Summary

- PLUG is a leading hydrogen fuel cell turnkey provider in North American and European markets.

- The company boasts advanced technology and strong growth momentum.

- We outline the company's path to growing from a $15 billion market cap to a $100 billion market cap over the next decade.

- That said, PLUG still faces significant risks to its thesis that investors should keep in mind.

Plug Power (PLUG) is a leading hydrogen fuel cell turnkey provider in North American and European markets. The company boasts advanced technology and strong growth momentum which should propel it to significant appreciation over the long term. In this article we outline the company's path to growing from a $15 billion market cap to a $100 billion market cap (nearly 7x returns) over the next decade.

#1. Addressable Market Potential

With the massive tailwinds for green energy and ESG investing at the moment, the hydrogen fuel cell market is likely to enjoy strong growth momentum for many years to come.

First and foremost, the Biden administration has executed an aggressive about-face from the previous administration in its disposition towards clean energy and fossil fuels. Between executive orders and rejoining the Paris Climate Accords, the U.S. Government is increasingly incentivizing green energy investment and consumption. The European Union and China are also increasingly headed in this direction.

Second, the ESG investing movement has taken off to where it now accounts for an astonishing one-third of total assets under management in the United States. Given that so much capital is attracted to environmentally friendly investments, companies across the board - including in the hydrocarbon sector - are increasingly adopting policies that appeal to the environmentally-conscious investor.

Third, the disruption and transformation of the automotive industry to reduce emissions is driving strong demand for new fuel technologies.

Finally - largely due to the heavy investment and market demand - green technologies such as hydrogen fuel cells are seeing costs decline dramatically, making them increasingly competitive on the marketplace.

All of this should lead to continued strong growth in the sector. In fact, U.S. Hydrogen demand is expected to be 17 million metric tons per year by 2030 and 63 million metric tons by 2050, which is pretty substantial growth from the 10 million metric tons consumed in the U.S. last year. Globally, the hydrogen generation industry is expected to reach $201 billion by 2025 and should continue to grow rapidly in the decades to follow similar to how it is expected to grow in the U.S.

#2. Market Share Drivers

We believe that PLUG has a strong chance at capturing a sizable portion of this massive addressable market for the following reasons.

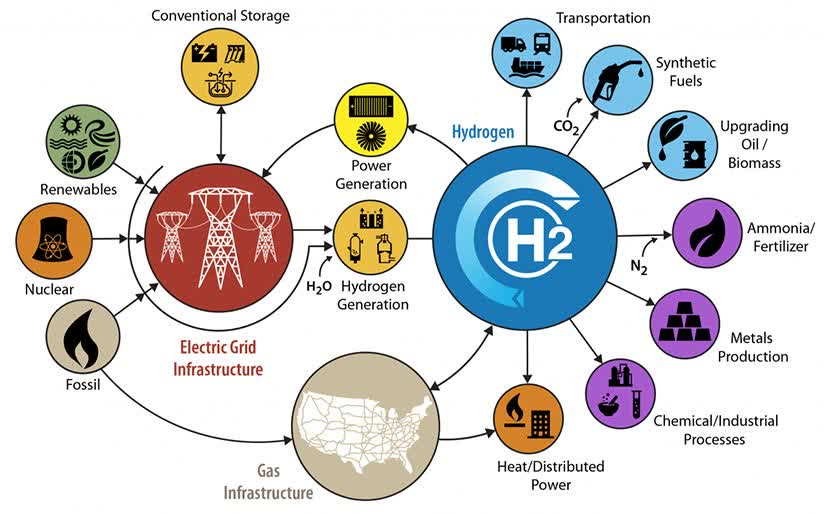

First and foremost, it has advanced technology and early mover advantages in the space. It owns numerous hydrogen energy systems including proton exchange membrane fuel cells, hybrid batteries, hydrogen storage, hydrogen dispensing, and fuel processing. Its flagship product is the electric vehicle focused GenDrive system that is complemented by their GenFuel and GenCare systems.

Second of all, it has a foothold in both North America and Europe which means that it has significantly more growth potential than if it was solely focused on a single continent. In fact, North America and Europe are likely to be the leaders in Hydrogen adaptation for the foreseeable future, so PLUG is well-positioned to capture a significant portion of the global market share.

Third, PLUG has strong growth momentum right now and is winning business from some of the biggest companies in the world, including Amazon (AMZN), Walmart (WMT), Home Depot (HD), and General Motors (GM) either currently using their products or expected to become customers in the near future. As a result, we expect the 76% year-over-year revenue growth in its most recent quarterly report (128% year-over-year growth in their fuel cell systems and related infrastructure segment) to be sustainable for the foreseeable future.

In fact,analysts expect revenue to grow by 57% in 2022, which should push the company to EBITDA profitability.

#3. Valuation

While PLUG certainly operates in a hot industry and has numerous drivers that should enable it to capture significant market share, the company is also not cheap as it is currently running a loss.

On the other hand, its EV/revenue figure is not outlandish given their growth runway as PLUG currently trades at 29.8x expected 2021 sales and 21x expected 2022 sales.

In fact, with a product gross margin of 38% that expanded by a whopping 600 basis points in PLUG's most recent earnings release, its profitability potential is significant. Overall, PLUG's gross margin is expected to be a fairly weak 9.71% in 2021, but is expected to nearly double in 2022 to 18.93%. This is also a massive increase from 2017 when the gross margin was a mere 1.2%. The EBITDA margin is also expected to be a somewhat respectable 10.7% in 2022 as well.

If PLUG can continue to leverage its strong technology and massive expected economies of scale in the coming years, we think it is reasonable for it to push gross margins to 30% and net margins to 20% by 2032. Meanwhile, if it can capture even just 3% of global hydrogen market share by 2032 and the global market reaches roughly $390 billion by then (it is expected to exceed $200 billion by 2025 and will likely be growing by around 10% per year at least for the foreseeable future), PLUG should be generating $11.7 billion in revenues by 2032. That would assume a 31.9% revenue CAGR between 2022 and 2032, which we also believe is quite reasonable given its aforementioned growth momentum and competitive strengths.

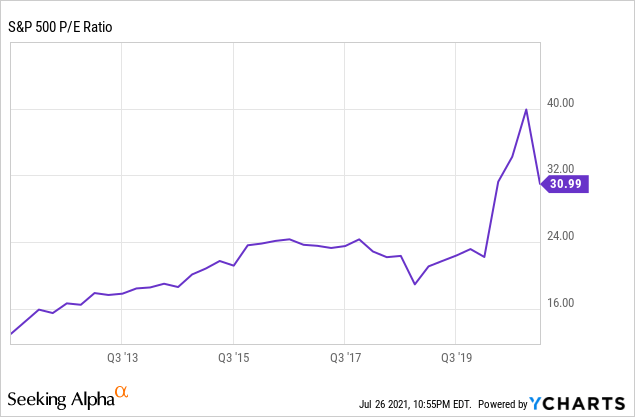

At a 20% net margin, that would put its net earnings at over $2.3 billion in 2032, which would require a 42.7x price to earnings multiple to warrant a $100 billion market cap. Is this a reasonable multiple? It depends a lot on interest rates, but, given that the current S&P 500 (SPY) multiple is ~31x and PLUG's growth rate and growth runway will likely still be vastly superior to where the S&P 500's is today, it certainly does not seem too far-fetched to us.

#4. Risks

If this model pans out how we think it could, PLUG is a very attractive buy on the latest pullback.

Of course, it assumes that PLUG will be able to overcome several risks, so investors should keep in mind that it remains a very speculative investment at this point.

First and foremost, it will demand that PLUG can maintain highly competitive technology in a space that is almost certain to grow increasingly competitive in the years to come.

Additionally, PLUG will need to balance investing in recruiting the best talent in the industry to sustain and increase its technological edge with investing in effective marketing while also avoiding diluting shareholders or running up a big debt burden. Given that it is not yet free cash flow positive, this could prove challenging in the short term. That said, their nearly $4.8 billion in cash and cash equivalents on hand should enable it to reach free cash flow positivity without stressing its balance sheet.

Third, hydrogen power has not been without its critics over the years, most notably Tesla's (TSLA) founder and CEO Elon Musk. The wildly popular and visionary entrepreneur argued that using hydrogen to store energy can never be as efficient as storing electricity in a battery. In fact, he has gone so far as to say that using hydrogen fuel cells (which he calls "fool cells") to power vehicles is "mind-bogglingly stupid." Obviously many individuals and corporations disagree with Musk's assessment and he has a clear incentive to try to discredit the technology, but this should still be viewed as a significant risk to keep an eye on. If hydrogen were to fall out of favor, it would significantly reduce the upside for PLUG and could even lead to permanent impairments from current levels if severe enough.

Investor Takeaway

PLUG is a competitively positioned company in a rapidly-growing industry. Not only that, but the industry's growth runway looks promising for many decades to come. With advanced technology, early mover advantages, and a foothold on the two most fertile continents for Hydrogen technology, PLUG should be able to generate strong revenue growth for a long time to come.

Given our assumptions outlined in this article, we think that PLUG could very possibly achieve a $100 billion market cap in about a decade. This would represent a 667% total return (20.9% CAGR) over that span assuming no further share dilution.

That said, PLUG is also far from a conservative sleep well at night stock and investors should keep in mind that its current valuation assumes significant future growth and an ability to scale into profitability. It also assumes that it will retain a strong technological moat which will enable it to increase gross margins over time.

Overall, we rate PLUG a speculative buy at this point.