Summary

- Zoom's revenue growth is entering a post-pandemic slump.

- Growth in key customer groups is also slowing down.

- Expenses are rising.

- Zoom is still overvalued.

Zoom Video Communications (ZM) is at risk of generating negative returns for shareholders as a period of pandemic gains is coming to an end. Zoom's third-quarter showed that the threat of a revenue slowdown is real and shares of Zoom are still overvalued!

A new normal: Slower revenue growth

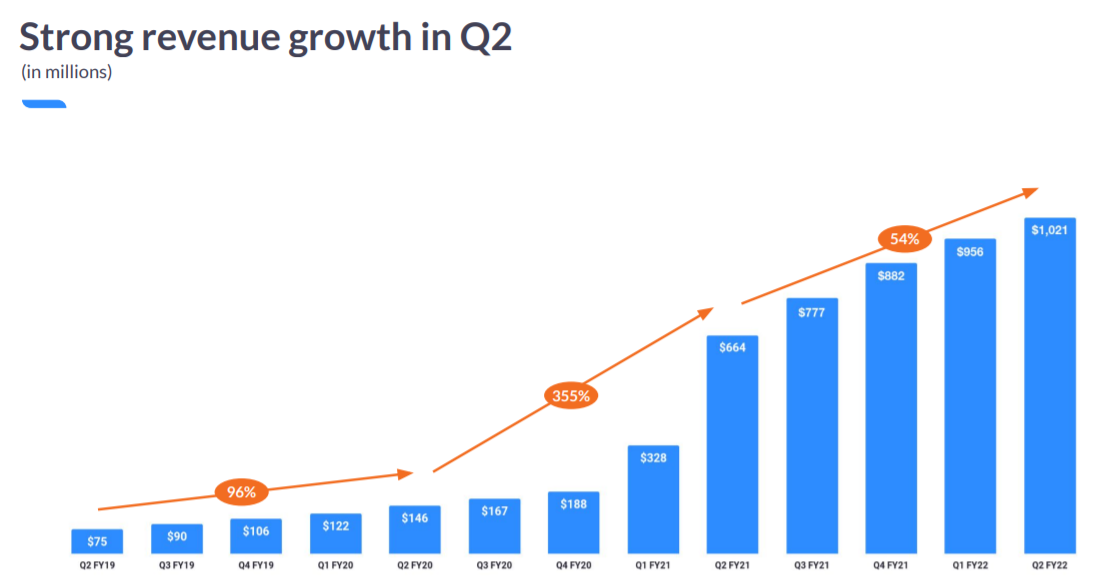

Zoom benefited from the COVID-19 pandemic like few companies did. The video chat company experienced an unprecedented revenue surge last year because businesses shut their doors and employees were forced to work from homes. The rise in remote working accelerated the digital transformation trend and Zoom played a key role for a lot of companies to communicate with their employees. Because of the pandemic, Zoom's revenues doubled between Q1'20 and Q2'20… and the business experienced strengthening demand for its video conferencing services in the quarters that followed. In the second-quarter, Zoom's communications platform generated more than $1.0B in revenues for the first time in the firm's history. Revenue growth in the second-quarter, year over year, was 54%.

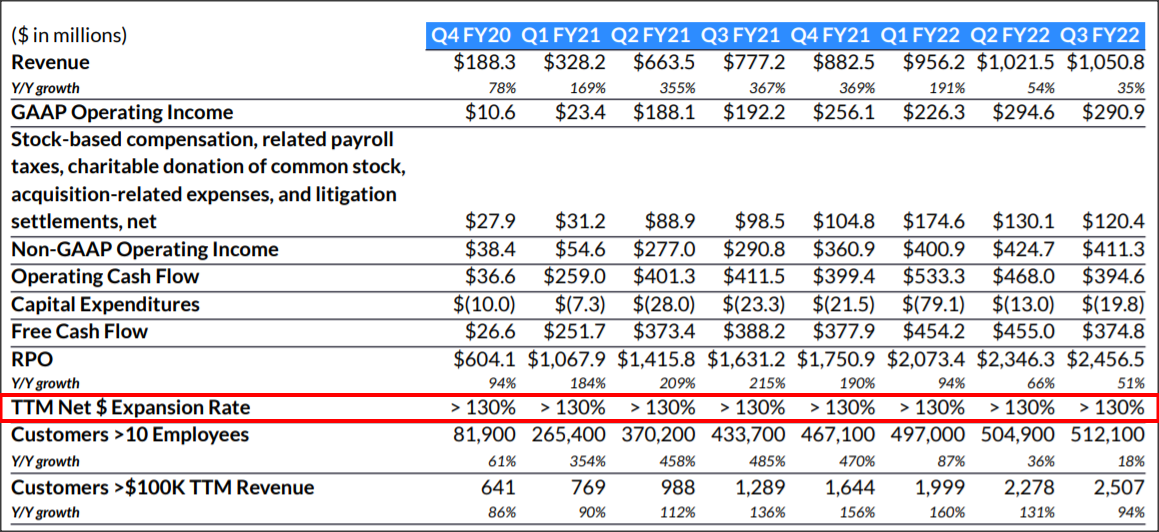

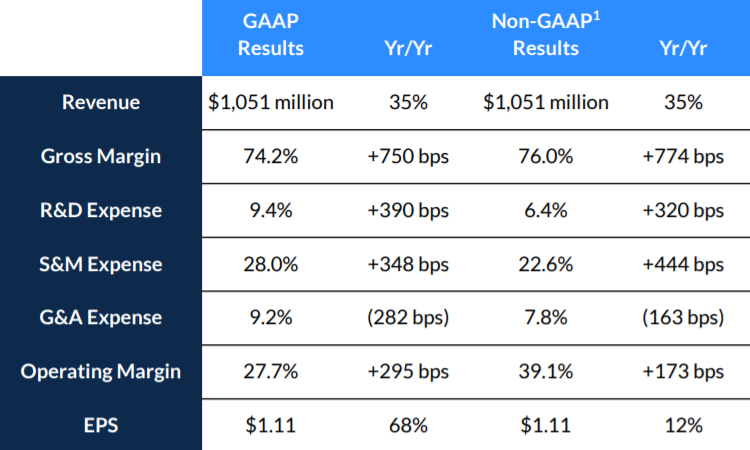

Since the second-quarter, however, sales growth has been slowing down. Revenues in the third-quarter were $1.05B, showing a revenue growth rate of only 35% year over year. Zoom, spoiled with accelerating revenue growth rates during the pandemic, is now looking at a material deceleration of growth… and it already has an impact on Zoom's perception as a growth stock. Shares of Zoom cratered 14.7% yesterday, after presentation of the third-quarter earnings card. The one year price return is (52)%...

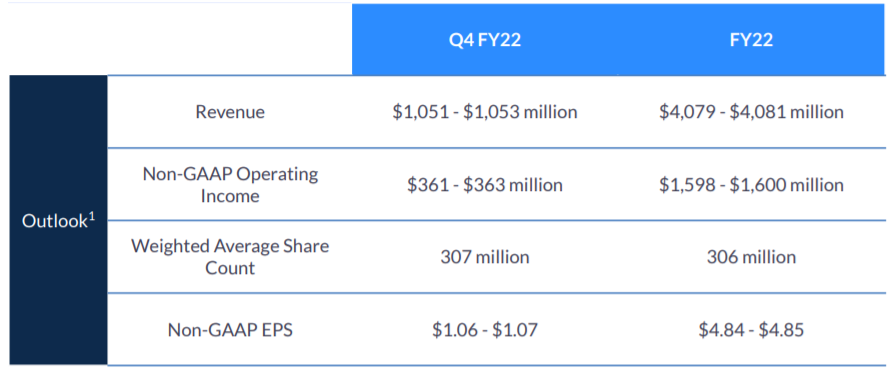

What isn't helping shares of Zoom is that the outlook for the fourth-quarter indicates a continual slowdown in revenue growth. Revenues are barely going to grow quarter over quarter in Q4'22, although they will grow 19% year over year to around $1.052B. The outlook for FY 2022 strongly indicates that Zoom's revenue growth rates have peaked… which creates a justification for a material repricing of Zoom's commercial growth prospects.

Zoom's customers- typically large companies with more than 10 employees or $100 thousand in LTM revenues- continue to use the firm's video chat and conferencing products. However, growth in the most lucrative customer group, those with the highest revenue contribution, is also slowing down. Zoom had 2,507 customers generating more than $100 thousand in annual recurring revenues in the third-quarter… which calculates to a customer group growth rate of 94% year over year. In the second-quarter, Zoom grew this customer category by 131% and growth rates have steadily declined since the first-quarter.

Improving customer monetization

Zoom measures its customer monetization with a figure called net dollar expansion rate/NDER. The net dollar expansion rate measures the firm's internal revenue growth on a per-customer basis and expresses how much more money existing customers spend on Zoom's video conferencing platform, from one reporting period to the next. Zoom's NDER has consistently remained above 130%, meaning the firm's average customer increased spending by more than 30% compared to the year-earlier period. A high NDER implies strengthening customer monetization, and success in customer retention and up-selling.

Expenses are rising

Zoom has to constantly innovate and expand its product suite to keep customers happy. But this costs a lot of money. Expenses in the first nine months of the year increased in all expense groups- R&D, S&M and G&A- and, if expenses grow faster than sales, margin declines could be a result of the revenue slowdown.

Zoom is still overvalued...

The worst thing that can happen to a growth company like Zoom is that it has to warn of slowing growth because it immediately creates pressure on the valuation. This is what is happening here. The disappointing outlook for Q4'22 also indicates that revenue estimates for Zoom will fall once they get refreshed.

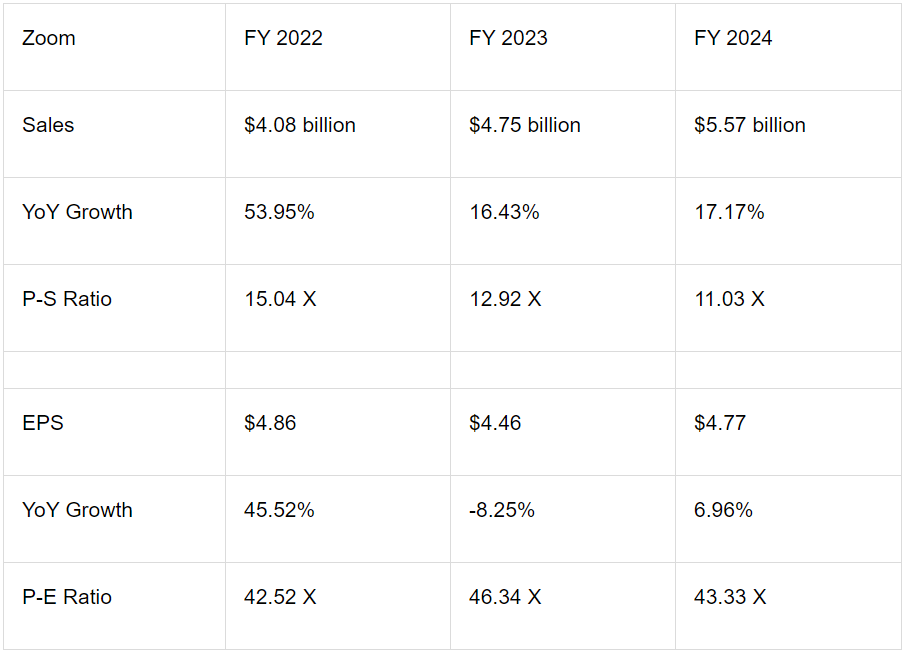

Despite a 39% drop in pricing this year, the video chat firm's growth prospects are overvalued. Zoom is expected to generate revenues of $4.08B this year and $4.75B next year. The revenue growth rate for next year, implied by estimates, is just 16.43%. Despite the sharp slowdown in growth, shares of Zoom still trade at a P-S ratio of 13 (based off of FY 2023 estimates).

Risks with Zoom

Zoom is in a critical situation: The world is moving on from the pandemic and it poses a challenge for a business that heavily benefited from digital transformation trends and remote working. New COVID-19 lockdown orders, like the ones that were just implemented in Europe, could accelerate Zoom's growth again. Longer term, the COVID-19 pandemic is poised to come to an end and there is considerable uncertainty as to how Zoom's growth will look like once the world fully returns to normal.

Final thoughts

I don't believe we have seen the end of this post-pandemic readjustment. The revenue slowdown is a real problem and Zoom has not found a recipe yet to counter this decline. New product roll-outs may counter the decline in revenue growth temporarily, but 'the new normal' will likely be a post-pandemic period of slower growth!