Summary

- SentinelOne went public in June of 2021 and has been on somewhat of a roller coaster since.

- The company has an enormous TAM, incredible growth, and strong future prospects.

- Despite these positives, there remain concerns that may not justify the current valuation.

- There are likely much better entry points coming.

SentinelOne Enters The Cybersecurity Fray

Cybersecurity is one of the most critical challenges of our time. The total costs from malware, ransomware, data breaches, and other threats account for billions upon billions of dollars worldwide - and growing rapidly. These threats affect organizations of all types. We have seen data breaches at Big Tech companies, hacks of United States government agencies, a brazen attack on a vaccine registry in Italy, and everything in between. The work-from-home (WFH) acceleration has only expanded the market for endpoint security that much faster.

SentinelOne(NYSE:S) is a leader in endpoint protection services and a rapidly growing company to watch.

SentinelOne Has Amazing Potential

As mentioned, SentinelOne is a leader in endpoint protection according to Gartner in 2021. This is a critically important function.

Forbes puts the total addressable market for SentinelOne at over $40B by 2024. It is important to note the stiff competition among the leaders. CrowdStrike(NASDAQ:CRWD) is clearly still the Gartner favorite among SentinelOne' s direct competition.

The growth metrics at SentinelOne are likely unmatched among peers. Year-over-year (YOY) the company increased annual recurring revenues (ARR) over 127% based on July 31, 2021 earnings. The total customer count increased over 75% in this period. Even better, large customers (those who provide over $100,000 in ARR) grew 140% over this time.

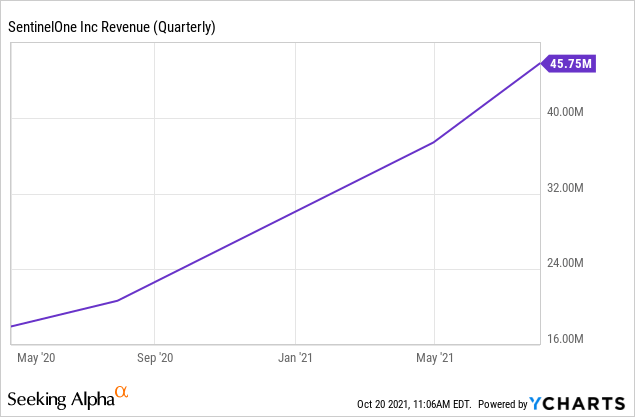

Shown above, quarterly revenue for the three months ended July 31, 2021 was $45.75M, up from $37.4M for the three months ended April 30, 2021. This is a quarterly growth of over 22%. The company's growth is expected to continue with another 70% of annual growth in fiscal 2023.

Author's note: S runs on a January 31 fiscal year end, so fiscal 2023 is the year ending January 31, 2023.

This is all excellent news. It is important not to forget the laws of small numbers and percentages. For instance, while SentinelOne is adding more revenue on a percentage basis, CrowdStrike is adding much more on an absolute basis. As SentinelOne scales the percentages will normalize. The same is true of customers. While SentinelOne grew the customer base 75% from July 31, 2020 to July 31, 2021, this amounted to about 2,300 customers added. Over the same period CrowdStrike added 5,850 customers, an increase of 80%.

The IPO cash windfall should allow management to spend whatever is needed on increasing the customer base and ARR. The company us sitting on $1.68B in cash and equivalents with only a small amount of current liabilities, relatively. Potential acquisitions are also a possibility.

Some Metrics Are Concerning

SentinelOne does have areas for which improvement is needed in coming quarters if they are to become a stock for which I am a buyer.

First, the ARR per customer is much lower than many peers. Based on the ARR reported of $198M, and total customer count of 5,400, SentinelOne is bringing in just $36,667 in ARR per customer. CrowdStrike, by contrast, brings in nearly $100,000 in ARR per customer. For those interested, I have written extensively about CRWD's metricshere.

Determining SentinelOne's customer acquisition cost is somewhat difficult based on the limited reporting available. However, it is likely, based on the six months ended July 31, 2021, that S has spent $130-$150M on sales and marketing in the last four quarters. This would give them a customer acquisition cost of between $56,000 and $64,000 for that period. Given the average ARR, the payback period is 18-20 months. This is far outside of the optimal 5-10 month payback period for SaaS companies. The SaaS Magic Number for the last four quarters would also be in the range of 0.73 - 0.85. The optimal Magic Number is greater than 0.75.

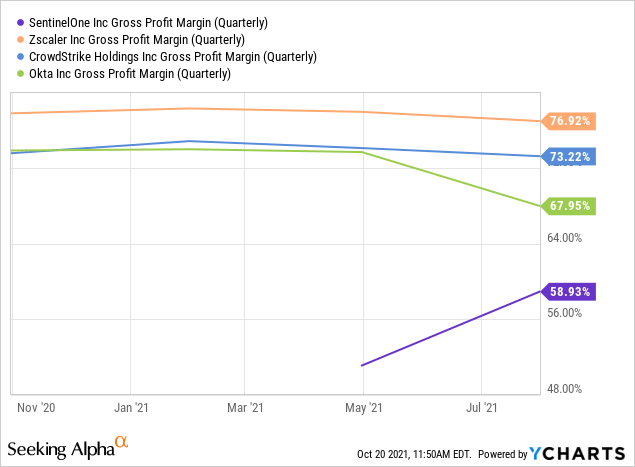

Gross margin is another area in which SentinelOne struggles compared to peers. Zscaler(NASDAQ:ZS),which I have covered recently here,is posting gross margins nearing 80% in some quarters, while S is struggling to maintain 60%.

As shown above, SentinelOne has some work to do in this area. Gross margin is often an indicator of a SaaS company's ability to scale to profitability successfully.

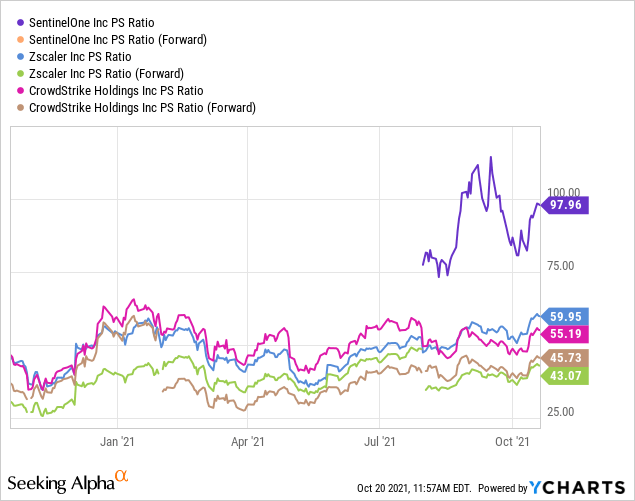

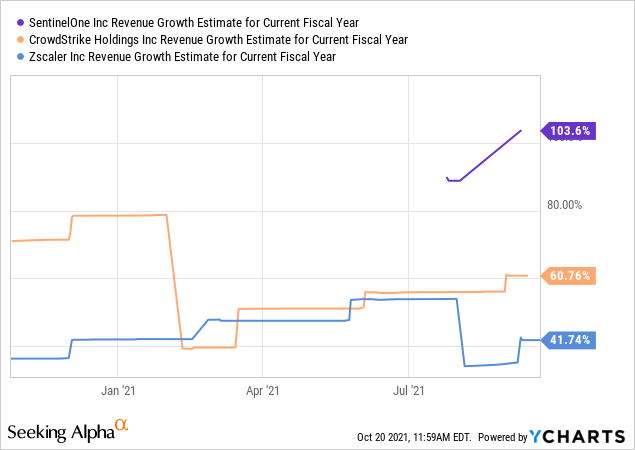

Despite these concerning metrics, SentinelOne stock trades at an incredibly high price-to-sales (PS) ratio. The forward PS ratio is 87.44x according to Seeking Alpha. This is far higher than peers who have better overall SaaS metrics. Given, none of these companies are growing at the percentages of SentinelOne, shown below.

Summary on SentinelOne

Wall Street is generally bullish on S stock with a Bullish rating according to Seeking Alpha's Wall St. Analysts Rating Summary. 10 analysts come in at Bullish or Very Bullish and two have neutral ratings. The average analyst price target is just over $75 or about 17% over current prices.

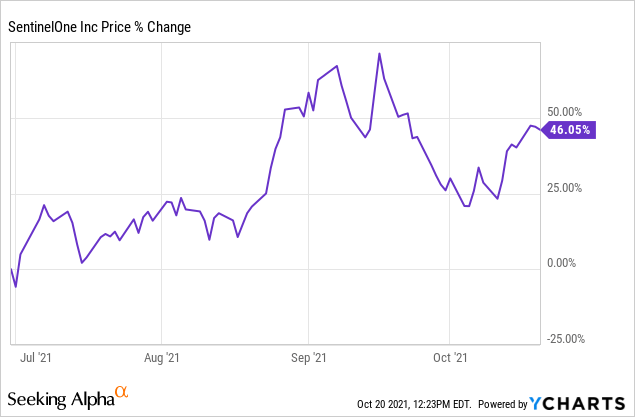

As shown below, the stock has enjoyed a bullish ride since its IPO, rising 46%. It is currently 15% off September 2021 highs.

In my opinion, SentinelOne is a stock to watch and a company with massive potential. At this point, however, I need to see quarterly improvements in metrics, or a price correction, before initiating a position.