Investors buying stocks no matter what shouldn’t fool themselves that the future will deliver the chunky returns of the past decade.

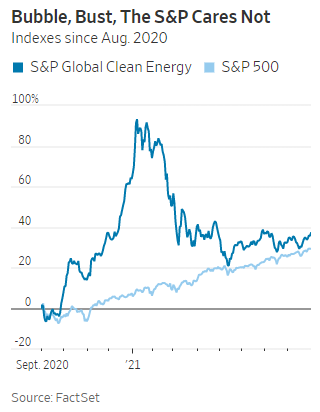

Some things that didn’t matter:a burst bubble in clean-energy stocks;a sharp rise in Treasury yields(to March);a big fall in Treasury yields(since March); China’s crackdown on moneymaking; the Federal Reserve’sshift toward tapering bond purchases; and the rise of the Delta variant.

On the optimistic side, it is great that the market has been pushed up by a variety of forces, not by wild excess in a single area. We need not worry that the bubble in clean energy will burst and bring down the market, because it has already burst without bringing down the market.

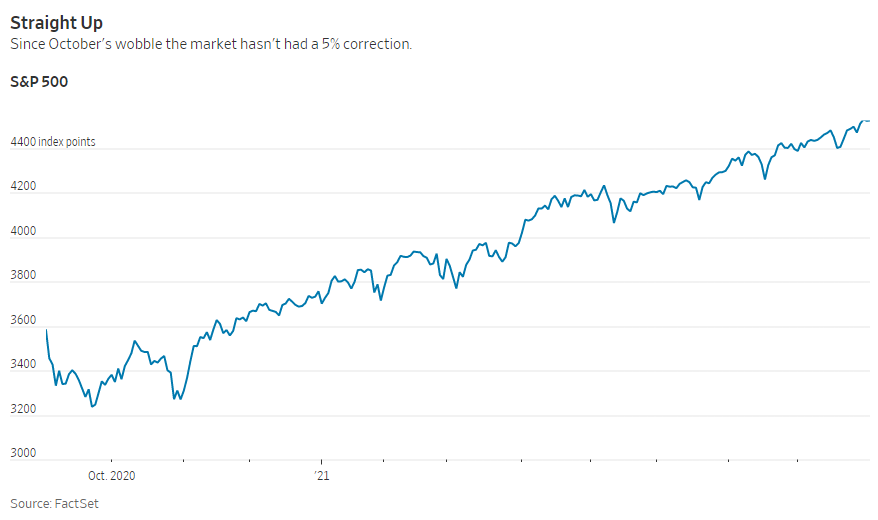

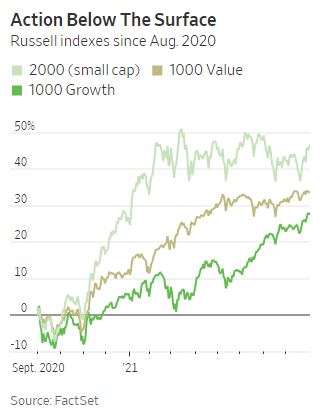

Throughout all this, the stock market has risen steadily,without a 5% fall since shortly before the election last year. Every time part of the market—technology stocks, cheap stocks, smaller stocks, oil stocks, strong-balance-sheet stocks—stops performing, something else steps in to rescue the broader index. The market seems invulnerable to bad news, and that is unusual. On the face of it, it is also scary, suggesting investors are complacent about danger.

It is far from unprecedented to go a long time without a correction, with 10 episodes since 1963 when the market lasted more than 200 trading days without a 5% drop. But they were different from the recent run. In every other case, the market was far calmer below the surface. This time, major events led to big swings between sectors, size and types of stock, but none disturbed its steady rise.

Similarly, the stimulus- and vaccine-driven willingness to take risk across every asset class faded from March onward, so we shouldn’t be too concerned about a switch in investor sentiment. Again, it has already happened.

The only explanation I have is the old one: “TINA”—There Is No Alternative to Stocks—because yields on alternatives such as bonds are so low. With more savings going into stocks than is cashed out or soaked up by IPOs, the price has to rise. It isn’t a satisfactory story, but it kind of works.

The problem with TINA is that the justification for stocks isn’t that they offer good returns in the future, but that they offer better returns than bonds. Bonds offer miserable returns—a guaranteed loss after inflation for 30 years on Treasury inflation-protected securities—so doing better than that isn’t saying much. If lower rewards came with lower risks, that would be fine, but at best the risks are as high as ever, perhaps much higher.

A simplistic way to quantify how much lower the rewards of stocks are likely to be is to use the earnings yield, the inverse of the forward price/earnings ratio. If companies match analyst profit forecasts, future returns should be about 4%—only slightly higher than was suggested by the measure at the height of the dot-com bubble in 2000. If corporate earnings miss forecasts, future returns could be substantially lower. If valuations fall too, returns are doubly hit, as they were after the dot-com bubble burst, when returns ended up negative for years.

Quantifying risks is much harder. Inflation risk is higher than before, and so are political (tax and regulation) and geopolitical (trade and supply chain) threats to stocks. The risk that analysts have horribly overestimated earnings or companies are massively overstating earnings is at least as high as usual. Central banks are sure to try to help if stocks plunge, but can’t use the traditional support of rate cuts. Alternative tools such as negative rates and buying a wider range of assets are available, but their risks are less well understood.

Getting a lower reward for the same or higher risk may still be acceptable, given how expensive the safer alternatives are. But investors buying stocks no matter what shouldn’t fool themselves that the future will deliver the 6.5% or so above inflation of the past century, let alone the 12% above inflation of the past decade.

The awful choice investors have is to join the monkeys in pretending all is well, or accept the terrible returns of safe assets.