Novavax and Beyond Meat are among the companies scheduled to report earnings Thursday.

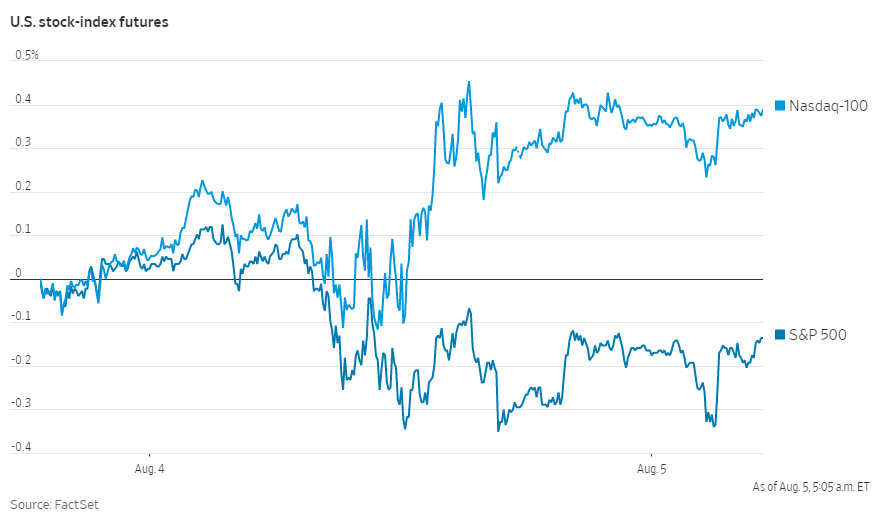

Futures tied to the S&P 500 ticked up less than 0.2%, pointing to modest gains at the opening bell after thebroad market index closed down 0.5%on Wednesday. Nasdaq-100 futures also gained 0.1% and Dow Jones Industrial Average futures were relatively flat.

The major stock indexes have wobbled in recent days amid concerns that the rebound may be slowing and the Delta variant of Covid-19 is leading to asurge in cases. Fresh data Wednesday showed that the private sector added half as many jobs in July as economists expected. Despite the volatility, the S&P 500 is still hovering near its all-time high, boosted by strong quarterly results fromthe biggest businesses.

“We’re pretty positive, we think that the earnings data is very strong,” said Caroline Simmons, U.K. chief investment officer at UBS Global Wealth Management. Equity markets can continue to climb by 5% to 10% over the next year, she said.

The continued signs of weakness in the labor market also suggests that the Federal Reserve will hold off on scaling back itseasy money policiesfor now, Ms. Simmons added.

“Unemployment is higher than it was pre-pandemic, and central banks feel there is still excess capacity in the labor market,” Ms. Simmons said. “When it comes to it, we believe that monetary tightening will be relatively gradual, well flagged, and actually, equities will probably be able to absorb it.”

In bond markets, the yield on the benchmark 10-year Treasury note edged up to 1.187% from 1.183% on Wednesday.

Pharmaceutical company Moderna, food giant Kellogg and media conglomerateViacomCBSare slated to report their results ahead of the opening bell.Novavax,NVAX18.69%Beyond MeatBYND0.20%andAmerican International Groupare scheduled to post earnings after markets close.

Data on the U.S. trade balance for June is due at 8:30 a.m. ET. Economists expect the trade deficit to have widened after preliminary figures showed record goods imports with Americans buying more from overseas.

Data on jobless claims, seen as a proxy for layoffs, are set to be released at 8:30 a.m. ET. The figures released last week showeda moderate decline in claims, but they remain in a range that is nearly double the pre-pandemic average.

Overseas, the pan-continental Stoxx Europe 600 added 0.3%. The Bank of England’s latest monetary policy decision, economic forecasts and minutes are due at 7 a.m. ET. Investors expect policies to remain on hold and are awaiting signals on when the central bank could begin to pull back on stimulus measures.

“We’ll be looking for signs, anything from the BOE that adds to the hawkishness in the developed-market central bank narrative,” said Arun Sai, multiasset strategist at Pictet Asset Management. Earlier this week, the Reserve Bank of Australia said it would go ahead with its plan totaper its bond-buying programdespite an uptick in Covid-19 cases.

Among European equities, Germany’sSiemensrose close to 5% after raising its full-year outlook and reporting revenue that beat analysts’ expectations. Bayer slipped over 5% after it posted a net loss and said earnings continued to be affected by litigation costs for its Roundup weedkiller.

The Shanghai Composite Index slid 0.3% by the close of trading, and Hong Kong’s Hang Seng Index declined 0.8%. Chinese stocks slipped due to concerns about restrictions on movement amid new outbreaks of Covid-19, according to analysts at Commerzbank.

Japan’s Nikkei 225 advanced 0.5% by the end of the trading session in Tokyo.