Summary

- Nvidia now sports a PE ratio of 90+, and the market is absolutely in love with its growth story. But will the growth story continue?

- In this article, we show that gaming growth is inflated artificially by high GPU AIB prices, which are not sustainable.

- Intel is about to launch its own discrete GPUs in Q1, and Ethereum is expected to go Proof-of-Stake in H1. These two are major headwinds to the Nvidia gravy train.

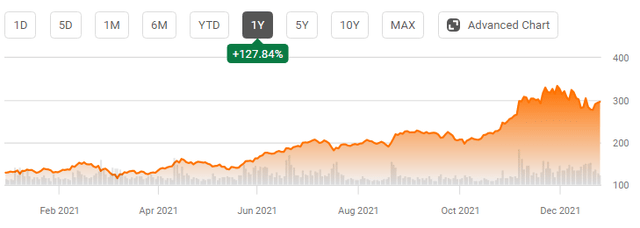

Nvidia (NVDA) has been an investor darling and had a spectacular runup year to date with the stock appreciating over 125%.

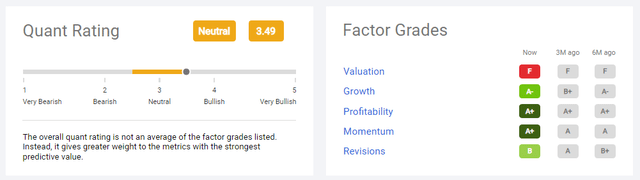

Despite having an "F" on valuation, the quant rating on the stock continues to be bullish (image below)

There is no shortage of boosters for the stock. Wall Street analysts are super bullish with only two of 42 surveyed analysts being bearish.

Is it a good thing to be bullish about a stock with an "F" rating on valuation? It depends. It depends on the drivers behind the valuation drivers and it depends on the drivers for future growth.

Nvidia Stock Recent Performance

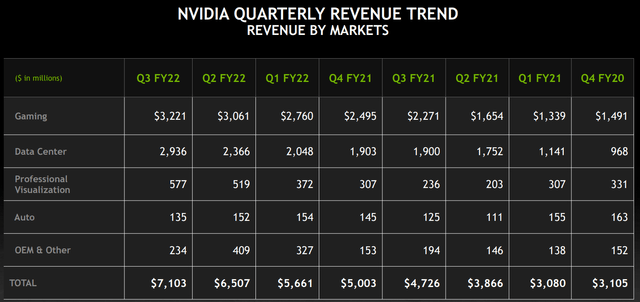

Let us take a look at Nvidia's recent growth and profitability drivers. As can be seen from the image below, despite the strong data center narrative, the Company's top revenue generator continues to be the "gaming" segment. To be sure, data center is growing more rapidly than "gaming" and will likely surpass gaming revenues in CY2022, but the impact of gaming on the recent earnings beat should be looked at carefully.

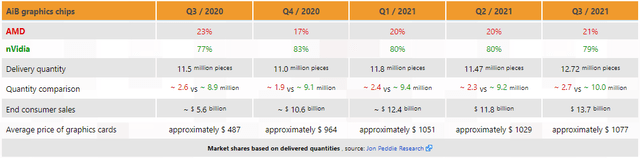

While these breakdowns are useful, Nvidia does two things that make interpreting the sustainability of these results difficult. The first one is that Nvidia underplays the impact of crypto-related buying in the gaming segment when multiple data points strongly indicate that it is crypto that is driving the gaming business. The second one is that Nvidia does not disclose the ASPs in the gaming business. A look at the table above shows that the gaming business grew from $1.9B in Q3 FY21 to $2.936B in Q3 FY22. At first, that comes across as a spectacular 55% growth year-over-year. But did the "gaming" business really grow that rapidly? Are there 55% more gaming card purchases? Given the lack of information from Nvidia, it is difficult to tell what the unit growth numbers look like. Fortunately, we can get a decent estimate by looking at retail prices of GPUs and from market research data. There are multiple data points out there that indicate that GPU ASPs are sky high now and cards are selling at prices never seen before.

For example, John Peddie Research, the source of the GPU data for the image below, shows that Add-In-Card GPU ASPs jumped from $487 in Q3 CY20 to $1077 in Q3 CY21. That is an increase of over 100% in ASPs at the board level. Note that the market research uses calendar years whereas Nvidia numbers are fiscal years. So, there is a slight offset, but the numbers are close enough. Note also that Nvidia reports a blend of chip and add-in-board sales whereas JPR quotes only AIB ASP. Because of the crypto demand, the AIB prices have shot up considerably, but chip prices may not have shot up as much. JPR also gives an estimate of the unit demand which they estimate went up from about 11.5Mu to 12.72Mu. That is only about a 10% growth in units. Working backward, we can see that the lion's share of Nvidia gaming growth came in ASP increases and not in unit growth.

Nvidia can achieve the big ASP gains by three methods - a) by increasing the prices of its chips, b) by selling AIBs at high ASPs directly to end customers, and c) by increasingly pushing the market toward higher-end solutions such as the 3070, 3080s, and 3090s. As most semiconductor investors know well, in a high leverage business like semiconductors, the incremental prices drop to the bottom line at a high rate. In other words, the current crypto-driven boom is artificially padding up revenue growth and is padding up profitability growth even more.

Impact of Crypto Miners on NVDA Stock

So, why is it that gamers are all of a sudden paying two times or higher prices for GPU cards? Is this sustainable? Firstly, there is absolutely no evidence that gamers are shelling out huge bucks to buy these cards. Gamer forums are full of complaints about gamers being unable to buy cards at reasonable prices - if at all. So, who is buying these cards?

The answer is simple. It is the crypto miners who are buying these cards and can justify paying the high prices due to high crypto prices - especially for Ethereum. A vast majority of the entire "gaming" supply appears to be getting sold to these miners as they see these cards as an investment.

But this crypto boom is likely to end soon as Ethereum is expected to go to Proof-of-Stake in H1 2022. Even if that gets delayed, as it has in the past, investors should be aware that Intel (INTC) is about to enter the gaming GPU market in Q1. Intel's entry should substantially change the supply-demand situation as there will now be three suppliers - Nvidia, Advanced Micro Devices (AMD), and Intel - serving the GPU market. Note that both AMD and Intel have low market share and are likely to derive proportionally small percentages of their revenues from the GPU segment and thus can afford to be very aggressive in going after market share. This dynamic is likely to be a severe headwind to Nvidia as the market leader has a lot more to lose than the challengers.

Conclusion: Is NVDA Stock a Long-Term Buy?

Nvidia's data center business is likely to do well in the near term, but the largest business segment taking big hits on revenues and profitability is likely to cause considerable harm to the growth story. Nvidia currently sports over 90x price-earnings multiple as the stock has become somewhat of a symbol for a growth story - although much of the recent growth has not been organic and instead a result of the Mellanox acquisition. In some ways, the GPU story is similar to how AMD went after Intel CPU market share and for the last several years Intel share price has stagnated as AMD gained share. Over time, Intel's ASPs have fallen, its margins and profitability have fallen, and the street is no longer in love with Intel. And Intel's stock price stagnation occurred even though Intel stock was not richly valued. Nvidia stock price has a lot more to give in context. Considering the steep valuation multiple the stock sports, now is not a good time to be long this story.