Summary

- SoFi has been growing rapidly, as evidenced by the significant increase in the company's membership base, the total number of product offerings, and revenue.

- SoFi's valuations are in the middle of the pack among its peers, and this seems fair given that it is still loss-making notwithstanding its attractive revenue growth prospects.

- SoFi is a Hold, considering its future prospects in terms of revenue growth and profitability.

Elevator Pitch

I have a Hold or Neutral rating assigned to SoFi Technologies, Inc. (SOFI).

Based on Wall Street's revenue forecasts and the company's financial targets, SOFI is expected to be able to maintain robust top line expansion (i.e. annual revenue growth in the +30%-60% range) over the next few years, and I see cross-selling as the key driver supporting the company's future growth expectations.

SoFi Technologies' forward price-to-sales multiples in the high single-digit to low-teens range appear reasonable. On one hand, the company has the strongest revenue growth potential in its peer group. On the other hand, SOFI is expected to reach profitability by fiscal 2023, while its peers are already in the black.

In conclusion, I think thatSoFi'sstock is neither worth buying nor a strong Sell now, which translates into a Neutral investment rating for the name.

Company Description

On its investors' FAQs webpage, SoFi Technologies, Inc refers to itself as a company that "was founded in April 2011 out of Stanford GSB (Graduate School of Business) with the goal of pioneering MBA peer-to-peer student loan refinancing."

SOFI also began providing mortgages and personal loans in 2014 and 2015, respectively. In 2019, SoFi Technologies ventured into financial services with the introduction of SoFi Money ("cash management account") and SoFi Invest ("brokerage account"). In 2020, SoFi Technologies bought out Galileo Financial Technologies, which it called "a global payments platform" that "enables critical checking and savings account-like functionality via its powerful open APIs (Application Programming Interfaces)."

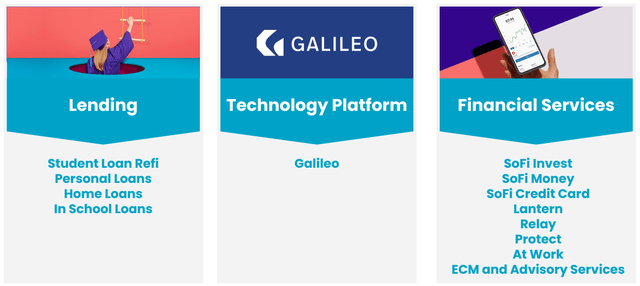

SOFI's Lending, Technology Platform and Financial Services business segments contributed 73%, 21%, and 6% of the company's revenue, respectively in the first half of 2021.

SOFI's Three Business Segments

Is SoFi Growing?

As of June 30, 2021, SoFi Technologies had approximately 2.6 million members and 3.7 million products (lending and financial services). In its Q2 2021 earnings report, SOFI defines members as "someone who has a lending relationship with us through origination or servicing, opened a financial services account, linked an external account to our platform, or signed up for our credit score monitoring service".

Based on my calculations, SOFI's membership base and product portfolio grew by two-year CAGRs of +84% and +105%, respectively up to the end of the second quarter of this year. SoFi Technologies' total number of accounts for its Technology Platform business segment also more than doubled from 36.0 million as of June 30, 2020 to 78.9 million as of June 30, 2021 following the company's acquisition of Galileo last year, as per its second-quarter earnings report.

SoFi Technologies' adjusted net revenue, which it calculates as "total net revenue, adjusted to exclude the fair value changes in servicing rights and residual interests classified as debt", increased by +74% YoY from $136.3 million in Q2 2020 to $237.2 million in Q2 2021. During the same period, SOFI reversed from an operating loss of -$23.8 million a year ago to register a positive non-GAAP adjusted EBITDA of +$11.2 million in the recent quarter.

It is clear that SoFi has been growing very fast.

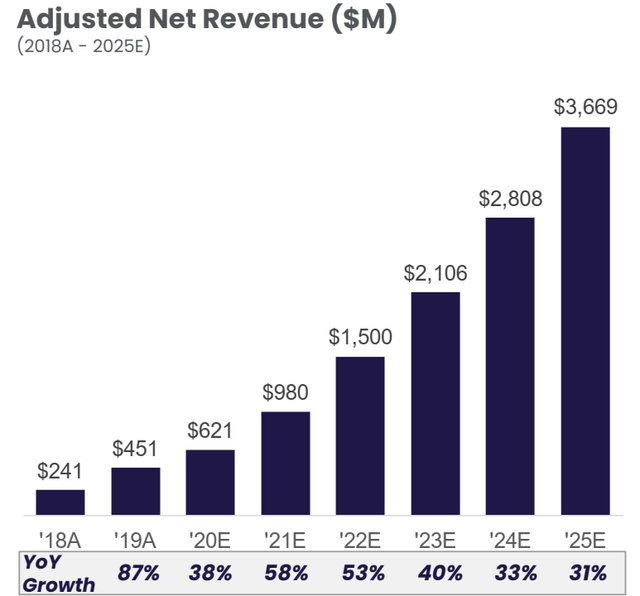

Looking ahead, both the company management and sell-side analysts expect SoFi Technologies' strong revenue growth momentum to be sustained in the next couple of years, as per the two charts presented below.

Company Management's Revenue Growth Expectations

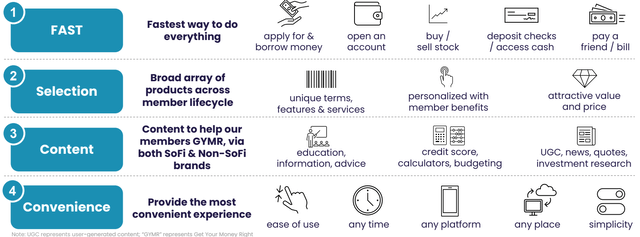

I attribute the positive growth outlook for SOFI to its key value proposition of making a wide range of financial products and services available on a single platform, which translates to a huge potential for cross-selling.

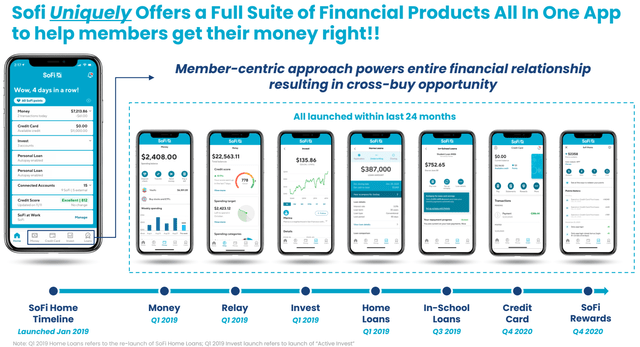

SoFi Technologies' Value Proposition

SoFi Technologies' Integrated Financial Solutions In A Single App

As evidence of SoFi Technologies' efforts to drive cross-selling in the past, SOFI's products per member (calculated as total number of products divided by its membership base) increased from 1.14 in Q2 2019 to 1.43 in Q2 2021. At the company's Q2 2021 earnings call, SOFI also highlighted that a tripling of the "number of financial services products held by SoFi members" led to "a 1.7x increase in the number of products that were cross-bought in the quarter versus Q2 2020."

More significantly, SoFi has set a target for the Financial Services business segment to account for 32% of the company's total adjusted revenue in fiscal 2025, as compared with the segment's current single-digit revenue contribution. As SoFi Technologies continues to ramp up its current financial services offerings and introduce new products & services over time, the company should be able to realize its ambitious top line expansion targets.

Is SoFi Stock Overvalued?

SoFi's closing stock price as of June 1, 2021, the first day of its listing, was $22.65, and the company's shares later fell by -40% to an all-time trough of $13.65 during intra-day on trading on August 17, 2021. SOFI's share price subsequently recovered by 39% in the next two months to close at $18.92 as of October 13, 2021.

Considering the volatility in SoFi Technologies' share price in the four and half months following its listing, it is worth examining SOFI's valuations to see if the stock is either overvalued and undervalued.

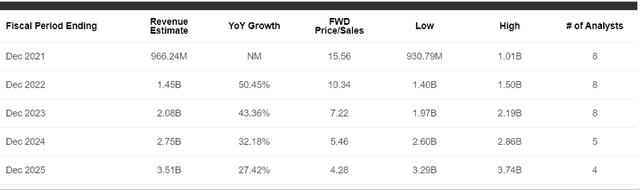

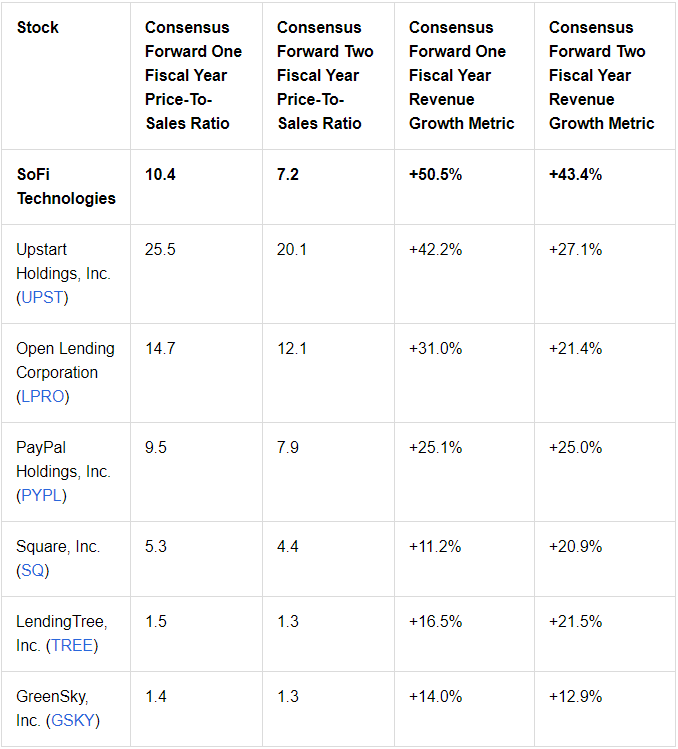

SoFi Technologies' Peer Valuation Comparison

As per the peer valuation comparison table above, the various stocks' forward price-to-sales ratios are largely correlated with their respective forecasted revenue growth rates (i.e. the better the revenue growth rates, the higher the valuation multiples), with the exception of SOFI.

SoFi Technologies' revenue growth expectations are the best among its peers, but its price-to-sales valuation is in the middle of the pack. The key issue here is profitability, as SOFI is the only loss-making company in the peer group. Both sell-side analysts and management expect SOFI to only become profitable in fiscal 2023. As such, it is reasonable that the market assigns a discount to SoFi Technologies, given that the company is still in the red.

I think that SOFI's shares are fairly valued. While the company's revenue growth prospects are excellent, it is not among the cheapest stocks in the sector and it is still unprofitable.

Is SOFI Stock A Buy, Sell Or Hold?

A Hold rating is what I will assign to SOFI's shares.

I am positive on the company's medium-term revenue outlook, especially in relation to its ability to cross-sell its products to support its future top line expansion. Notably, the revenue contribution of the Financial Services business segment is still very low, now in the single-digit percentage range, suggesting that there is significant room to market its existing offerings more aggressively and launch new products as well.

On the flip side, I am concerned that if there is a significant shift (e.g. higher interest rates) in the current accommodating credit environment going forward, SoFi Technologies might take a longer-than-expected time (i.e. later than FY 2023 as per management guidance and Wall Street's forecasts) to achieve profitability, as a result of potentially more expensive funding and higher-than-expected credit losses. This will imply that the valuation discount assigned to SOFI for its lack of profitability could possibly persist for some time.