Summary

- KO looks like it wants to break out.

- But I'm skeptical right now given a number of fundamental headwinds.

- With the valuation stretched, avoid KO.

Beverage companies are not always the most glamorous stocks to buy, but over time, they tend to do well. Steady demand from consumers in both at-home and away-from-home channels generally fuels not only reliable growth but some measure of recession resistance as well.

Bubbly beverage OG Coca-Cola(KO) is just such a stock that has paid rising dividends longer than most of us have been on this earth, so it fits nicely into the “recession resistant” and “steady growth” categories to be sure.

But does that make the stock a buy today? In a world of elevated valuations and low yields, Coca-Cola today seems to fit the bill on both of those accounts as well, and given this, I’m not certain it’s a good use of your capital.

We’ll start as we always do with a look at the chart to get a glimpse of where we are today. First, the stock broke out over its prior consolidation earlier this year after being pummeled down to $47 back in January. The rally took the stock up about ten bucks in a virtually straight line, which is a huge move for a stock like this. That rally was quite strong, but proved to be unsustainable, as evidenced by the momentum indicators.

The PPO made its high in April, months before the share price did, and even in the most recent stage of the rally, the PPO was actually declining fairly sharply, indicating that there was a meaningful negative divergence. That’s generally what the end of a rally looks like; the bulls are still fighting but not nearly as hard.

However, the PPO recently successfully tested centerline support (the blue oval) and looks like it wants to bounce. I’ve noted the trendline of the current rally, which is just about ready to bump heads with the prior high at $57. We’re going to get a showdown, and the stock will either break trend and decline, or break out and move higher.

It looks to me like the stock wants to break out, so that’s the way I’m leaning. However, I’m not certain enough to bet on that because the momentum divergences are concerning to me. But if Ihadto pick one, I’d say a breakout is slightly more likely.

Fundamental considerations

Now, with a stock like Coca-Cola, there are lots of other considerations besides just the chart. We know that away-from-home volumes dried up massively for the company during the pandemic, as things like restaurants, sports stadiums, and other places where you would go out and buy a zesty beverage were shut temporarily. That segment is still gradually recovering for Coca-Cola, and it has had to compensate with its other growth avenues that are focused at-home, such as coffee, tea, and its core sparkling beverages in smaller packages, for instance.

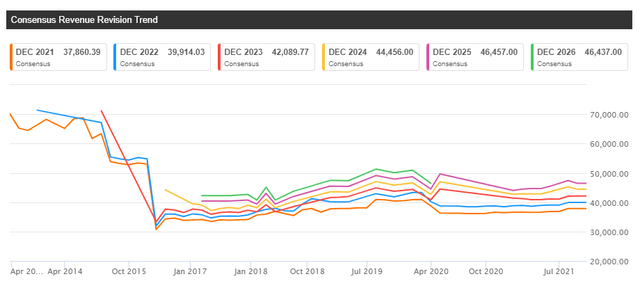

That has shown up in revenue estimates, which we can see below.

Ignore the massive declines in the early part of this chart; that was due to the company’s now-completed bottling refranchising effort. We can focus on the past couple of years, and see that the company’s revenue estimates are still struggling relative to expectations. As great of a company as Coca-Cola is, you cannot escape the fact that it has a tendency to struggle with revenue estimates. That creates the obvious problem of a lower top line, but also because that impacts things like margins.

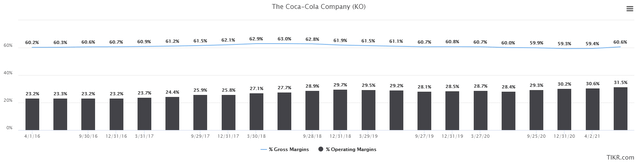

The goal of the company’s refranchising effort was to boost margins by divesting low-margin bottling revenue, and it has certainly worked. But that tailwind is no more as those gains have been lapped, and Coca-Cola will now need to find actual margin improvements through sales mix, volumes, or any other means possible.

As we can see, it is working to some extent. Operating margins are in excess of 31% on a trailing-twelve-month basis, which is great. But that’s only marginally higher than it was before the bottling refranchising effort was complete. I’ll say that the company has been able to find profitability improvements in recent quarters, some of which were due to corporate layoffs to reduce headcount where it was apparently bloated. But for investors wanting to own this stock, operating margins are critical, particularly because revenue growth has been so weak.

I’m not certain where revenue growth will come from for Coca-Cola apart from the usual suspects of bottled water, coffee, tea, and other non-sparkling beverages. The trick is that sparkling isn’t growing for the most part but continues to make a huge proportion of revenue. That makes overall growth tricky, even if one or more segments are flying. Diversification works both ways, and in Coca-Cola’s case, it has been a years-long struggle with consumers shifting preferences to non-sparkling beverages.

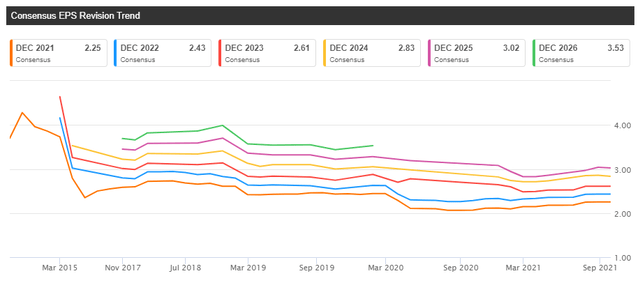

Now, let’s take a look at earnings.

We can see the same sort of behavior that we saw with revenue, and that is not a compliment. EPS estimates have nearly continuously fallen, and while there’s been an uptick in recent months, it is peanuts compared to the prior declines.

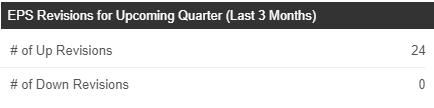

We can see that all 24 revisions that have been made in the past three months have been higher, and that’s fantastic. However, in this case, keep in mind it was because the company is simply retracing lost ground; these are not estimates that are carving out new highs by any stretch of the imagination. You must temper your bullishness as a result, and keep in mind that the stock is knocking on the door of new highs while EPS estimates languish; more on that in a bit.

Other considerations

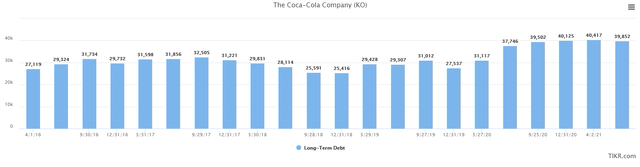

Apart from revenue concerns, I have others with Coca-Cola as well. Below I’ve plotted long-term debt over the past several years to illustrate one meaningful concern I have.

We’re now up to about $40 billion in long-term debt, which is much higher than it was even before the refranchising effort was kicked off. Debt has been steady for the past handful of quarters, but this is a lot of debt for any company, and that includes one of the world’s premier consumer brands. Coca-Cola has the credit to borrow almost whatever it wants, so it isn’t like we’re looking at default potential. But what it does mean is that the company is on the hook for an ever-rising amount of interest expense, which is also taking a bigger share of operating income.

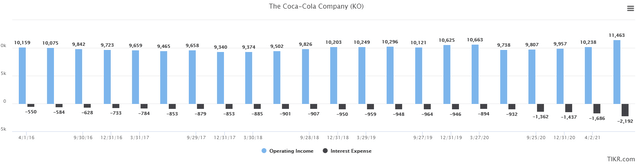

Below, we have operating income and interest expense on a trailing-twelve-month basis to illustrate what I’m on about.

Operating income has been remarkably flat over the years given the amount of change the company has undergone. The most recent quarter finally saw a new high in TTM operating income at $11.5 billion, but interest expense was also $2.2 billion. As a percentage of operating income, interest expense is now nearly 20%. So while the company has been busy trying to boost margins and scrape together some revenue increases, it continues to pay more to creditors.

This, in turn, reduces EPS because more and more operating income is going to creditors rather than shareholders. At a time when the company is struggling to grow EPS, this is yet another headwind it doesn’t need.

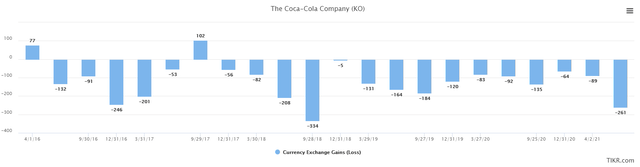

There’s another consideration for Coca-Cola given its mostly non-US revenue base, and that is forex conversion.

Forex conversion has been a headwind given US dollar strength, and as long as the dollar is strong, the company will continue to have hundreds of millions of dollars of headwinds from forex conversion over time. This fluctuates a bunch given the unpredictable nature of forex crosses, but one thing is clear: Coca-Cola isn’t managing it well and it shows.

Final thoughts

Coca-Cola has some of the greatest consumer brands that have ever existed, and it is a terrific dividend stock. However, the points I’ve raised here make me wary of the stock as it tries to make new highs. I see the valuation as quite stretched, not only against historical norms but against the company’s ability to grow earnings given the points I’ve raised.

The stock is at ~24X forward earnings today, which is nearly its highest valuation ever. The stock was slightly more expensive at times in 2020 and 2021, but compared to historical valuations, I see the stock as overpriced. That doesn’t mean it cannot get more overpriced by any means, but I’d suggest caution at this stage.

As I mentioned, I think the path of least resistance short-term is probably higher, but I’m in no way interested in trying to trade it. There are numerous headwinds in place that make me doubt the rally, and the valuation is way too stretched for my liking. There are better consumer stocks to buy than Coca-Cola, and if you want the dividend, I think you wait for another larger selloff before pulling the trigger. Medium-term, I see the stock either pulling back to reflect the headwinds I’ve mentioned, or consolidating for a long time to allow EPS to catch up to the share price. Either way, there is no urgency to go out and buy today.