Summary

- The Fed's outlook of lower for as long as possible was just what stocks wanted to hear.

- However, that has sent US yields soaring.

- The higher yields will force a massive repricing of equity valuation.

- Looking for a helping hand in the market? Members of Reading The Markets get exclusive ideas and guidance to navigate any climate.

The Fed gave the equity market exactly what it wanted, lower for as long as possible. Unfortunately, the bond market doesn't seem as pleased, which will be horrible news for the stock market. Rising rates are crushing growth and technology stocks, and soon the rest of the market will follow because there are very few if any "cheap" sectors left in the market.

In essence, the Fed will let the economy run hot, and the bond market does not seem the least bit comfortable with that. Rates are rising sharply on March 18, with the 10-Year now trading just under 1.75%. The curve continues to lift because the bond market fears that a hot economy could quickly overheat, causing prices to rise, and inflation becomes an issue.

It leaves the door open for the Fed to start having to taper its bond purchases and to raise rates much sooner than expected and potentially much faster than indicated. This is resulting in bond yields pushing higher. Additionally, there's a tremendous amount of debt coming to the market, with another round of fiscal stimulus passed, and more supply will need a lot more demand.

While the news at first seems to be everything the stock market wants to hear, it's not good news. In fact, there was very little the Fed could have on March 17 to please both the stock and bond market. The Fed chose to placate the stock market. But stock prices are derived from interest rates, and as interest rates rise, stock prices need to reprice. They have been repricing and shall continue to reprice at lower levels.

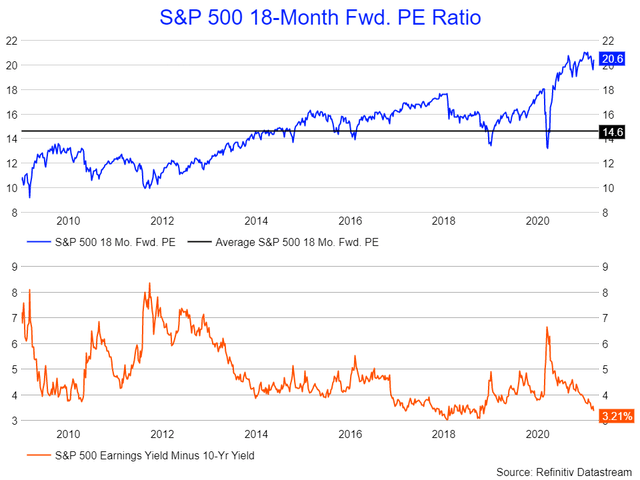

The problem is that now, relative to the 10-year note, the S&P 500 has a valuation on par with the periods in January 2018 and October 2018. At no other time in modern history has the index been this expensive on a relative basis in this low-interest rate world. Everything changed in 2008 when we flipped from a high rate to a low rate world, so the period of 1999 would not be a fair comparison.

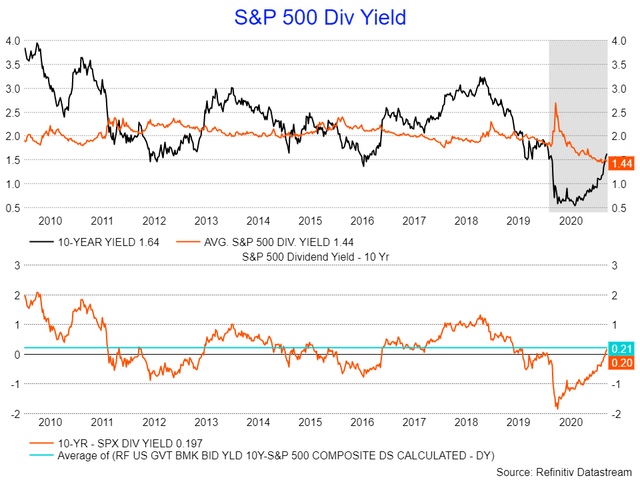

From another angle, the S&P 500 dividend yield is currently around 1.44%, and it has only been lower one other period in time, at the turn of the century. And now, the 10-Year once again has a higher yield than the S&P 500. So will the 10-Year yield pull the S&P 500 dividend yield over time? It seems possible. Since 2010 the 10-year has traded with a premium over the S&P 500 dividend yield of 21 bps. It is currently 20 bps, which means that a movement high in the 10-year from this point is likely to result in the premium growing wider, or dragging the S&P 500 yield higher along with the 10-year.

The rising yields in the bond market have prompted investors to refocus from growth and technology stocks to value and reflation stocks. The problem is that there is no bargain sector left - there's no "value" trade. The cheap stocks are cheap for a reason and because they have weak fundamentals. Over the past six months, the top ten holdings in the S&P 500 Value ETF have skyrocketed.

| Name | Symbol | 3/18/2021 | 10/31/2020 | % Change |

| EXXON MOBIL ORD | XOM | 58.25 | $ 32.62 | 78.57% |

| BANK OF AMERICA ORD | BAC | 39.9274 | $ 23.70 | 68.47% |

| JPMORGAN CHASE ORD | JPM | 161.48 | $ 98.04 | 64.71% |

| WALT DISNEY ORD | DIS | 193.735 | $ 121.25 | 59.78% |

| CHEVRON ORD | CVX | 106.65 | $ 69.50 | 53.45% |

| INTEL ORD | INTC.O | 64.98 | $ 44.28 | 46.75% |

| BERKSHIRE HATHAWAY CL B ORD | BRKb | 255.2 | $ 201.90 | 26.40% |

| JOHNSON & JOHNSON ORD | JNJ | 161.1501 | $ 137.11 | 17.53% |

| AT&T ORD | T | 30.245 | $ 27.02 | 11.94% |

| VERIZON COMMUNICATIONS ORD | VZ | 56.095 | $ 56.99 | -1.57% |

The banks have risen sharply and for good reasons because yields have risen and spreads have widened. But even the banks are getting stretched with many trading at all-time highs, and the sector trading at valuations not witnessed since 2017, relative to the 10-year Treasury rate, making the banks one of the least overvalued sectors. The industrial sector has only been this expensive relative to the 10-year rate one time and that was in January of 2018, which was followed by nearly two years of going nowhere.

Sure, there may be some value left out there in the materials and energy sector. But these two sectors are highly correlated to the commodities they represent. As the dollar begins to strengthen, those commodity prices are likely to begin falling rather sharply, dragging the sectors lower with them. That dollar seems poised to rise.

The dollar initially began to fall following the fears of inflation, but that quickly reversed when US rates began to rise again. That allowed the spread between global rates to widen. The spread between the US and German 10-Year now stands at 2%, while US and Japanese 10-years are at 1.65%. The wider the spreads get, the more attractive US yields become. This will bring foreign investors to buy US bonds, sell local currency, and buy US dollars, supporting the dollar and boosting its value.

Source: TradingView

The rising dollar already has helped to bring oil prices off their highs, and that's a trend that's likely to continue as the dollar strengthens further. Oil has already broken down from a technical standpoint after failing at a key level of resistance around $66.50. It has additionally broken a major uptrend, with a drop below $59.50, sending the commodity back to $54. This could easily reverse the very hot rotation into the energy sector.

Source: TradingView

If the economy will continue to improve, and the Fed is more than happy to let it, then there's no reason yields shouldn't continue to rise. The more they raise, the more the dollar will strengthen, and the more overvalued equities will grow on a relative basis, forcing a massive repricing.

精彩评论