Summary

- Apple has spent years working on its own electric vehicle and autonomous driving system.

- After many fits and starts, the project appears to be back on track; the Apple Car is now expected to debut in 2025.

- Analysts and investors have responded positively toward Apple's EV ambitions thus far; perhaps unsurprising given the EV bullish frenzy.

- Apple may benefit from mounting excitement as the project moves ahead, but the long-term economic case for the Apple Car is suspect.

- If Apple commits to building a significant EV footprint, it will likely result in lower margins and higher costs for the company in the long run.

It is no secret that Apple Inc. (NASDAQ:AAPL) has long toyed with the idea of launching its own electric vehicle (“EV”) line. The company has titillated analysts and investors for years with the prospect, yet time and again it ended up coming to nothing. So, when a fresh round of rumors began to swirl this fall, I initially viewed them with a healthy degree of skepticism.

Yet the rumors proved remarkably persistent, gaining steam thanks to rising interest among Wall Street analysts. The rumors became far more concrete earlier this month in light of Bloomberg’s reporting on Apple’s internal plans, which call for the Apple Car to launch in 2025.

It is easy to understand why investors and analysts would be excited about an Apple EV. On paper, the idea of the Apple Car is unquestionably exciting. In reality, however, the economics of the Apple Car may leave much to be desired.

Let’s discuss.

Riding On High Hopes

To understand the Apple Car, we must first understand the EV space. EV companies are clearly enjoying a moment in the sun. The EV bull market has been fueled in no small part by the bubbly analyst forecasts and research notes coming out of Wall Street with increasing regularity in recent years. This bullishness has already seeped into analyst coverage of the Apple Car, especially that of Bernstein’s IT Hardware and Electric Vehicles team. In fact, it was Bernstein’s EV analysts who really sparked the latest revival of interest in Apple’s EV ambitions. In February, they highlighted Apple’s potential development partners, name-checking Volkswagen AG (OTCPK:VWAGY) in particular. Their August research update fanned the market flame further, laying out projections of exponential growth. According to Bernstein, Apple Car sales can reach 1.5 million vehicles per year, with annual revenue to the tune of $75 billion, in under a decade.

Of course, financial forecasts about the Apple Car mean little if there is no Apple Car. Apple’s decision to play its cards close to the vest has only served to fuel wild speculation. On Nov. 18th, Bloomberg offered a welcome dose of new information. According to Bloomberg, Apple has settled on both a strategy and a timeline for the Apple Car:

For the past several years, Apple’s car team had explored two simultaneous paths: creating a model with limited self-driving capabilities focused on steering and acceleration––similar to many current cars––or a version with full self-driving ability that doesn’t require human intervention. Under the effort’s new leader––Apple Watch software executive Kevin Lynch––engineers are now concentrating on the second option. Lynch is pushing for a car with a full self-driving system in the first version, said the people, who asked not to be identified because the deliberations are private...Apple is internally targeting a launch of its self-driving car in four years, faster than the five- to seven-year timeline that some engineers had been planning for earlier this year. But the timing is fluid, and hitting that 2025 target is dependent on the company’s ability to complete the self-driving system -- an ambitious task on that schedule. If Apple is unable to reach its goal, it could either delay a release or initially sell a car with lesser technology.

Unsurprisingly, this Bloomberg revelation has sparked a flurry of analyst commentary. Adam Jonas of Morgan Stanley (MS) has been especially visible in recent days discussing the Apple Car in general, and its planned autonomous driving capabilities in particular. Remarkably, Jonas’ forecast is even more bullish than Bernstein’s,projecting 1.8 million vehicle sales in 2030(all of which he expects to be fully autonomous).

Economic Reality Check

If Apple is genuinely serious about making the Apple Car a reality at long last, I see little risk of it outright failing. Bernstein made this point quite clearly in August:

Given its revenue base, few addressable markets are sizeable enough to impact Apple’s financials, but the auto sector offers a uniquely large, addressable consumer market...A successful EV launch from Apple would add a formidable, well-capitalized competitor to the automotive industry.

Apple clearly has the financial resources, brand power, and know-how to carve out a healthy piece of the EV pie for itself if that is what it wants to do. But confidence in Apple’s ability to make a successful EV play is not what really matters, at least from an investment standpoint. The real question is why Apple would even want to do it in the first place.

Apple’s core (pardon the pun) value proposition is its consumer tech and digital services empire. This business has become a veritable cash-printing machine. Even after spending a monumental $85.5 billion on stock buybacks in 2021 thus far, Apple still has $62.6 billion in cash on hand. Thatcash pile is the product of a business with incredibly high margins operating in an industry over which Apple can exert considerable market power.

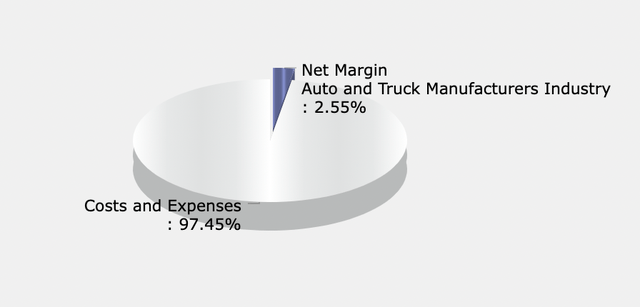

Venturing into the automotive industry will force Apple to face an entirely different kind of beast, economically speaking. Apple currently boasts gross and net profit margins of 46.6% and 23.7%. Among global automakers, meanwhile, the industry average gross margin is 27.9%, while net margin is a wafer-thin 2.6%.

Apple’s foray into cars would almost certainly mean more capital investment and thinner margins overall, with the mix set to get worse the larger its automotive division becomes relative to its wider business. That hardly sounds like a recipe for value creation.

Investor’s Eye View

Given the economic realities prevailing in the automotive sector, it is difficult to understand why Apple would want to be involved in it at all. While there may be something to the argument that autonomous vehicles can fundamentally transform the economics of the automotive industry, it is far from clear whether self-driving cars and robotaxis will improve margins substantially. Indeed, there is agrowing body of research calling this belief into question.

Perhaps it is the bull market in EV stocks that has enticed Apple back to the table. After all, investor excitement has reached such a fever pitch that even pre-revenue EV startups can now claim valuations rivalling those of established automakers netting billions of dollars in profit annually. Right now, Ford Motor Co. (F) and Lucid (LCID) have virtually the same market capitalization, despite Ford having posted $1.8 billion in net income for Q3 2021 compared to Lucid’s $7 million net loss. Perhaps Apple perceives the Apple Car as an opportunity for an upward revaluation of its enterprise even if it ultimately compresses the company’s overall profit margins and cash generation potential.

Ultimately, I see little about the automotive sector – EV or otherwise – that would make it a natural fit for Apple. While I suspect development of the Apple Car over the next few years will act as a positive catalyst for Apple’s stock, it will end up being more of a liability than an asset.

In my assessment, investors buying Apple on the basis of its EV future would be wise to think again.

Trade carefully!