We had been waiting for a long time for Airbnb (ABNB) to enter the stock market, as we are fans of its house renting platform, but were deeply disappointed that its shares have never traded at what we consider reasonable prices.

It seems we are not the only ones liking their platform, seeing the number of downloads of its app on the Google Play Store exceeding 50 million, and with an average rating of 4.6/5.

On the other hand there is Booking Holdings (BKNG), which has traded in the stock market for over 20 years, and has not experienced as much hype recently as Airbnb has. It actually has more downloads and a better app rating than Airbnb. The Booking app has been downloaded more than 100 million times and has a 4.7/5 rating.

Source: Google Play Store

Beyond their namesake apps, Airbnb acquired Lastminute.com, and Booking Holdings owns other very popular websites and apps including OpenTable, Kayak, and Agoda.

1. Reason #1 Business model

Both companies have very strong platform business models that benefit from network effects. People looking for travel accommodation tend to search first on the site with more/better options, and property owners tend to list their offerings on the platforms with more users. This creates a powerful network effect that reinforces the dominance of the platform. The main difference in the business model is that while they both compete on demand side of the platform for travelers, on the supply side Booking mostly features hotels while Airbnb has properties owned by individuals. We prefer Booking's focus on hotels given that it is more reliable and has less regulatory risks.

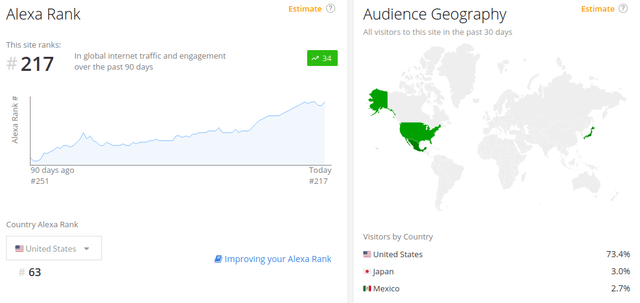

Another important business model difference is the market focus. Looking at Alexa.com we see that Airbnb is only the #217 most popular website worldwide, but it is #63 in the United States. Most of its website traffic comes from the USA, with some significant contribution from Japan and Mexico.

Source:Alexa.com

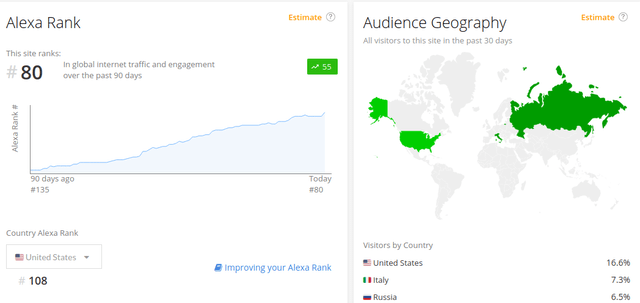

Meanwhile Booking is a lot more popular internationally, with its website being the #80 in the world, but #108 in the USA. Its website visits are a lot more distributed around the globe, with the USA as the most important contributor, followed by Italy and then Russia.

Source:Alexa.com

While both companies have relatively similar platform business models, we believe the focus on professional supply and international focus is somewhat preferable, but it can be said that both companies operate attractive and successful platforms.

2. Reason #2 Regulatory issues

One big advantage Booking has is that by focusing on hotels it is not at odds with city and national government the way Airbnb is, with many cities battling the company over taxes and zoning rules.

Source: Wired.com

There is some nuance to this point, since Booking is starting to add alternative accommodations and Airbnb has lastminute.com which focuses on hotels, but in general it is fair to say that the accommodation supply on Airbnb tends to be more problematic in terms of regulations or lack thereof.

For readers interested in a more in depth look at the issues cities have with Airbnb we recommendthis Wired article. Below we include an extract detailing the type of legal issues the company is facing:

"Read my lips: We want to pay taxes,” Chris Lehane, Airbnb’s global head of public policy,told the nation’s mayorsin 2016. In the years since, the home-sharing site has repeated the declaration in press releases,op-eds, emails, and onbillboards. On its website, Airbnb says it is “democratizing revenue by generating tens of millions of new tax dollars for governments all over the world.”But when Palm Beach County, Florida, a popular tourist destination, passed an ordinance in October 2018 requiringAirbnband other short-term rental companies to collect and pay the county’s 6 percent occupancy tax on visits arranged through their sites, Airbnb sued.Palm Beach County tax collector Anne Gannon wasn’t surprised. “We knew we were going to get sued,” she says. “That’s what they do all over the country. It’s their mode of operation.”

3. Reason #3 Valuation, valuation, valuation

If the 3 most important things in real estate are location, location, location. When investing the 3 most important things are valuation, valuation, valuation.

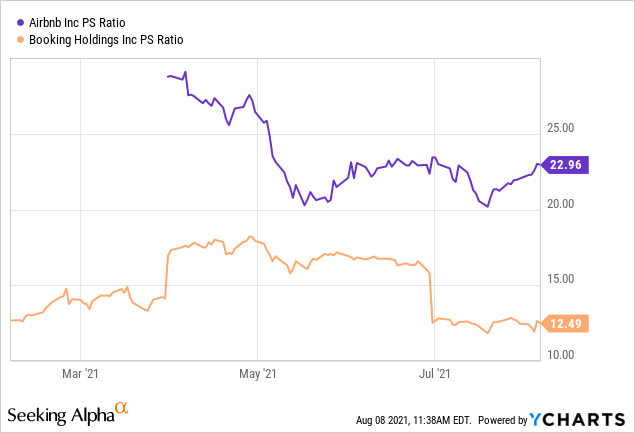

Despite the similarities between the two companies, investors are paying almost twice for a dollar of revenue for Airbnb compared to Booking.

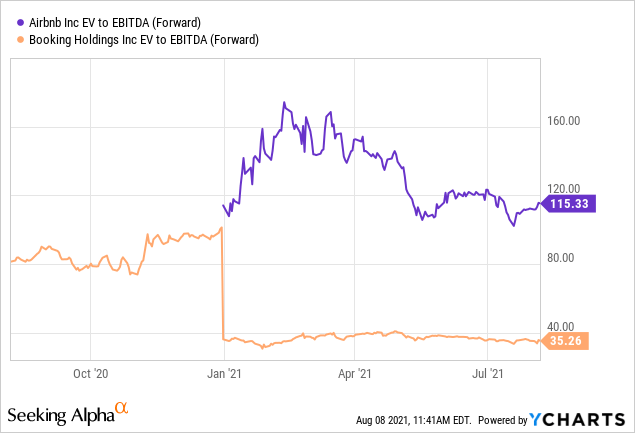

Similarly a quick look to the EV/EBITDA multiples shows again that investors are valuing Airbnb at a huge premium to Booking. Below we show the difference, with EBITDA being the estimate for the coming year (i.e. forward estimate). We do not think it is reasonable to value a dollar of earnings from Airbnb at more that 3x a dollar of earnings for Booking.

It could be argued by some that the valuation difference is due to faster growth by Airbnb, so we will proceed to compare both companies using a DCF model.

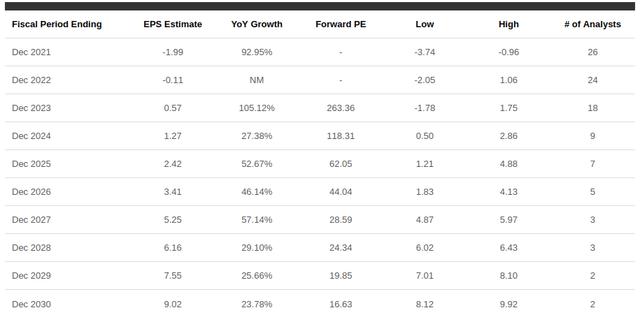

We used the earnings estimates from Seeking Alpha to build a discounted cash flow model for each. We start with Airbnb where we use more than ten years of analyst estimates, and then we assume an above GDP long-term growth rate of 5%. For the discount rate we use 10% since that is the minimum return we would be willing to accept as investors in the company.

Source: Seeking Alpha

| Fiscal Period Ending | EPS Estimate | # Analysts |

| Dec 2021 | -$1.99 | 26 |

| Dec 2022 | -$0.11 | 24 |

| Dec 2023 | $0.57 | 18 |

| Dec 2024 | $1.27 | 9 |

| Dec 2025 | $2.42 | 7 |

| Dec 2026 | $3.41 | 5 |

| Dec 2027 | $5.25 | 3 |

| Dec 2028 | $6.16 | 3 |

| Dec 2029 | $7.55 | 2 |

| Dec 2030 | $9.02 | 2 |

| Terminal value | $180.40 | 5% growth per year |

| DCF value per share | $86.02 | 10% discount rate |

The DCF model result of $86 per share for Airbnb is significantly lower than its recent trading price of ~$150.

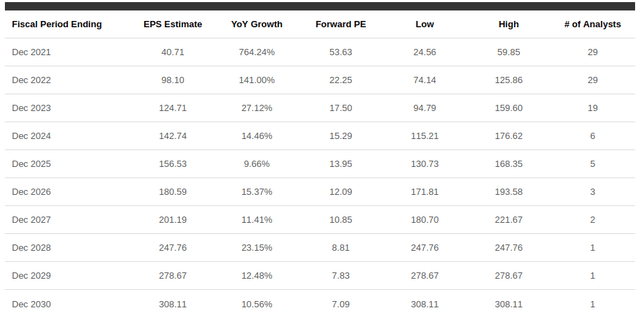

Repeating the exercise for Booking we obtain an estimated value per share of $3,422 compared to a recent trading price of $2,182. We therefore believe Booking Holdings is trading at a more than 33% discount to fair value, with a very nice margin of safety.

Source: Seeking Alpha

| Fiscal Period Ending | EPS Estimate | # Analysts |

| Dec 2021 | $40.71 | 29 |

| Dec 2022 | $98.10 | 29 |

| Dec 2023 | $124.71 | 19 |

| Dec 2024 | $142.74 | 6 |

| Dec 2025 | $156.53 | 5 |

| Dec 2026 | $180.59 | 3 |

| Dec 2027 | $201.19 | 2 |

| Dec 2028 | $247.76 | 1 |

| Dec 2029 | $278.76 | 1 |

| Dec 2030 | $308.11 | 1 |

| Terminal value | $6,162.20 | 5% growth per year |

| DCF value per share | $3,422.16 | 10% discount rate |

Conclusion

Airbnb and Booking Holdings are both high-quality platform businesses that will likely benefit from the increase in online travel bookings. However, at present time, we think Booking Holdings is the better option thanks to its international strategy, focus on hotels, and more than anything a much more reasonable valuation.