Summary

- SoFi’s member growth accelerated in Q2’21.

- The FinTech reiterated its FY 2021 outlook regarding revenues and EBITDA.

- With strong growth ahead, shares of SoFi are a buy.

SoFi Technologies (SOFI) is growing its platform at a rapid rate and steadily rolling out new financial service products to improve customer monetization. SoFi posted impressive revenue gains Y/Y and the FinTech is set for continual growth. The stock is a buy!

Why SoFi Technologies is a buy

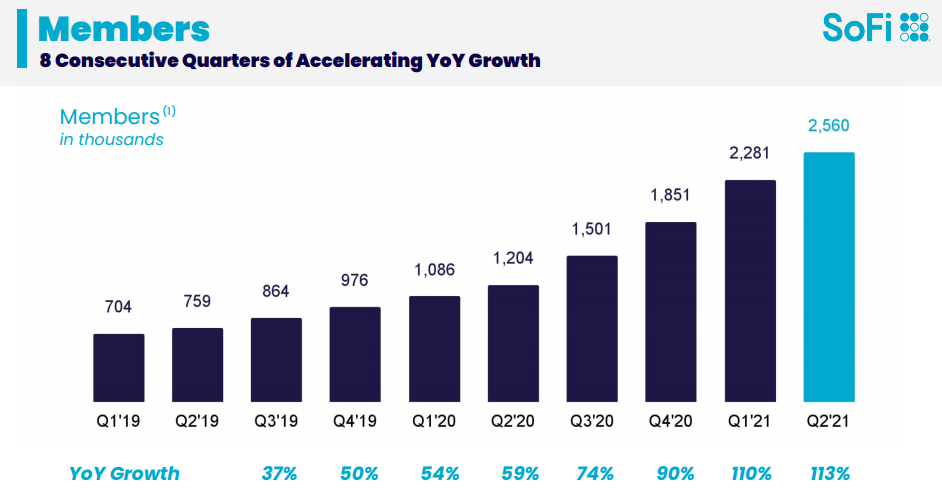

SoFi is a rapidly growing FinTech company whose customer count has really taken off in the last two years. Members - which is SoFi’s term for its customers - have grown from 759,000 in Q2’19 to $2.56M in Q2’21, which is equal to an annual growth rate of 84%. SoFi’s growth accelerated during the pandemic as more people relied on mobile devices to bank and invest. Although the pandemic effects have started to wear off and people returned to work again in Q2’21, the FinTech continued to see strong Q/Q growth in its customer base. SoFi signed on 279,000 new members in the last quarter, which is an increase of 12% Q/Q. If SoFi continues to grow at this rate, the firm should see at least 3M members by the end of the year.

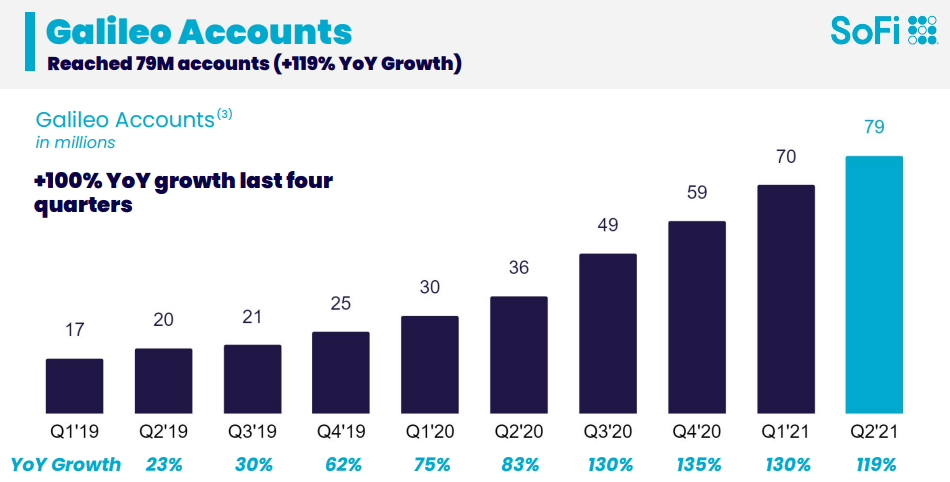

Besides offering lending and financial services products, SoFi owns a payment processing platform aimed at the enterprise market. The digital payments platform operates under the brand “Galileo” and it has also seen strong continual customer growth. Growth in Galileo accounts moderated slightly in Q2’21, but still grew 119% Y/Y. During the last quarter, Galileo gained 9M new customers and the FinTech had 79M customer on its digital payments platform at the end of the quarter.

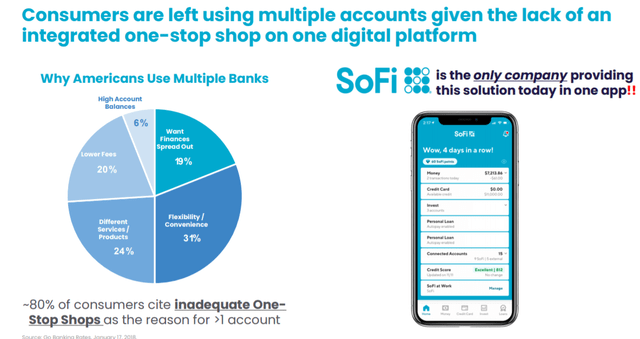

The strength of SoFi's personal finance platform is that it provides a one-stop banking solution for customers that require more than just one product. A customer that needs student loan refinancing may also need a credit card or purchase a mortgage financing solution from SoFi Technologies. Once a customer is signed on to the platform and part of the ecosystem, SoFi can target the member with customized offers.

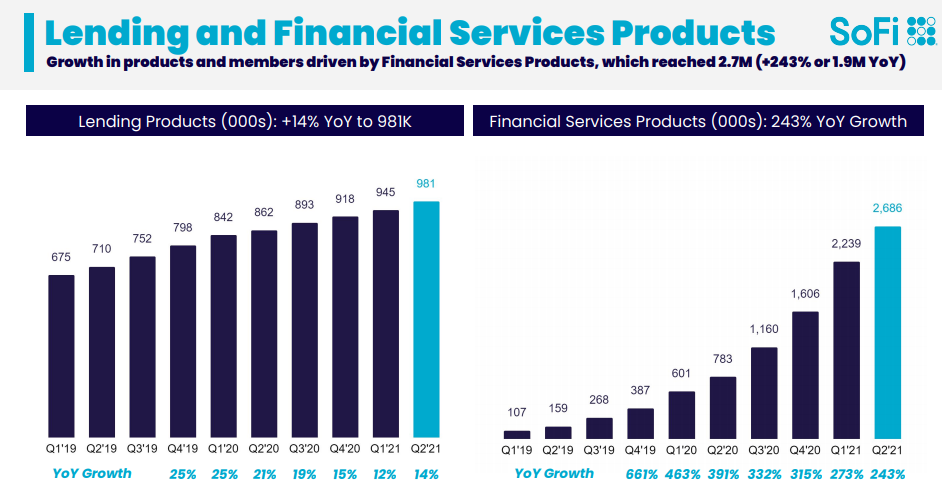

SoFi does a good job at that. The firm rolled out more tailored products in Q2’21, with strong growth present in the financial services category. The biggest growth opportunity for the FinTech is financial services and the firm is adding new products to improve uptake and customer monetization. Financial services products grew 243% Y/Y to 2.69M and are the driving source behind SoFi’s revenue growth.

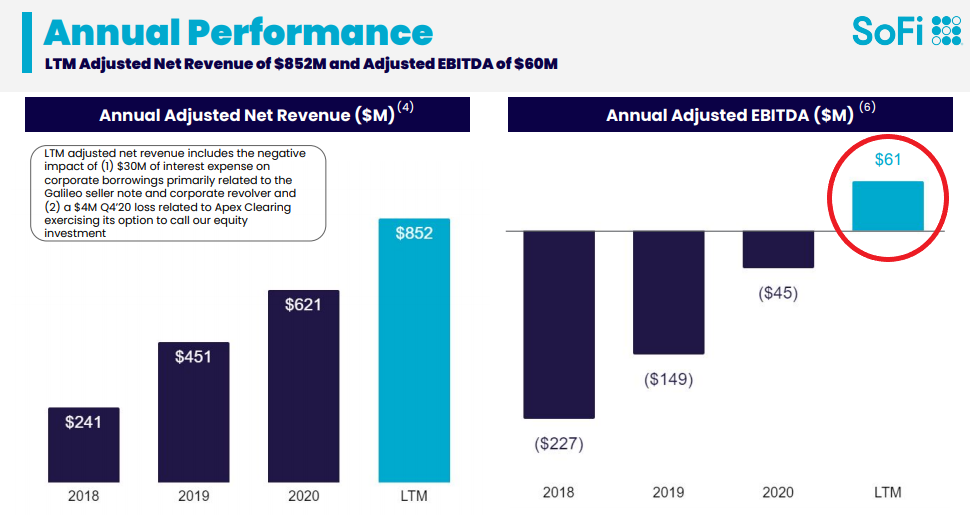

The second-quarter is generally a strong quarter for SoFi. Revenues for the second-quarter were $237M, showing growth of 74% Y/Y. SoFi’s Q2’21 adjusted EBITDA reached $11M which means the personal finance platform has been profitable for four straight quarters. The FinTech’s total adjusted EBITDA over the last twelve months totaled $61M on revenues of $852M.

Strong liquidity, low debt

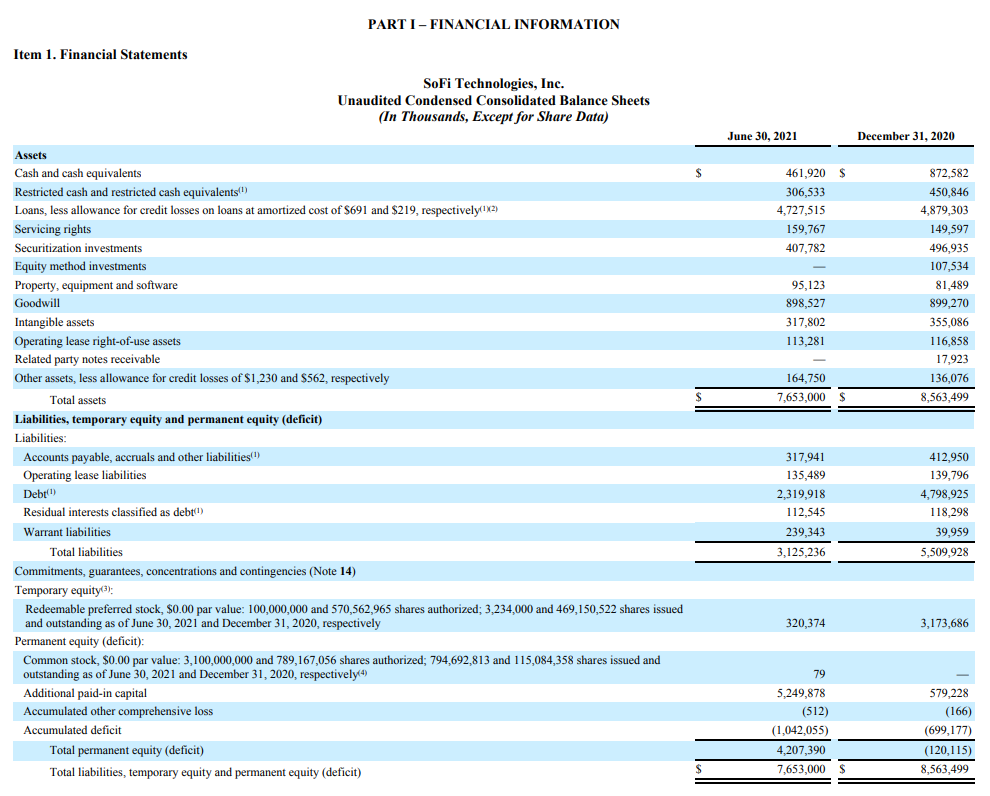

As a FinTech company, SoFi’s main assets are the personal finance and payment processing platforms it owns, and the human capital behind it. SoFi carries $2.3B of financial debt and is flush in cash… with $462M directly available for the firm’s digital growth strategy.

Buy, buy, buy

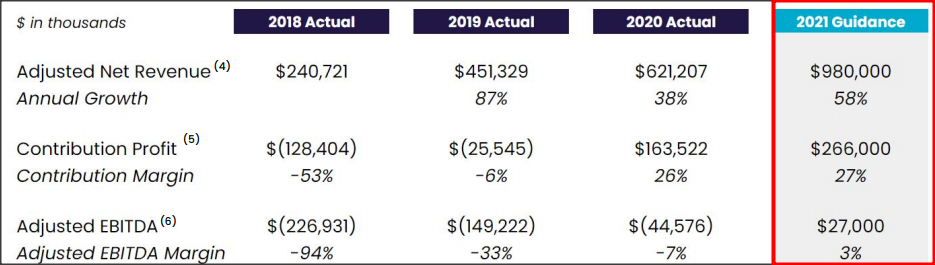

SoFi reiterated its outlook for the rest of the year and continues to project $980M in revenues and $27M in adjusted EBITDA for FY 2021. The personal finance platform also expects to see its first positive EBITDA margin this year. The guidance implies 58% Y/Y growth in revenues with strong momentum continuing in member acquisition.

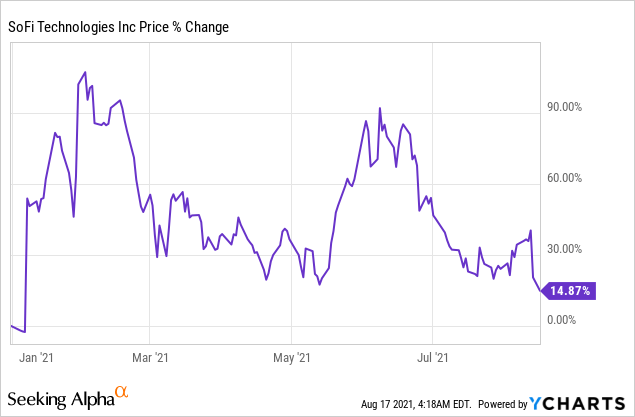

Although SoFi reiterated its guidance and the earnings card was showing continual growth along key metrics, shares of SoFi slumped 14% last week...

The drop creates another buy-the-drop situation for SoFi since the company is just at the very beginning of its growth. If current growth rates prove to be sustainable, SoFi could have 10M members by FY 2025 and revenues of $3.6B. Revenue estimates imply very strong revenue growth for at least the next four years. Based on expected sales of $1.5B in FY 2022, shares of SoFi trade a P-S ratio of 7.6. In June, shares of SoFi traded at a P-S ratio of 11.0.

Risks with SoFi

FinTech companies can be hard to value because they are growing fast and have small or no profits. Although SoFi is profitable regarding EBITDA, the FinTech continues to post net losses… and it will likely continue to do so for a few more years as it prioritizes member and platform growth.

Personalized banking is a growth opportunity in the FinTech sector, but not only for SoFi. The pandemic accelerated FinTech adoption and other digital payment companies are making moves to expand their platforms.

SoFi has no perceptible moat in its platform business which poses a challenge to long term profitability and customer retention. Other banks/FinTechs can easily enter the market and offer similar, better or more differentiated financial services products. Declining member and revenue growth rates are possibly the two most defining risks for SoFi at this point in time, with delayed profitability being only a secondary risk.

Final thoughts

SoFi’s second-quarter was good: Member and revenue figures kept surging and the FinTech continued to roll out new financial services products, the firm’s fastest area of growth. The full year revenue outlook was reiterated, showing that the FinTech is confident in achieving its business goals. The slump after earnings creates another buy-the-drop situation for SoFi as the FinTech gets ready to reach 3M customers by year-end. Buy, buy, buy!

精彩评论