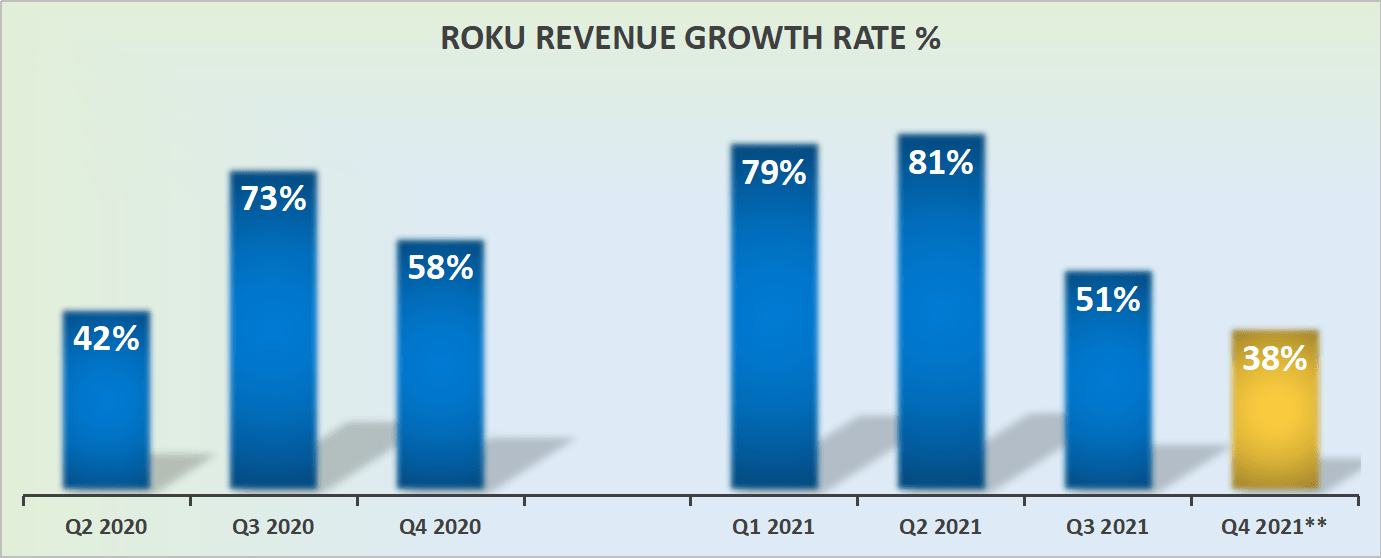

Roku's Revenue Growth Rates Point to Maturing Business

Throughout 2020 and into early 2021, Roku's growth rates were incredibly strong. What's more, as I've often stated, as long as the share price is going up, nobody is going to ask difficult questions about their investment.

But when the share price starts to turn lower, then, all of a sudden shareholders start to get anxious and become all-too-eager to book gains that they hold. This causes selling, which in turn, forces shareholders to revisit the question of why they are holding onto the stock.

And the problem here has less to do with Roku's growth rates into Q4 2021 but everything to do with what Roku's growth rates will be in 2022? That's the key to this investment thesis, can Roku's growth rates stabilize in the high-30s%? Or will its growth rates start to dip closer to the low-30s% and high 20s%?

These two different scenarios have dramatic implications on the multiple that investors would be willing to pay for the stock. But I get ahead of myself, first let's take a step back and understand that not all revenues from Roku have the same worth.

Not All Revenues Are the Same

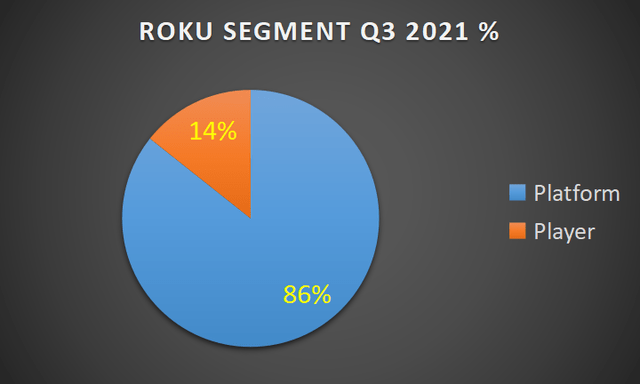

Roku's revenues are made up of two different segments, it has its Platform business that carries all the appeal, and it has its Player segment.

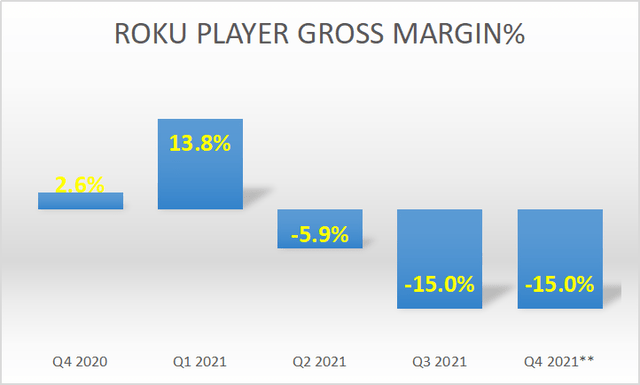

The Player segment comes from streaming players, in essence, hardware products, that have historically been sold at close to breakeven to bring more households onto its network.

The more Players that are sold, the more active users Roku gets onto its Platform, the more profitable the company as a whole becomes.

In that light, it makes a lot of sense to even incur minor losses on the sale of its hardware products, just to get eyeballs onto its network.

During the earnings call, management stated that,

The global supply chain disruptions will likely impact the overall holiday season in terms of shipping delays, product availability issues and product price increases.

Thus, I've estimated that the pricing headwinds from Q3 remain into Q4, the all-important holiday season. This could translate into slightly better or slightly worse gross margins for its Player segment, but I believe it's probably the right ballpark, at negative 15% gross margins.

So Why to Price the Hardware so Cheaply?

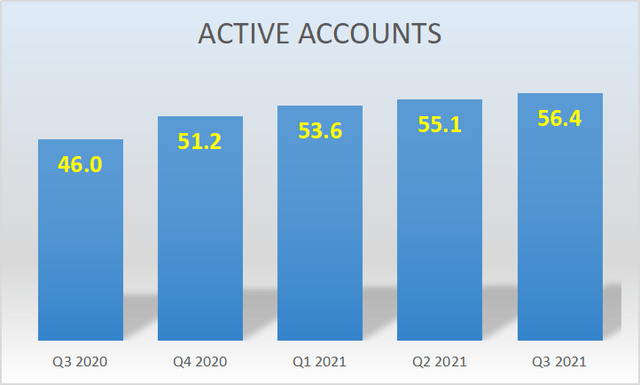

Roku sets the hardware cheaply to drive an increase in active accounts. But as you can see here, the sequential growth in active accounts is steadily decreasing from an 11% increase sequentially from Q3 2020 into Q4 2021 to just a 2% increase sequentially from Q2 2021 into Q3 2021.

The point here is not to get too focused on the actual numbers of active users, but to understand the overall trajectory. It appears that the growth in active users has been slowing down for a while, and if that's going to persist, that further reinforces the thesis that Roku's strong revenue growth rates are starting to mature.

Valuation - Understanding Roku's Multiple

As I've already highlighted, only approximately 85% of Roku's revenues actually carry any profits, that is its Platform revenues.

Thus, if we use analysts' estimates that Roku's revenues reach $3.8 billion of revenues in 2022, that means that only approximately $3.2 billion of those revenues are actually worth anything.

Of its Platform revenues, the gross margins typically oscillate around 65%. This is meaningfully lower than Pinterest's (PINS), which carry nearly 80% gross margins, but higher than Snap's (SNAP) which has around 55% gross margins.

This implies that investors are paying 10x next year's revenues for Roku's advertising or its Platform business, compared with 9x for Pinterest's and 15x forward sales for Snap.

Thus, altogether, it's difficult to argue that even now, after this difficult sell-off in its share price, that Roku is priced in the bargain basement.

The Bottom Line

At the end of my previous article, I concluded with,

When investing, don't seek out ideas that with 50/50 or even 60/40 chances of working out positively. Seek out ideas that have a 70/30 chance of working out favorably. I hope this works out well for you. Good luck.

I stand by that comment today. Paying 10x forward sales for Roku's Platform business requires a very high level of conviction that its revenue growth rates will be able to reignite back up to 40% CAGR. I fear that will be far from easy, particularly as we look out to H1 2022 and the very tough comps Roku will have against this year's H1 2021 period.

In conclusion, I believe that there are better investment opportunities to deploy my capital into right now.

精彩评论