From "gamma hammers" to "gamma unclenching", the cycles of pump, dump, and BTFD has been unrelenting this year, with the pattern around options expirations becoming more and more pronounced since May...

The surge into these 'overwriting' funds...

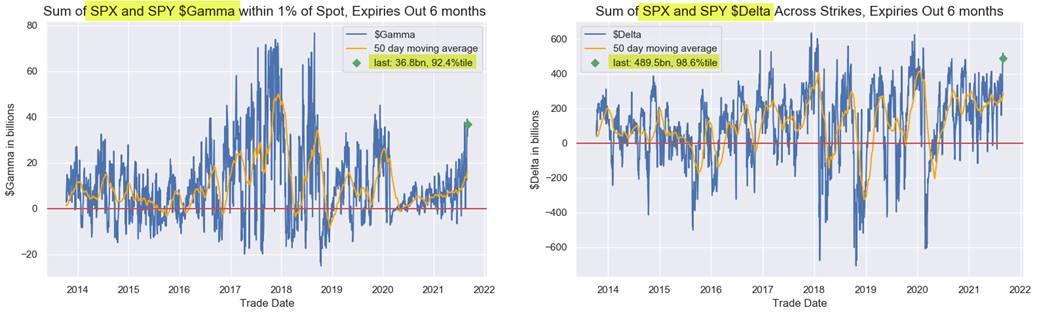

...has stuffed dealers to the gills with gamma and delta exposures at extreme levels...

The cumulative flows from the “Gamma Hammer” strangle-seller alone (2 clips a day, ~3x’s a week in approximately 2-3 week expiration 20d strangles) has Dealers long ~$3B in Gamma (and at a cost of nearly ~5.0mm / day in decay) - which means that for a generic 100bps selloff, desks would in theory be in the mkt buying ~$2.5B of futures - which in-turn prevents any nascent selloff from developing thanks to said “insulation”

Which is obvious when we see there hasn't been a 3bps drawdown since May...

...as the now well-publicized Op-Ex cycle “volatility expansion” phenomenon (VIX 15th, index / ETFs 17th and set-up for another large “Gamma unclench” occurring while then too losing aforementioned Vanna- and Charm- supports into this large serial / qtrly expiration) coinciding with the “buyback blackout”kicking-off for US Financials in that 3rd week of September… and all ahead of the FOMC on the 22nd

Specifically, McElligott notes thatThe Fed timing here is particularly meaningful- not because the potential for an “official” announcement of “tapering” is some massive deal to markets (I believe we are well past that now) - but more because the potential for movement in the Committee’s economic projections and thus, the “dots,” which could cause some Rates upheaval after being firmly parked within their own range-trade hellscape for the past two months themselves (UST 10Y yields ~1.10-1.40).

And because of the potential for US Rates volatility around / after the 22nd Fed meeting as the market resets expectations on both the future path of hikes (off the new economic projections) and tapering,I think this “event risk” could then decrease the supply of “short vol” which has been conditioned to step-in the moment that volatility typically expands(i.e. around the Op-Ex cycle, which has finally gone “mainstream” and seemingly now trades like it too….see this past weekend’s write-up from Bloomberg “Options Turn Upheavals Into a Mid-Month Sure Thing for S&P 500”).

This could mean a longer period without the support that comes from said “short vol” flows reflexively swooping-in to save the day, which over the past decade + have acted to reset nascent spikes in volatility and stop the bleeding—IF this time we were to see those flows on hold due to the FOMC event risk a week later, their potential absence could allow for the “delta one” flow to hold more sway than usual of late (all that EPIC $Delta from index / ETF options as a source of de-risking flow, as well as Vol Control strategy de-allocation supply into an rVol move higher off of such an absolutely low base).

精彩评论